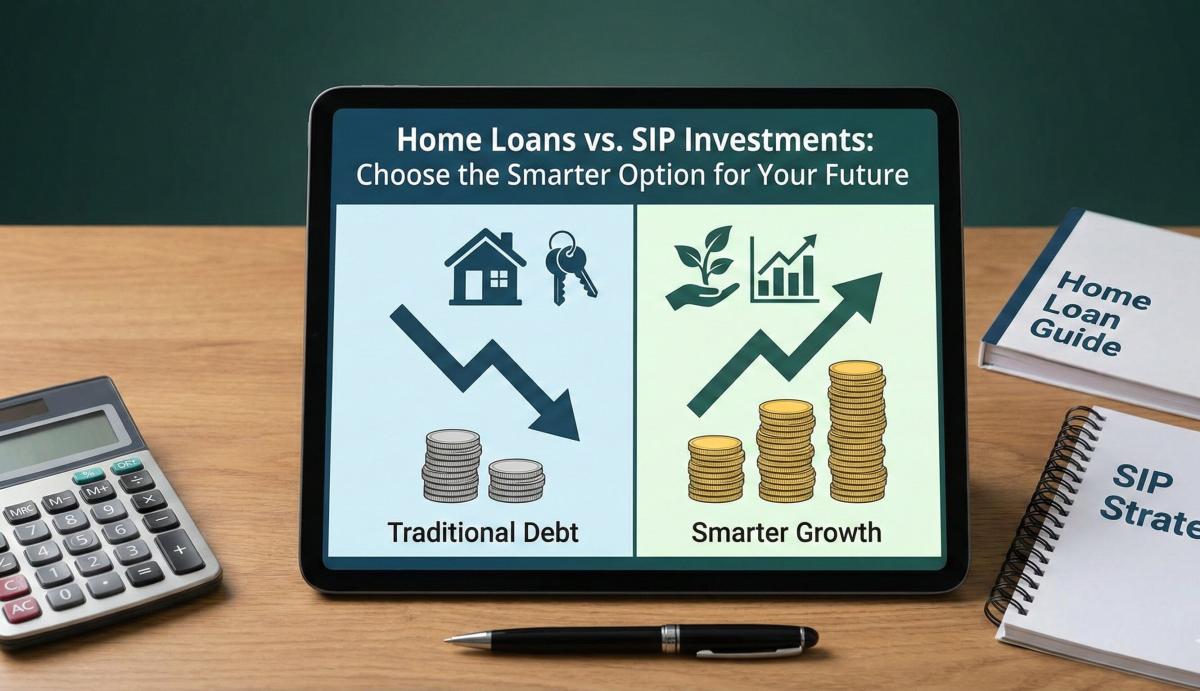

Home Loans vs SIP Investments: Choose the Smarter Option for Your Future

Confused between SIP investments and home loans? Learn the pros and cons of each to make smarter, goal-based financial decisions. Find out what suits you best.

Table of Contents

- What to Know About Home Loans

- Pros of Home Loans

- Cons of Home Loans

- What is an SIP?

- Benefits of SIP Investments

- Disadvantages of SIP Investments

- A Comparison of Home Loans vs SIP Investments

- Factors to Consider When Making a Decision

- Choosing Between Home Loans vs SIP Investments Depends on Your Goals and Risk Tolerance

- FAQs

Deciding whether to take a home loan or invest in SIPs can be confusing. Each has its benefits and potential downsides, and it really comes down to what you want to accomplish financially, how much risk you can tolerate, and your future plans. This guide lays out specifics on Home Loans vs SIP Investments to help you make the right decision.

What to Know About Home Loans

A home loan is the money you borrow from a bank or financial institution to buy or build a house. Your new house becomes the collateral until you repay the entire loan. They have fixed or variable interest rates and can be set to run from 10 years up to even 30 years.

Pros of Home Loans

While taking a home loan could be a lengthy process, here are some of its benefits:

- Have a Place to Call Your Own: There is nothing like the feeling of being able to say that you own your home.

- Appreciation: Property can often increase in value over time, making it a solid investment.

- Tax Benefits: Home loans come along with lucrative tax benefits, where the borrower gets the dual benefit of saving on taxes while obtaining a home likewise.

Cons of Home Loans

Even though there are many benefits, here are some cons to consider:

- Large Interest Charges: While the interest rates are affordable, you will undoubtedly pay a large sum over the life of your loan.

- Long-term Commitment: A home loan is a huge commitment for which you have to make the payment regularly for many years.

- Market Risk: The price of your home increases or decreases based on the market.

What is an SIP?

You can invest in mutual funds through a Systematic Investment Plan (SIP) where you need to contribute a fixed amount of money regularly. Doing so methodically is what forces you to grow your portfolio piece by piece.

Benefits of SIP Investments

Here are some key benefits of SIP investments:

- Compounding Returns: With SIPs, you can enjoy the benefit of compounding. Through this, you can grow your savings over a period of time.

- Convenient: Liquidating an SIP investment is a relatively simpler process when you need the money.

- Risk Diversification: Your investment from SIP is distributed to sectors and assets that reduce your overall risk.

Disadvantages of SIP Investments

Even though SIP investments can significantly grow your portfolio, here are some disadvantages to consider:

- Market Fluctuations: The market conditions can fluctuate, which could lead to varying returns on SIPs.

- No Physical Asset: Unlike a home, SIPs do not lead to the ownership of anything tangible.

- Discipline is Required: Regular, disciplined investing must happen, and you must be patient to see better returns.

A Comparison of Home Loans vs SIP Investments

As you choose between home loans vs SIP investments, here are a few key things to keep in mind:

Your Financial Goals

- Home Loan: Best for people who wish to own a home and have an asset in hand.

- SIP: Ideal for seasoned investors growing their wealth through diversified investments of time in the market.

Low Risk, High Reward

- Home Loan: Typically low risk because you are left with an actual property. That being said, the value may go up and down.

- SIP: Market-driven, so there’s a higher risk but potential for more returns.

Repayment

- Home Loan: You should plan for long-time regular payments.

- SIP: This form of investing allows for more flexibility. You can modify the investment amount based on your investment situation.

Tax Benefits

- Home Loan: Tax savings on both the principal and interest portion.

- SIP: Tax benefits are tentative as per the type of mutual fund and tenure of the investment.

Factors to Consider When Making a Decision

Additionally, these are the key factors that you should consider before finalising between home loans vs SIP investments:

- Length & Time

If you are looking for a home in the next year, you may need loans. For wealth building (long-term goals), SIPs might do the trick.

- Current Financial Situation & Income

Stability in your earning power as per current and future job stability; home loans require you to make regular payments, and an SIP can be more flexible.

- Current Debts

Consider your existing debts before borrowing a new loan.

- Be Risk-averse

If you have a relatively low-risk tolerance, taking a home loan is better as it gives an appreciating physical asset. If you can bear market volatility, investing in an SIP might provide increased earnings.

- Market Conditions

If property prices are set to increase, a home loan is a great investment. Similarly, if the stock market is booming, then SIPs could be a better bet.

Choosing Between Home Loans vs SIP Investments Depends on Your Goals and Risk Tolerance

When it comes to deciding between investing in an SIP and a home loan, you need to determine what best suits your financial objectives, schemes, and risks associated with the latter. Home loans provide a sense of security in the form of an asset and tax savings, while with SIPs, you get freedom, liquidity, and potential for higher returns.

The best route is somewhere in the middle. Maintain perspective and look at both options based on your financial goals and where you hope to find yourself in the future. When you decide on a home loan, an SIP investment, or a combination of both, ensure that your choice is in sync with your individual financial goals and risk profile.

FAQs

- What is better, a home loan or an SIP?

This depends on what you're aiming for. A home loan lets you buy your place, but you'll be paying interest on top of the price. It's a long commitment, but the house could go up in value, and you might even get some tax breaks on your repayments. SIP, on the other hand, is like saving for the future, a bit at a time. You invest your money, and hopefully, it grows over time. It's flexible, so you can start small and adjust how much you put in as needed.

- Which is better: SIP or EMI?

Both are very different. SIP is like putting money away to grow it, kind of like planting seeds. The stock market can be unpredictable, so things might not go as planned. But if you're in it for the long haul, SIPs can be a great way to build wealth. EMI, on the other hand, is that fixed monthly payment you make on a loan, like for a house or car. By paying your EMIs on time, you eventually own that thing you borrowed money for. So, SIP is for growing your money, and EMI is for paying off debt.

- Is it better to close a home loan or invest in mutual funds?

Paying off your home loan completely means you'd be debt-free, giving you peace of mind and freeing up extra cash each month. But that extra cash wouldn't be available to invest in mutual funds, which have the potential to grow your wealth a lot over time. The best choice depends on your situation and how comfortable you are with risk.

- What if I SIP 30,000 per month for 5 years?

It's impossible to say for sure how much you'll have after 5 years because the market can go up and down. But SIPs benefit from something called compounding, which is basically like earning interest on your interest. This can boost your returns in the long run. The key is to stay invested for a while to ride out the ups and downs of the market.

Related Blogs

Published on Mar 25, 2026

CIBIL Score Explained: What It Is, How It Is Calculated, and How to Improve It

Learn how Credit Information Bureau (India) Limited scores impact your loans. Discover how CIBIL is calculated, why it matters, and tips to improve your credit.

Arjun Sharma

Content Lead – Banking & Payments

Published on May 18, 2025

Tips on How to Calculate Monthly EMI for Any Loan

Struggling to understand your EMI amount? This blog covers all the necessary tips on how to calculate your monthly EMI to help you stay ahead of your finances.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Apr 25, 2025

Monthly EMI Calculators: A Detailed Overview

Monthly EMI calculators allow you to get a pre-hand idea of the EMI you must pay monthly. In return, an EMI calculator per month helps manage monthly finances better.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Mar 02, 2025

Buying a Car? Here's How to Use a Vehicle EMI Calculator the Smart Way

Plan your car or bike loan with ease. Learn how to use a vehicle EMI calculator, input values correctly, and get accurate monthly EMI instantly.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Feb 17, 2025

Master EMI Calculators: How to Estimate Your Monthly Payments with Ease

Learn how EMI calculators work to estimate monthly payments accurately. Explore EMI formulas, examples, and factors to make smart financial decisions.

Arjun Sharma

Content Lead – Banking & Payments

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ