IMPS Transaction Speed: Technical Mechanics Explained

How is IMPS so fast? Discover the technical mechanics behind IMPS transaction speed, including NPCI's central switch and ISO 20022 messaging standards.

Table of Contents

I still vividly remember the days when transferring money between different banks meant waiting hours, sometimes even a full business day, for funds to reflect. It was a frustrating bottleneck in a rapidly digitizing world. That’s why, when the Immediate Payment Service (IMPS) was introduced in India, it wasn’t just another banking product; it was a revolution. Understanding IMPS transaction processing speed, technically, reveals the intricate dance of modern financial infrastructure that enables near-instantaneous money movement. It’s a testament to robust engineering, designed to offer unparalleled convenience and reliability, fundamentally changing how we interact with our finances. This system, from my perspective, truly sets a global benchmark for real-time payments, and its underlying mechanics are far more fascinating than many realize.

The Foundation of Real-Time: NPCI and IMPS

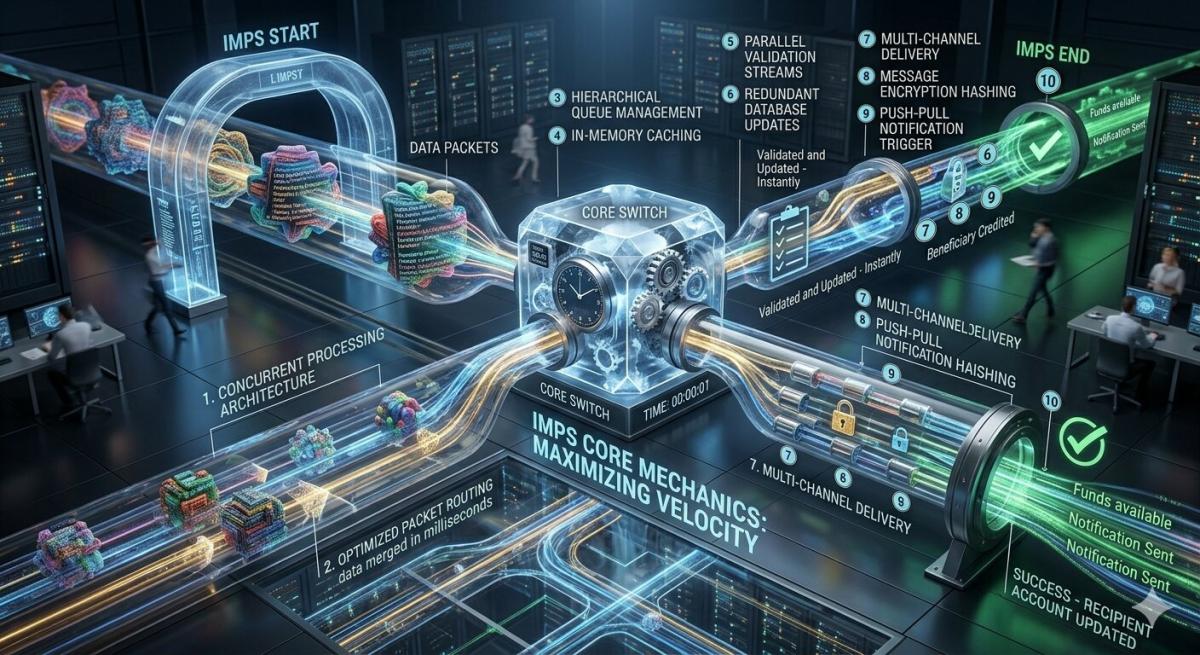

At its core, the remarkable IMPS transaction processing speed is powered by the National Payments Corporation of India (NPCI), an umbrella organization for operating retail payments and settlement systems in India. NPCI acts as the central switch, connecting all participating banks and financial institutions. When you initiate an IMPS transfer, your bank doesn’t directly send money to the recipient’s bank in a peer-to-peer fashion. Instead, both banks communicate with the NPCI’s central server. This centralized architecture is crucial for ensuring consistency, security, and, most importantly, the instantaneous nature of these transactions, distinguishing it from older batch processing systems.

The system is designed for high availability and low latency, critical for its “immediate” promise. NPCI’s infrastructure leverages robust network protocols and sophisticated transaction processing engines that can handle millions of requests per second. From an architectural standpoint, the use of ISO 20022 messaging standards facilitates standardized communication between diverse banking systems, reducing integration complexities and potential points of failure. This standardization is a quiet hero, ensuring that whether you’re using a large public sector bank or a smaller cooperative, the message format for your IMPS transaction remains universally understood and quickly processed by the central switch.

The Technical Flow: From Initiation to Completion

When you initiate an IMPS transaction, say from your mobile banking app, the request first hits your bank’s core banking system. This system validates your credentials, checks your account balance, and then formats the transaction details into a standardized message. This message is then securely transmitted to the NPCI switch. The journey from your phone to your bank’s server and then to NPCI is typically measured in milliseconds, thanks to optimized network infrastructure and dedicated communication channels, often bypassing public internet routes for critical segments.

Upon receiving the message, the NPCI switch performs its magic. It identifies the beneficiary bank based on the account number or mobile number and IFSC code provided, and then routes the transaction request to that bank. The beneficiary bank’s core banking system then validates the recipient’s account details and credits the amount. Finally, a confirmation message is sent back through NPCI to your bank, which then updates your transaction status. This entire round trip, often taking just a few seconds, is a testament to the efficient orchestration of multiple systems, all designed to minimize latency and ensure transaction finality in near real-time.

The Role of Interbank Messaging

The swiftness of IMPS is heavily reliant on an efficient interbank messaging system. Once your initiating bank sends the transaction details to NPCI, NPCI acts as a central hub, forwarding the payment instruction to the beneficiary bank. This communication relies on highly optimized and secure networks, often private leased lines or virtual private networks (VPNs) with robust encryption, ensuring both speed and data integrity. The messages exchanged are not just simple data packets; they contain cryptographic signatures and timestamps, ensuring non-repudiation and an auditable trail, which is crucial for financial transactions. This intricate choreography of data ensures that funds are debited and credited almost simultaneously, providing the real-time experience users expect and depend on in 2026.

Factors Influencing IMPS Speed

While IMPS is designed for near-instantaneous transfers, several technical factors can subtly influence the actual IMPS transaction processing speed. Network latency is a significant one; the speed of data transmission between your device, your bank’s servers, NPCI, and the beneficiary bank can vary based on network congestion or infrastructure quality. Though banks and NPCI use dedicated, high-speed networks, external factors like your internet connection quality can introduce minor delays at the initial and final stages of the transaction. Furthermore, the processing load on core banking systems, especially during peak hours, can also momentarily impact how quickly a transaction is handled, though modern systems are built to scale.

Another critical factor is the internal processing speed of each participating bank’s core banking system. While NPCI processes transactions very quickly, the ultimate credit to the beneficiary’s account depends on their bank’s ability to process the incoming message and update the account ledger. Legacy banking systems, though continuously upgraded, might introduce slightly more overhead compared to newer, cloud-native architectures. However, the regulatory push for real-time payments has largely incentivized banks to invest heavily in modernizing their infrastructure, ensuring that such delays are minimal and rarely noticeable to the end-user. For deeper insights into payment system regulations, the Reserve Bank of India’s website is an invaluable resource.

Security and Reliability: The Unsung Heroes of Speed

The impressive IMPS transaction processing speed wouldn’t mean much without ironclad security and reliability. Every IMPS transaction is encrypted end-to-end, protecting sensitive financial data from interception and tampering. This involves complex cryptographic protocols and secure sockets layer (SSL)/Transport Layer Security (TLS) for data in transit. Furthermore, banks and NPCI employ multi-factor authentication, fraud detection systems, and real-time monitoring to identify and prevent suspicious activities. These security layers operate seamlessly in the background, adding minimal overhead to the transaction time while providing maximum protection against cyber threats, a paramount concern for any financial system.

Reliability is built into the system through redundant infrastructure and robust disaster recovery mechanisms. NPCI, for example, operates multiple data centers with active-active or active-passive configurations, ensuring that even if one facility experiences an outage, transactions can seamlessly switch to another, maintaining continuous service availability. This resilience is vital for a system that processes billions of transactions annually. The meticulous planning and investment in fault-tolerant architecture mean that IMPS is not only fast but also incredibly dependable, a critical factor for financial stability and user trust, especially as we look towards even higher transaction volumes by 2026.

Key Takeaways

- Centralized Hub Architecture: IMPS leverages NPCI as a central switch, enabling direct, standardized communication between all participating banks, which is fundamental to its real-time processing capabilities.

- Technical Efficiency and Standards: The system relies on optimized network infrastructure, ISO 20022 messaging standards, and high-performance transaction processing engines to achieve near-instantaneous debits and credits.

- Factors Affecting Speed: While generally instant, actual speed can be subtly influenced by network latency, the processing load on individual bank core banking systems, and the quality of your personal internet connection.

- Integrated Security and Reliability: End-to-end encryption, multi-factor authentication, fraud detection, and redundant infrastructure are critical components that ensure transactions are not only fast but also secure and highly available.

Frequently Asked Questions

Is IMPS truly instantaneous?

Technically, IMPS transactions are near-instantaneous. While the actual processing by NPCI and interbank messaging takes mere seconds, the time for funds to reflect in a beneficiary account can occasionally be slightly longer due to factors like the beneficiary bank’s internal system load or network conditions. However, the overwhelming majority of transactions complete within a few seconds.

What is the maximum amount I can transfer via IMPS?

The maximum limit for IMPS transfers is currently ₹5,00,000 (five lakh rupees) per transaction. However, individual banks may set lower per-transaction or daily limits based on their internal policies and customer segments. It’s always advisable to check with your specific bank for their applicable limits.

How does IMPS differ from NEFT and RTGS?

IMPS offers immediate, 24×7 real-time fund transfers, even on holidays. NEFT (National Electronic Funds Transfer) operates on an hourly batch settlement system, meaning funds are processed in batches at specific intervals, typically taking a few hours. RTGS (Real Time Gross Settlement) also offers real-time processing but is primarily for large-value transactions (₹2 lakh minimum) and operates during specific banking hours. IMPS is ideal for urgent, smaller to medium-value transfers.

What if an IMPS transaction fails but my account is debited?

If an IMPS transaction fails but your account is debited, the system is designed to automatically reverse the amount to your account, typically within a few minutes to a few hours. This is due to the transaction finality rules and error handling protocols built into the IMPS architecture. If the amount is not reversed within 24 hours, you should contact your bank with the transaction reference number for assistance, though such instances are rare.

Conclusion

The IMPS transaction processing speed is a marvel of modern financial technology, blending speed, security, and accessibility into a seamless user experience. It’s more than just an instant payment system; it’s a meticulously engineered ecosystem that underscores India’s leadership in digital payments. From its centralized NPCI hub to the sophisticated interbank messaging and robust security protocols, every layer is designed for efficiency and reliability. As we look towards 2026 and beyond, the continuous evolution and scaling of IMPS will undoubtedly continue to empower millions, making financial transactions faster, safer, and more convenient than ever before. It’s a system I genuinely admire for its technical prowess and societal impact.

Related Blogs

Published on Apr 09, 2026

IFSC Code Changes: Can They Happen Over Time in Banking?

Does your IFSC code stay the same forever? Learn why bank mergers, relocations, and RBI 2026 updates cause IFSC changes and how to update your records.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Transaction Timeouts in Banking: Unpacking the Root Causes

Why do bank payments timeout? Explore the technical root causes, from database locks to network latency and third-party API failures in our 2026 guide.

Arjun Sharma

Content Lead – Banking & Payments

Published on Mar 30, 2026

BHIM App vs GPay vs PhonePe vs Paytm: Which UPI App Should You Use in 2026?

Confused between BHIM, Google Pay, PhonePe or Paytm, this in-depth guide explains differences, pros and cons, and helps you choose the best UPI app in India based on your usage.

Arjun Sharma

Content Lead – Banking & Payments

Published on Mar 25, 2026

Advantages and Risks of Net Banking

Learn the advantages and risks of net banking, including convenience, speed, and security concerns. Understand how to use online banking safely.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Mar 25, 2026

4 Things you can do with your online banking account

Discover 4 useful things you can do with your online banking account, from paying bills to applying for loans and earning rewards easily.

Arjun Sharma

Content Lead – Banking & Payments

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ