How to Maximise Your FD Returns: Tips for Choosing the Right Tenure?

Learn how to maximise your FD returns by selecting the right tenure. Discover strategies like FD laddering, cumulative interest, and reinvestment tips to grow your wealth effectively.

Table of Contents

Fixed Deposits (FDs) are a reliable and safe investment option for those looking to earn stable returns without much risk. However, the key to making the most out of your FD returns lies in choosing the right tenure. While it might seem simple, the tenure you select plays a crucial role in determining your interest earnings. In this blog, we’ll explore how to choose the right tenure and maximise FD returns.

Understanding Fixed Deposit Tenures

The tenure of an FD refers to the duration for which you invest your money in the deposit. Depending on the bank or financial organisation, this could last a few months to many years. Longer tenures may provide greater rates, but that is not always the case; the interest rate on FDs usually changes with the tenure.

Common Fixed Deposit tenures are:

- Short-term FD: 7 days to 12 months

- Medium-term FD: 1 to 5 years

- Long-term FD: 5 to 10 years

The interest rates on medium—to long-term deposits are usually slightly lower than deposits for a shorter term, but short-term FDs help manage liquidity.

How to Maximise Your FD Returns: Tips for Choosing the Right Tenure

Choosing the right tenure for your FD comes down to many factors, the most important one being your personal preference and needs in the short term and long term. Here are a few investment tips to effectively maximise FD returns:

- Consider Your Financial Goals

The FD tenure is much influenced by your financial goals and investment horizon. A 1- or 2-year FD can be perfect for your short-term savings—that of a vacation or a wedding. Long-term objectives like children's schooling or retirement would make more sense with a longer tenure since compounding interest over time benefits.

- Assess the Interest Rate Trends

FD interest rates usually change depending on central bank policies and the state of the market. Before deciding on the tenure, one should monitor changes in interest rates. Should rates be rising, you might wish to lock your money for a shorter period and renew the FD at a higher rate later. On the other hand, choosing a longer term guarantees you lock in a better rate should rates be dropping.

- Consider the Reinvestment Option

You might choose longer-term FDs with cumulative interest instead of short-term FDs and continuous renewal of them. Under this alternative, you compound your returns over time by adding interest to the principal at periodic intervals.

- Opt for Laddering

Maximising returns while preserving liquidity is achieved via FD laddering by means of which You split your money among many tenured FDs. In this sense, you gain flexibility by ensuring some deposits mature sooner and from better interest rates on longer-term FDs.

For instance, you might divide ₹5 lakhs in a single 5-year FD into five FDs of ₹1 lakh each with tenures of 1, 2, 3, 4, and 5 years. You can reinvest each FD at the going rates or spend the money as required as it ages.

- Use an FD Calculator

One useful tool for computing the returns for several tenures and interest rates is an FD calculator. Entering the principal amount, interest rate, and tenure will help you to compare the returns over several periods readily. This will help you choose a tenure that fits your financial objectives.

- Check for Special Tenure Offers

Certain banks or NBFCs have unique interest rates for particular tenures, say 500 or 750 days. Investigating these offers is worthwhile as they could yield superior returns compared to conventional tenure choices.

- Tax Considerations

Interest accrued on FDs is liable under "Income from Other Sources." Should you belong to a higher tax rate, FD interest tax can lower your total returns. Investing in tax-saving FDs, which have a 5-year lock-in term but provide tax deductions under Section 80C, is advised in such circumstances.

- Avoid Premature Withdrawals

Premature withdrawal of your FD before maturity might attract penalties and/or low rates of interest, which will burn your profits. In case you expect to require the money in the early future, then you should consider dividing your investment into several smaller FDs, not in a single lump sum. In this case, it is possible to withdraw only whatever amount you may require without interfering with other saved amounts.

Risks and Considerations in FD Investments

Although Fixed Deposits (FDs) are usually seen as a safe investment, there are several things you should think through before locking up your money:

Inflation Risk

The possible effects of inflation constitute one of the most important hazards of FDs. If inflation increases faster than the interest rates on your FD over time, the actual worth of your dividends could be diminished. This risk must thus be carefully considered, particularly for long-term investments.

Lack of Flexibility

Unlike more liquid assets, once money is locked in an FD, it cannot be retrieved until maturity unless you are ready to pay penalties. This could be a disadvantage if you unexpectedly need money for an emergency or a better investment opportunity presents itself.

Fixed Interest Rates

FDs have set returns; hence, even if market interest rates rise, your FD won't gain from the better rates until maturity. This could restrict possible returns relative to more flexible or market-linked investment choices.

Conclusion

Maximise FD returns by selecting the right term. Understanding interest rate patterns, thinking through laddering and reinvestment choices, and applying an FD calculator will help you make wise selections according to your financial objectives. To find the ideal balance and maximise your fixed deposit investment, always compare your liquidity demands to possible rewards.

FAQs

1. What is the best tenure for a Fixed Deposit?

The ideal tenure depends on your financial goals. Short-term FDs (less than a year) suit immediate needs, while long-term FDs (5-10 years) offer higher returns for wealth accumulation.

2. How does tenure affect FD interest rates?

Generally, longer tenures offer higher interest rates. However, some banks may offer competitive rates for specific mid-term tenures, such as 1-3 years.

3. Can I withdraw my FD before maturity?

Yes, but premature withdrawals may attract penalties, and the interest will be lower. To avoid this, consider creating multiple smaller FDs instead of one large deposit.

4. What is the FD laddering strategy?

FD laddering involves splitting your investment into multiple FDs with varying tenures. This ensures regular payouts and flexibility to reinvest at higher interest rates upon maturity.

Related Blogs

Published on Mar 27, 2026

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

Arjun Sharma

Content Lead – Banking & Payments

Published on Mar 27, 2026

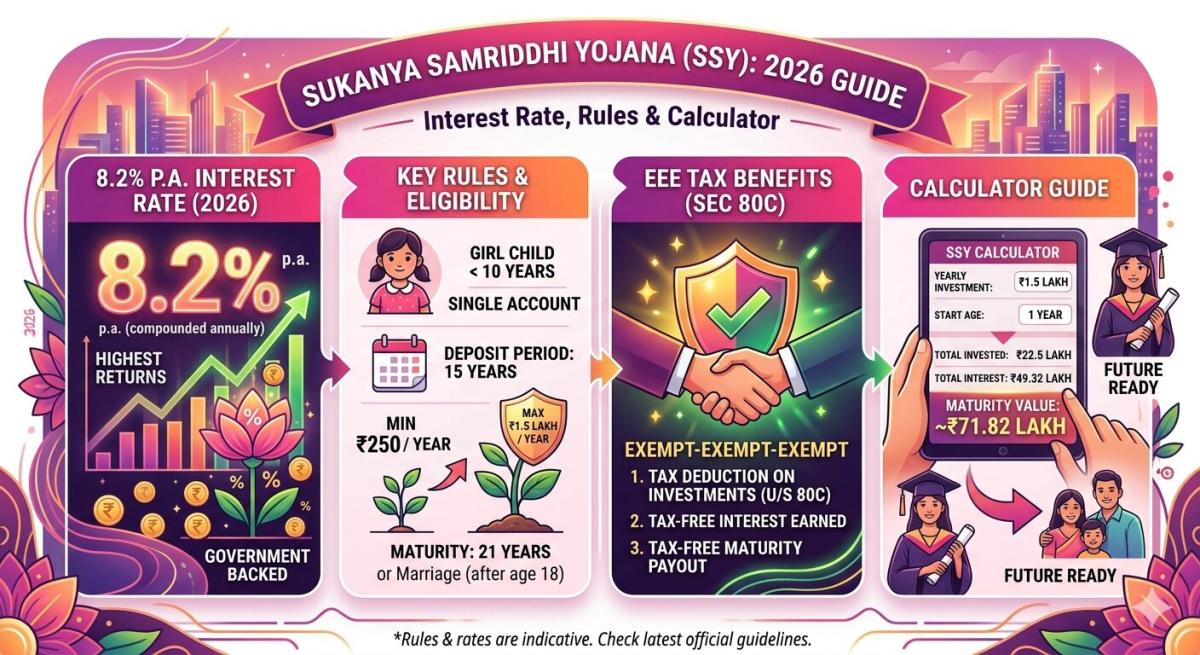

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

Arjun Sharma

Content Lead – Banking & Payments

Published on Mar 02, 2026

Planning an FD? Don’t Miss These Top Questions About FD Calculators

Curious how FD calculators work? This guide answers the top questions to help you calculate returns, compare plans, and invest smarter in fixed deposits.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Mar 02, 2026

PPF (Public Provident Fund) Calculator – Returns, Interest & Planning Guide

A PPF Calculator helps you estimate the maturity value and interest earned on your Public Provident Fund investment. By entering your contribution amount, tenure, and current interest rate, you can project long-term returns and plan your savings effectively.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Mar 02, 2026

Recurring Deposit (RD) Calculator – Returns, Interest & Maturity Guide

An RD Calculator helps you estimate the maturity amount and interest earned on your Recurring Deposit investment. By entering your monthly deposit, tenure, and interest rate, you can project returns and plan your savings effectively.

Priya Nair

Senior Compliance Editor at IFSC.co

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ