PPF vs. Other Tax-Saving Instruments: A Comparative Analysis

Discover the key differences between PPF vs. other tax-saving instruments like NPS, ELSS, and FDs. Learn about PPF benefits, tax-saving options, and more.

Table of Contents

When it comes to saving taxes, selecting the right tax-saving investment will not only lower your tax load but also, over time, increase your wealth. Of the several choices, the Public Provident Fund (PPF) is always a somewhat common one.

PPF vs tax-saving instruments is a common debate among individuals who want to save tax and invest for the future. Examining its special qualities and advantages, this article will compare PPF with other important tax-saving tools to enable you to make a knowledgeable decision.

Understanding PPF

The Public Provident Fund or PPF is a long term saving plan launched by the Indian Government. It aims to increase own and others’ savings to the general public by emphasising safety, good returns on investments, and tax advantages. Here are some of the key features of PPF:

- Tenure: The PPF has a fixed investment period of 15 years, which can, however, be renewed in intervals of 5 years.

- Minimum and Maximum Investment: A minimum investment of ₹ 500 per year to a maximum of ₹ 1,50,000 per year is necessary for a subscription to the journal.

- Interest Rate: The government sets the interest rate on a yearly basis, although there is a provision to change it quarterly. This rate is usually higher than that of a simple savings account.

- Tax Benefits: The amount paid to PPF is also tax-exempt under 80C of the Income Tax Act, and the interest earned under this scheme is also exempt from tax.

PPF Benefits

PPF benefits us in many ways that make it a preferred choice for tax-saving investments:

- Safety: PPF, being a government-backed plan all over, is referred to as a risk-free investment plan.

- Guaranteed Returns: It is known to have a fixed interest rate, and this rise-up guarantees fixed returns above any other market-related investment.

- Tax-Free Growth: In particular, all the agreed sum, including interest and the principal(, becomes tax-free at maturity, which makes it very effective for investors.

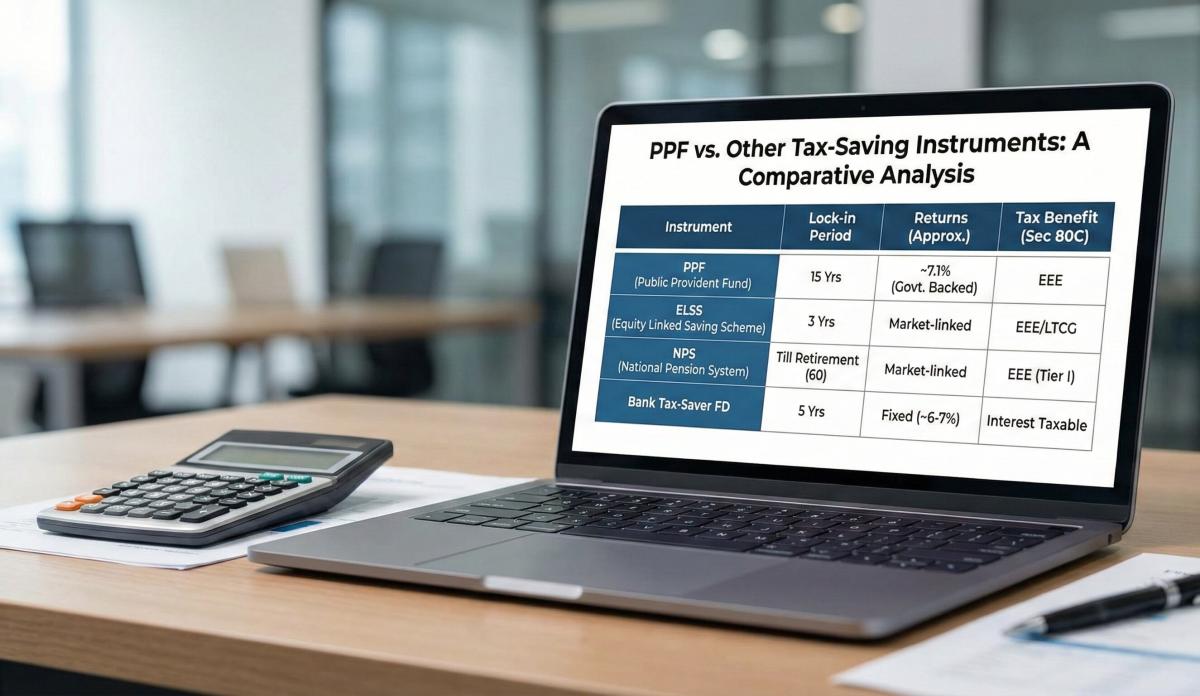

Comparing PPF vs Tax-saving instruments

While PPF has its merits, it's essential to compare it with other popular tax-saving instruments available in India to make informed decisions.

1. National Pension System (NPS)

The National Pension System is a long-term investment plan that provides returns on retirement. It offers facilities to invest in equities and fixed-income instruments.

- Tax Benefits: NPS can be funded through a regular instrument of tax-saving and is allowed under Section 80C for the contribution made along with an extra deduction of Fifty thousand under Section 80CCD(1B).

- Liquidity: NPS has lock-in tenure until the retirements but partial withdrawal can be made in certain circumstances.

- PPF vs. NPS: Although NPS can provide higher growth because it is linked to stocks and offers equity-linked returns, it has higher risks and lower liquidity than PPF.

2. Equity-Linked Savings Scheme (ELSS)

ELSS is one of the mutual fund products that invest mainly in equities and offers the maximum tax benefit.

- Tax Benefits: ELSS investments are also eligible for deductions under section 80C, and the lock-in period is at least three years.

- Risk Factor: Because they are equity-oriented, ELSS has higher risks than PPF, but it does come with the potential for higher rewards.

- PPF vs. ELSS: PPF is a less risky investment with assured returns, while ELSS is suitable for high-risk-takers who look for higher returns.

3. Fixed Deposits (FD)

Fixed deposits are savings plans in which one invests a certain amount for a certain period at a specific rate of interest.

- Tax Benefits: These fixed-income saving instruments are tax-saving, but they come with a lock-in period of five years; moreover, they come under section 80C.

- Interest Rate: The interest rates in FDs are usually relatively lower than those in the PPF.

- PPF vs. FD: PPF offers better tax exemptions and a higher rate of interest than the tax-saving fixed deposit.

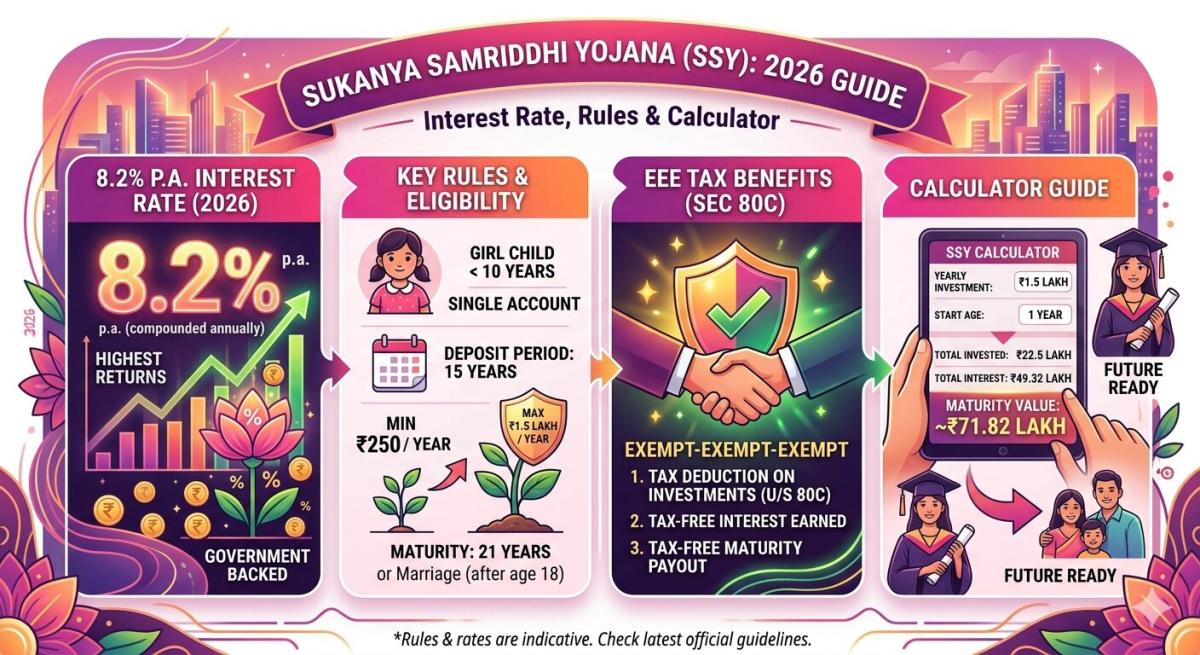

4. Public Provident Fund (PPF) vs. Sukanya Samriddhi Account (SSA)

The Sukanya Samriddhi Account is a savings scheme specially meant for the future needs of girl children.

- Tax Benefits: Like PPF, the contribution made to SSA is included in the special 80C deduction category.

- Tenure: The account then gains maturity when the girl child becomes 21 years old.

- PPF vs. SSA: PPF can be made by anyone at any time, while SSA is more focused on requiring money for Girl children and may offer higher interest rates.

Factors to Consider When Choosing a Tax-Saving Instrument

When you’re doing a PPF comparison with other tax-saving instruments, consider the following factors:

- Investment Horizon: Evaluate your financial target and whether you can afford to hold your money for a year or two.

- Risk Appetite: If you want to be extra cautious, you have to decide how much risk you are willing to take. PPF is particularly suitable for conservative investors, while products such as ELSS are suitable for aggressive or conservative investors.

- Liquidity Needs: Do you need a high level of liquidity? The period during which one cannot exit PPF is longer than that of other investment tools such as ELSS and NPS.

- Tax Efficiency: Assess how much more tax credit can be claimed from each plan, particularly if you are looking to optimise your tax deduction fully.

Conclusion

Therefore, the PPF continues to be one of the most promising and safe tools for saving taxes and receiving certain fixed and tax-exempt amounts of money. Nevertheless, before choosing your investment option, it is vital to know your financial objectives and your tolerance for risk.

However, PPF is comparatively better for saving for long-term goals like retirement, a kid’s marriage, or any big financial goal. NPS and ELSS are other instruments that are better for return seekers and comfortable with volatility.

Knowing the pros and cons of using PPF compared with other tax-efficient investments makes it possible to maximise the amount of money you can invest within the allowable limits while enjoying all the Tax-sheltered benefits. However, the most preferred instrument of tax savings is one that serves your purpose of investing and your capacity to take risks.

FAQs:

What is PPF, and how does it work?

The Public Provident Fund (PPF) comprises government-backed long-term savings plans with a 15-year lock-in term. It's a safe and tax-efficient investment choice with guaranteed interest rates, tax-free returns, and Section 80C exemptions.

How does PPF compare to other tax-saving instruments like ELSS and NPS?

Unlike ELSS and NPS, which involve equities and provide greater returns but come with more risk, PPF provides certain returns with little risk. NPS targets retirement savings; ELSS has a shorter lock-in period.

Is PPF a better option for risk-averse investors?

Given its government support, set yields, and tax-free interest, PPF is indeed perfect for risk-averse investors. It provides security and protection above erratic choices like ELSS or NPS.

What are the tax benefits of investing in PPF?

Highly tax-efficient, contributions to PPF are tax-deductible under Section 80C, and both the interest earned and the maturity amount are free from tax.

Can I make partial withdrawals from my PPF account?

Indeed, partial withdrawals from a PPF account are permitted following the seventh year of investment, therefore providing some liquidity in an otherwise long-term investment plan.

Related Blogs

Published on Mar 27, 2026

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

Arjun Sharma

Content Lead – Banking & Payments

Published on Mar 27, 2026

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

Arjun Sharma

Content Lead – Banking & Payments

Published on Mar 02, 2026

Planning an FD? Don’t Miss These Top Questions About FD Calculators

Curious how FD calculators work? This guide answers the top questions to help you calculate returns, compare plans, and invest smarter in fixed deposits.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Mar 02, 2026

PPF (Public Provident Fund) Calculator – Returns, Interest & Planning Guide

A PPF Calculator helps you estimate the maturity value and interest earned on your Public Provident Fund investment. By entering your contribution amount, tenure, and current interest rate, you can project long-term returns and plan your savings effectively.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Mar 02, 2026

Recurring Deposit (RD) Calculator – Returns, Interest & Maturity Guide

An RD Calculator helps you estimate the maturity amount and interest earned on your Recurring Deposit investment. By entering your monthly deposit, tenure, and interest rate, you can project returns and plan your savings effectively.

Priya Nair

Senior Compliance Editor at IFSC.co

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ