IFSC Code Explained: How Bank Routing Works in India

Understand the step-by-step routing process of bank transfers in India. Learn how IFSC codes guide NEFT, RTGS, and IMPS transactions in 2026.

Table of Contents

Have you ever experienced that heart-stopping moment when a crucial payment seems to vanish into thin air, or a transaction gets delayed for reasons unknown? I certainly have, and it often boils down to the intricate, yet often overlooked, details of how banks communicate. Understanding the Bank Routing Process Using IFSC Code isn’t just for finance professionals; it’s essential knowledge for anyone navigating India’s digital economy. The IFSC code acts as the digital address label on your financial mail, ensuring your money reaches the correct recipient swiftly and securely, a process far more sophisticated than a simple account number might suggest.

Decoding the IFSC: Your Digital Compass

The Indian Financial System Code, or IFSC, is an 11-character alphanumeric code that uniquely identifies every bank branch participating in electronic funds transfer systems in India. It’s not merely a random string of letters and numbers; rather, it’s a meticulously designed identifier that serves as a digital compass for your money. Without the correct IFSC, electronic transfers like NEFT, RTGS, or IMPS simply wouldn’t know where to direct the funds, leading to frustrating delays or even failed transactions. Think of it as the postal code for your bank branch, crucial for pinpoint accuracy.

Every single bank branch in India has its own unique IFSC, making it an indispensable component for interbank transactions. This specificity ensures that when you initiate a transfer, the system can precisely route your funds to the intended branch, regardless of the bank. It underpins the entire digital banking infrastructure, making seamless financial interactions possible across the vast network of Indian banks. Its importance cannot be overstated in today’s fast-paced financial landscape, where speed and accuracy are paramount.

Anatomy of an IFSC Code

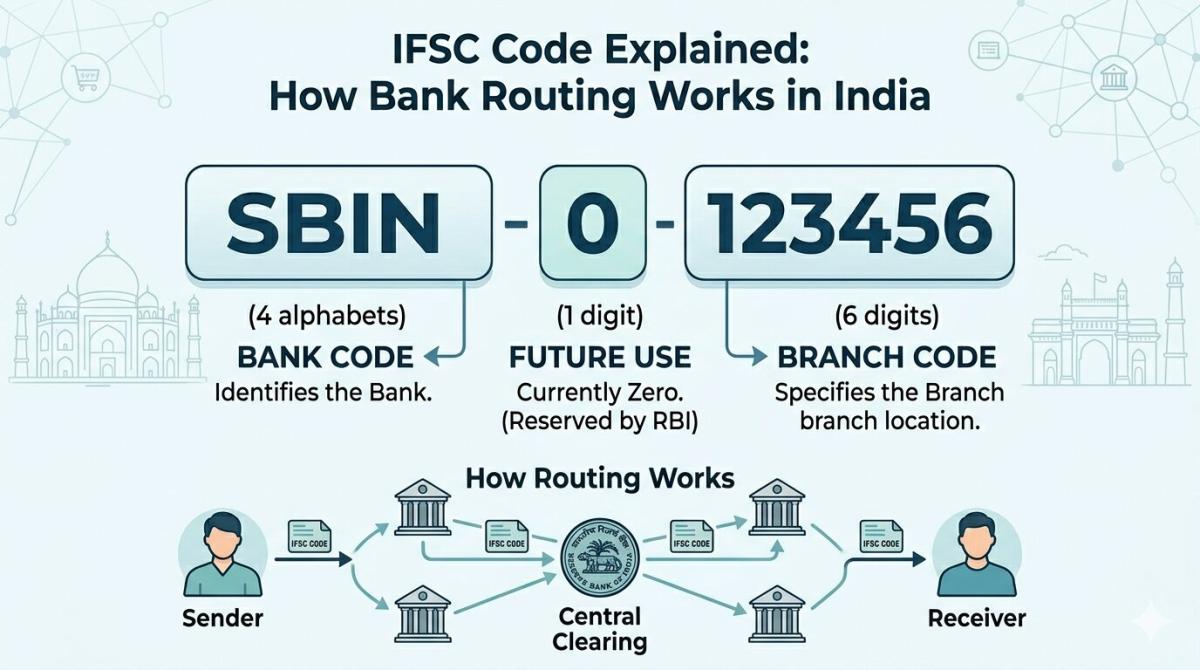

Delving deeper, the 11 characters of an IFSC code are not arbitrary. The first four characters represent the bank code, identifying the specific financial institution. For instance, “ICIC” would denote ICICI Bank. The fifth character is always a zero, serving as a control character for future use and ensuring uniformity. The subsequent six characters identify the individual bank branch. This structured format allows for millions of unique branch identifiers, accommodating the extensive banking network across India and providing a robust, scalable system for financial routing well into 2026 and beyond.

IFSC’s Core Role in NEFT & RTGS

When you initiate a National Electronic Funds Transfer (NEFT), the IFSC code is fundamental to the process. NEFT operates on a deferred net settlement basis, meaning transactions are processed in batches at specific intervals throughout the day. The originating bank uses the beneficiary’s IFSC to identify the correct destination branch and forwards the transaction details. Without this precise routing information, the central clearing system, managed by the Reserve Bank of India, would be unable to sort and settle the funds effectively, highlighting the code’s critical behind-the-scenes functionality.

Similarly, for Real-Time Gross Settlement (RTGS) transactions, which are typically for high-value transfers and processed individually on a real-time basis, the IFSC code is equally indispensable. RTGS ensures immediate and final settlement, crucial for time-sensitive large payments. The IFSC ensures that the funds are routed directly and instantly to the correct beneficiary bank branch, facilitating the rapid movement of capital across the financial system. This real-time capability, powered by accurate IFSC information, is a cornerstone of modern corporate and interbank finance. For more on these systems, the Reserve Bank of India website provides excellent resources.

Real-Time Payments: IMPS & UPI

The Immediate Payment Service (IMPS) has revolutionized personal banking by enabling instant, 24/7 interbank electronic fund transfers. The IFSC code is central to how IMPS functions, allowing funds to be credited to the beneficiary’s account almost instantaneously, even on holidays or weekends. When you use IMPS, your bank leverages the recipient’s IFSC to identify their bank and branch, ensuring the immediate and accurate delivery of funds. This system has significantly enhanced convenience, moving away from batch processing to truly real-time transactions.

The Unified Payments Interface (UPI) has further transformed India’s digital payment landscape, making transactions incredibly user-friendly. While UPI often uses Virtual Payment Addresses (VPAs) like “yourname@bank” or mobile numbers for transactions, the underlying bank routing process still relies heavily on the IFSC code. These VPAs are essentially aliases linked to your bank account, which in turn is tied to a specific IFSC and account number. Therefore, even when you don’t explicitly enter an IFSC for a UPI transaction, it’s working diligently in the background to ensure your payment reaches its intended destination securely and efficiently, proving its continued relevance in 2026.

Navigating Common Routing Challenges

Despite the robustness of the IFSC system, errors can occur, leading to significant headaches. The most common mistake is entering an incorrect IFSC code, which can cause transactions to fail, be delayed, or, in rare cases, even be misdirected if the incorrect code happens to correspond to another valid account. Mismatched beneficiary names or account numbers also contribute to these issues. My personal advice is always to double-check every digit and character of the IFSC, especially when setting up a new beneficiary. An ounce of prevention truly is worth a pound of cure here.

To avoid these pitfalls, always verify the IFSC code directly with the beneficiary or through official bank channels. Many banks provide IFSC lookup tools on their websites, or you can cross-reference it with the details printed on a cheque leaf. Some online payment platforms also offer auto-fill or verification features, which can be incredibly helpful. Taking a moment to confirm these details can save you hours of tracing lost funds and dealing with bank customer service, ensuring a smooth and stress-free banking experience.

The Evolution of Digital Banking in India

The IFSC code has been a foundational pillar in India’s rapid digital banking transformation. Its standardized format and unique identification capabilities have enabled the seamless integration of various payment systems, from the foundational NEFT and RTGS to the revolutionary IMPS and UPI. This robust routing mechanism has fostered trust in electronic transactions, encouraging millions of Indians to embrace digital payments. It’s a testament to thoughtful infrastructure design that continues to serve as the backbone of financial innovation.

Looking ahead to 2026, while new payment technologies and digital currencies may emerge, the core principle of precise bank routing will remain paramount. The IFSC system, or an evolution of its underlying logic, will undoubtedly continue to play a critical role in maintaining the integrity and efficiency of interbank transactions. Its adaptability and proven track record suggest it will continue to facilitate the next wave of financial innovations, ensuring that money moves accurately and securely across an increasingly interconnected digital economy.

Key Takeaways

- IFSC is Crucial for Electronic Funds Transfer: The 11-character Indian Financial System Code uniquely identifies every bank branch, acting as a digital address for seamless NEFT, RTGS, IMPS, and UPI transactions.

- Structured for Precision: Its specific format (bank code, zero, branch code) ensures accuracy in routing funds, preventing delays and misdirection across India’s vast banking network.

- Underpins Real-Time Payments: While not always overtly entered, IFSC is fundamental to the speed and reliability of modern payment systems like IMPS and UPI, linking virtual addresses to physical bank branches.

- Verification is Key to Avoiding Errors: Always double-check IFSC codes with official sources to prevent common pitfalls such as failed transactions or misdirected funds, ensuring your money reaches its intended destination.

Frequently Asked Questions

Can an IFSC code be incorrect or change?

Yes, an IFSC code can sometimes be incorrect if provided erroneously, or it might change if a bank branch relocates, merges, or is closed. While rare, it’s crucial to verify the latest IFSC with the bank or reliable online tools before initiating any transaction to prevent issues.

Is IFSC required for all bank transfers in India?

For most interbank electronic fund transfers within India, such as NEFT, RTGS, and IMPS, the IFSC code is a mandatory requirement. While UPI transactions might use a VPA or mobile number, the underlying system still relies on the IFSC to route funds to the correct bank account.

What happens if I use a wrong IFSC code?

If you use an incorrect IFSC code, the transaction will typically fail and the funds will be returned to your account. However, in rare instances where the incorrect IFSC code corresponds to another valid bank branch and account number, funds could be misdirected. Always verify details carefully.

How can I find the correct IFSC code for a bank branch?

You can find the correct IFSC code on your bank’s official website, your cheque book, your bank passbook, or by using reliable online IFSC lookup tools provided by financial institutions. It’s always best to cross-reference the information for accuracy.

Conclusion

The IFSC code, though often an unseen player, is the silent workhorse behind India’s digital payment revolution. Its precise routing capabilities ensure that billions of transactions flow smoothly and securely every single day. As we look towards an even more digitally integrated financial future in 2026, understanding and correctly utilizing the IFSC code remains fundamental. It’s not just a string of characters; it’s the bedrock of trust and efficiency in our modern banking system, empowering us all to transact with confidence.

Related Blogs

Published on May 06, 2026

Backend Processing of UPI and IFSC Based Transfers Explained in Depth

Explore the backend processing of UPI and IFSC-based transfers, comparing real-time APIs, batch settlement systems, and how NPCI and RBI power secure digital payments in India.

Arjun Sharma

Content Lead – Banking & Payments

Published on May 06, 2026

How Banks Manage Transaction Queues During Peak Load

Learn how banks manage transaction queues during peak load using distributed systems, priority queues, load balancing, and real-time processing to ensure fast and reliable payments. Author

Arjun Sharma

Content Lead – Banking & Payments

Published on May 06, 2026

How Bank Switches Process Interbank Transactions

Learn how bank switches process interbank transactions by routing, authorizing, and securing payments between banks in real time using advanced switching systems and payment networks.

Arjun Sharma

Content Lead – Banking & Payments

Published on May 06, 2026

Technical Reasons Behind Delayed IMPS Transactions

Explore the technical reasons behind delayed IMPS transactions, including network latency, server downtime, bank processing delays, API failures, and high transaction volumes.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 28, 2026

How Banks Sync Data Between Branches Instantly

Learn how banks sync data instantly across branches using core banking systems, real-time processing, high-speed networks, and secure database technologies.

Arjun Sharma

Content Lead – Banking & Payments

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ