IFSC Code Changes: Can They Happen Over Time in Banking?

Does your IFSC code stay the same forever? Learn why bank mergers, relocations, and RBI 2026 updates cause IFSC changes and how to update your records.

Table of Contents

Ah, the unassuming IFSC code. Most of us punch it into our online banking apps without a second thought, assuming it’s as fixed as our account numbers. But what if I told you that this critical piece of financial plumbing isn’t always static? I remember a client calling me in a panic a few years back, their recurring payment had bounced, and the only thing that had changed was their bank’s name due to a merger. It was a stark reminder that the question, “Can IFSC Code change over time in banking system?” is not just hypothetical; it’s a real-world concern that can impact millions of transactions. Understanding its dynamic nature is absolutely crucial for smooth financial operations in India’s ever-evolving banking landscape.

The Immutable Core, Yet Dynamic Nature

At its heart, the Indian Financial System Code (IFSC) is an 11-character alphanumeric code uniquely identifying every bank branch participating in India’s online money transfer systems. Think of it as a digital address for your bank branch, essential for facilitating NEFT (National Electronic Funds Transfer), RTGS (Real Time Gross Settlement), and IMPS (Immediate Payment Service) transactions. Without this precise identifier, funds wouldn’t know where to go, leading to chaos in the digital payments ecosystem. Each character in the code serves a purpose: the first four identify the bank, the fifth is always zero (reserved for future use), and the last six identify the specific branch.

However, despite its critical role in identifying specific branches, the IFSC code is not set in stone indefinitely. It’s tied to the operational existence and structure of a bank branch. When significant changes occur within the banking sector, particularly those involving consolidation or restructuring, the associated IFSC codes can, and often do, undergo revisions. This dynamic aspect is a testament to the Indian banking system’s adaptability, ensuring that the unique identification system remains accurate and reflective of the current organizational structure, even as banks merge or branches relocate.

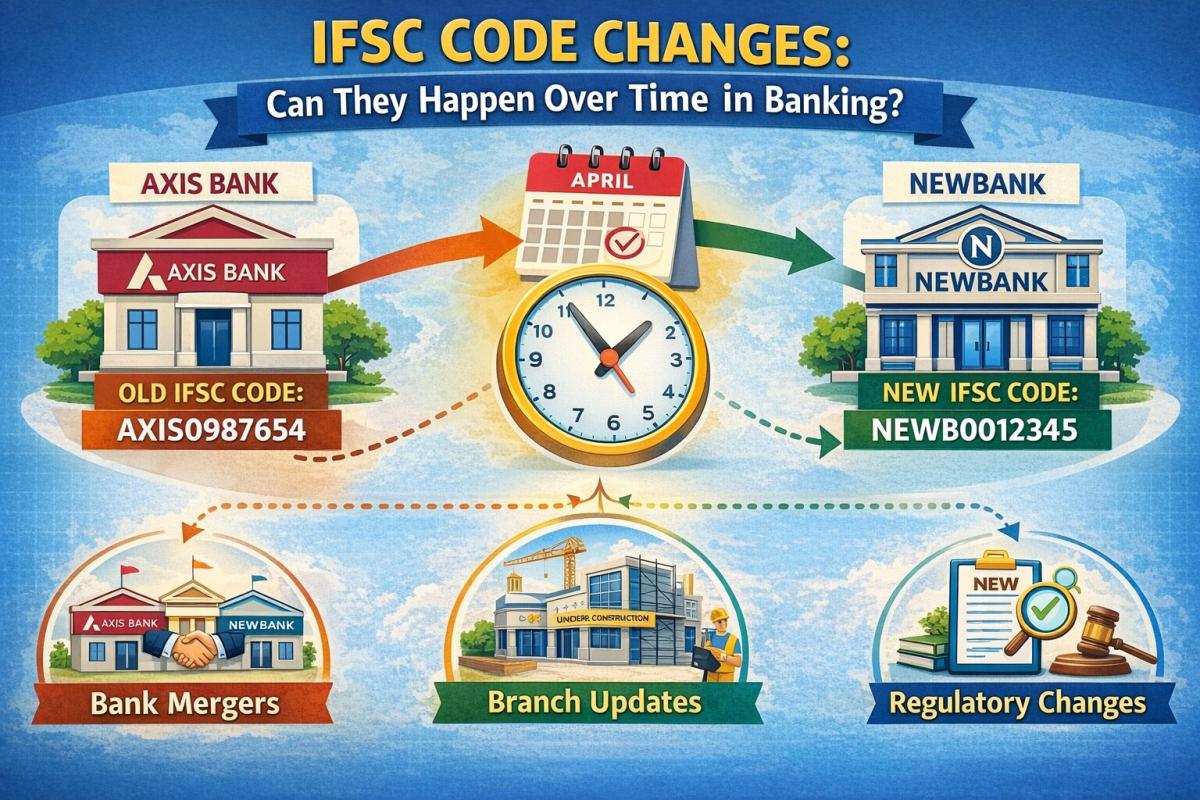

Bank Mergers: A Primary Catalyst for Change

One of the most significant triggers for an IFSC Code change is the consolidation of banks through mergers and acquisitions. We’ve seen a wave of such events in the Indian banking sector over the past decade, aimed at creating larger, more resilient financial institutions. When two or more banks combine, the branches of the acquired or merging entities typically adopt the IFSC code structure of the anchor or acquiring bank. This process isn’t instantaneous but follows a carefully orchestrated transition period, during which customers are usually given ample notice to adapt to the new details.

For example, if Bank A merges with Bank B, all branches previously belonging to Bank B will eventually cease to use their old IFSC codes and be assigned new ones under Bank A’s umbrella. This ensures uniformity across the newly formed larger entity and streamlines interbank transactions. From a customer’s perspective, this means updating their financial records, recurring payment mandates, and communicating the new details to anyone who regularly sends them money. Failing to do so can result in failed transactions, causing inconvenience and potential delays in receiving funds. It’s a crucial update that often gets overlooked.

Branch Relocations and Operational Shifts

Beyond mergers, an IFSC code can also change due to a bank branch’s relocation or significant internal operational restructuring. While less common than merger-driven changes, a physical move from one address to another, even within the same city, can sometimes necessitate a new IFSC code. This is because the code is not just about the bank, but also about the specific geographical identifier of that branch. If the move is substantial enough to warrant a re-evaluation of its identification within the banking network, a new code might be issued by the Reserve Bank of India (RBI).

Furthermore, banks sometimes undertake internal reorganizations that might lead to a branch being re-designated or its operational scope changing dramatically. While less direct a cause, such shifts can occasionally prompt a review and subsequent alteration of its IFSC. It’s a nuanced process, and the decision to issue a new code rests on whether the existing identifier accurately reflects the branch’s current operational reality and location within the broader banking network. The banking system thrives on precision, and any ambiguity in branch identification is usually rectified swiftly.

The RBI’s Oversight in IFSC Changes

The Reserve Bank of India (RBI) plays a pivotal role in regulating and overseeing all IFSC code changes. As the central banking institution, the RBI maintains the master database of all valid IFSC codes in India. Any bank merger, acquisition, or significant branch relocation that necessitates a change in IFSC must be approved and registered with the RBI. This meticulous oversight ensures the integrity and reliability of the entire electronic funds transfer system. Without the RBI’s stamp of approval, no new or altered IFSC code can be considered valid for transactions.

This regulatory framework is designed to protect consumers and maintain stability in the financial markets. The RBI ensures that banks adhere to proper procedures for communicating changes to their customers and updating relevant payment systems. Their involvement provides a layer of trust and standardization, meaning that while an IFSC Code change can occur, it is always a controlled and documented process, not an arbitrary one. It’s a testament to the robust regulatory environment governing India’s financial infrastructure.

Impact on Account Holders and Best Practices

When an IFSC Code change occurs, the primary impact falls on the account holders. Any individual or entity that regularly sends or receives funds from that specific branch needs to update their records. This includes employers processing salaries, government departments disbursing benefits, customers setting up recurring bill payments, and even friends sending money via UPI or net banking. Using an outdated IFSC code will, more often than not, lead to transaction failures, with funds being returned to the sender after a delay.

Banks are generally quite proactive in informing their customers about impending IFSC Code changes through various channels – SMS, email, branch notices, and announcements on their official websites. It’s imperative for account holders to pay attention to these communications. My advice, which I often share with clients, is to proactively check your bank’s official website or contact customer service if you hear about any major banking sector developments, especially bank mergers, that might affect your branch. A quick verification can save a lot of hassle down the line.

Future Outlook and Staying Updated

The Indian banking sector is dynamic, constantly evolving with new technologies, regulations, and market consolidations. As we move towards 2026 and beyond, we can expect this evolution to continue. While the fundamental purpose of the IFSC code will remain, the frequency or nature of changes might adapt. For instance, increasing digitalization could lead to more seamless internal updates, but the need for customer vigilance will likely persist. The core takeaway is that IFSC codes are not immutable; they are living identifiers that reflect the current structure of the financial system.

Therefore, cultivating a habit of periodically verifying the correct IFSC code, especially before setting up new beneficiaries or large transactions, is a best practice I wholeheartedly endorse. Reputable sources like the official RBI website (RBI.org.in) or your bank’s dedicated portal are always the most accurate places to find this information. Don’t rely on old records or third-party sites without cross-verification. Staying informed and proactive is your best defense against potential transaction disruptions caused by an IFSC Code change.

Key Takeaways

- IFSC Codes Are Dynamic: While designed for unique identification, IFSC codes are not permanently fixed and can change over time due to specific banking system events.

- Mergers Are Major Drivers: Bank mergers and acquisitions are the most common reasons for an IFSC Code change, as branches of acquired banks adopt new codes from the acquiring entity.

- RBI Oversees All Changes: The Reserve Bank of India (RBI) rigorously regulates and approves all IFSC code alterations, ensuring system integrity and protecting consumers. For official information, always refer to the RBI website.

- Customer Vigilance is Crucial: Account holders must stay informed about any changes affecting their branch and update their financial records promptly to avoid failed transactions.

Frequently Asked Questions

How do I know if my bank’s IFSC code has changed?

Your bank will typically notify you through various channels such as SMS, email, official website announcements, or notices at the branch itself. It’s always best to check your bank’s official website or contact their customer service directly if you suspect a change or before making important transactions, especially following news of bank mergers.

What happens if I use an old IFSC code?

Using an outdated IFSC code will most likely result in the transaction failing. The funds will usually be returned to the sender’s account, but this process can take some time, causing delays and inconvenience. In rare cases, if the old code routes to a different active branch, funds might be misdirected, though modern systems are robust against this.

Is the IFSC code linked to my account number?

No, the IFSC code is specific to the bank branch where your account is held, not directly to your individual account number. Your account number uniquely identifies your specific account within that branch, while the IFSC code identifies the branch itself within the broader Indian financial system.

Can a bank change its IFSC code without informing customers?

No, banks are legally obligated and operationally compelled to inform their customers about any IFSC Code change well in advance. The Reserve Bank of India (RBI) mandates proper communication protocols to ensure a smooth transition and minimize disruption for account holders. For more details on payment systems, you can check the NPCI website.

Conclusion

So, can the IFSC Code change over time in the banking system? Absolutely, yes. It’s not a static identifier but a dynamic one, reflecting the evolving structure of India’s financial landscape. From major bank mergers to strategic branch relocations, these changes are an integral part of maintaining an accurate and efficient digital payment ecosystem. Staying informed, actively checking for updates from your bank, and exercising a little proactive vigilance will ensure your financial transactions remain smooth and uninterrupted, even as the banking world continues to transform well into 2026.

Related Blogs

Published on Apr 09, 2026

IMPS Transaction Speed: Technical Mechanics Explained

How is IMPS so fast? Discover the technical mechanics behind IMPS transaction speed, including NPCI's central switch and ISO 20022 messaging standards.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Transaction Timeouts in Banking: Unpacking the Root Causes

Why do bank payments timeout? Explore the technical root causes, from database locks to network latency and third-party API failures in our 2026 guide.

Arjun Sharma

Content Lead – Banking & Payments

Published on Mar 30, 2026

BHIM App vs GPay vs PhonePe vs Paytm: Which UPI App Should You Use in 2026?

Confused between BHIM, Google Pay, PhonePe or Paytm, this in-depth guide explains differences, pros and cons, and helps you choose the best UPI app in India based on your usage.

Arjun Sharma

Content Lead – Banking & Payments

Published on Mar 25, 2026

Advantages and Risks of Net Banking

Learn the advantages and risks of net banking, including convenience, speed, and security concerns. Understand how to use online banking safely.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Mar 25, 2026

4 Things you can do with your online banking account

Discover 4 useful things you can do with your online banking account, from paying bills to applying for loans and earning rewards easily.

Arjun Sharma

Content Lead – Banking & Payments

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ