The Difference Between IFSC, MICR, and SWIFT Codes: When to Use Which?

Master IFSC, MICR, and SWIFT codes in 2026. Learn their differences, when to use each, and avoid transaction failures with our expert guide.

Table of Contents

- Before vs. After: The 2026 Banking Landscape

- 1. IFSC: The Digital Address (Domestic Only)

- 2. MICR: The Paper-Trail Tech

- 3. SWIFT: The Passport for Your Money

- The 2026 Twist: ISO 20022 Compliance

- Impact on Your Daily Life

- Actionable Checklist: What You Need to Do Immediately

- Frequently Asked Questions (FAQ)

In the rapidly evolving landscape of Indian digital banking, 2026 marks a pivotal year. With the Reserve Bank of India (RBI) finalizing the Master Direction on Regulatory Consolidation, and the successful implementation of the T+3 Hour Cheque Clearing framework this January, the "identifiers" we use to move money have never been more critical.

For the last decade, you might have gotten away with using an old IFSC from a pre-merger passbook or a slightly outdated SWIFT code. That grace period is officially over.

Whether you are setting up a new SIP, receiving freelance payments from London, or paying your rent via NEFT, the codes—IFSC, MICR, and SWIFT—are the GPS coordinates of your money. Under the new RBI Risk-Based Authentication (2025-26) protocols, using an obsolete code doesn't just mean a delay; it can lead to immediate transaction reversals or "frozen" payment status to prevent fraud.

Here is your definitive, expert guide to navigating these codes in the current banking era.

Before vs. After: The 2026 Banking Landscape

The merger of banks like Oriental Bank of Commerce into PNB or Allahabad Bank into Indian Bank is now technically ancient history. However, 2026 is the year the "backend" completely changed.

|

Feature |

Old Rules (Pre-2025) |

New Rules (Effective 2026) |

|

Legacy IFSC Codes |

Old merged bank codes were often "mapped" or redirected by systems. |

Strict Rejection: Only the anchor bank's current IFSC is valid. |

|

Cheque Clearing |

Standard CTS-2010 processing (24-48 hours). |

T+3 Hour Clearing: High-speed scanning requires valid MICR; no manual overrides. |

|

International Payouts |

SWIFT was the primary identifier. |

SWIFT + ISO 20022: Structured address data is now mandatory for all cross-border flows. |

|

Validation |

Manual entry errors often "bounced" days later. |

Real-time Lookup: API-based beneficiary name & code matching before the money leaves. |

1. IFSC: The Digital Address (Domestic Only)

The Indian Financial System Code (IFSC) is an 11-character alphanumeric string that is the backbone of NEFT, RTGS, and IMPS.

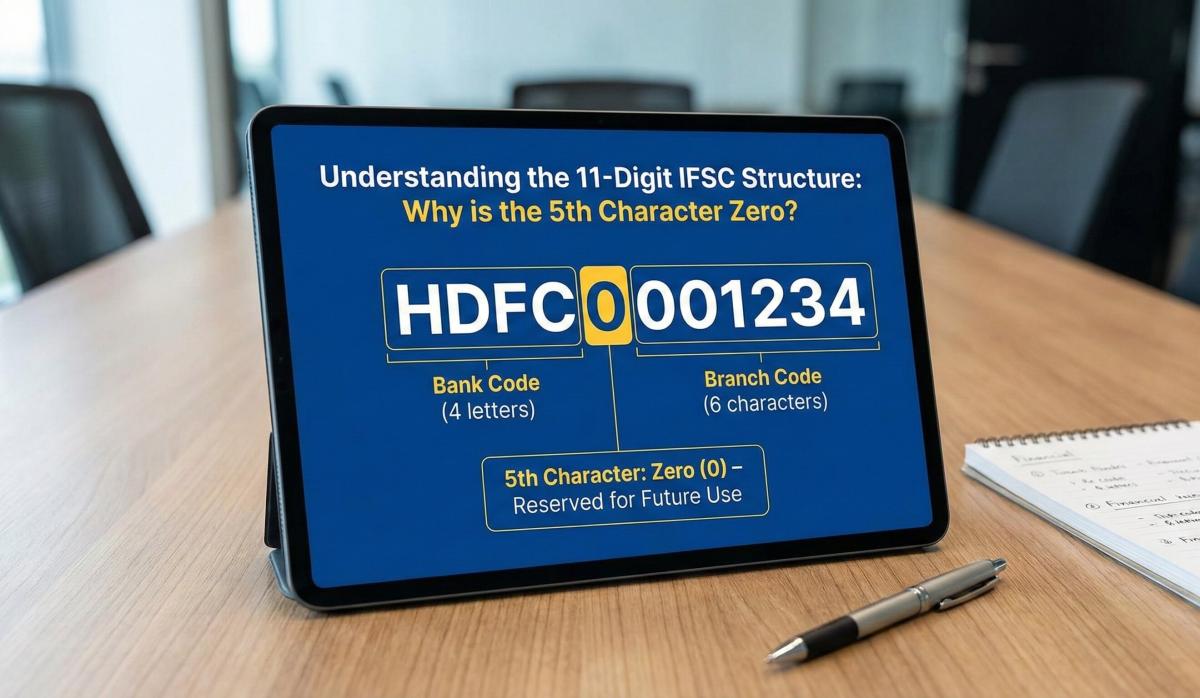

The Anatomy of an IFSC: Why is the 5th Character '0'?

Every IFSC follows a strict pattern: BANK 0 BRANCH.

- First 4 Characters: Represent the bank (e.g., SBIN for SBI, HDFC for HDFC Bank).

- 5th Character: This is always '0' (Zero). It was reserved by the RBI for future expansion. Despite the digital explosion of the last decade, this remains a placeholder to ensure the system can handle billions of unique branch combinations without breaking the code structure.

- Last 6 Characters: Define the specific branch location.

Regulatory Alert (2026): As per the RBI Digital Payment Security Directions, effective April 2026, banks must now perform a "Beneficiary Name Match". If you enter a correct IFSC but the name on the account doesn't match the new post-merger database (e.g., "Syndicate Bank" instead of "Canara Bank"), the transaction will trigger a risk alert.

When to use it: Use IFSC for any electronic transfer within India. It tells the RBI's central server exactly which digital "pigeonhole" the money should land in.

2. MICR: The Paper-Trail Tech

While IFSC is for the digital world, Magnetic Ink Character Recognition (MICR) is for the physical world. It is a 9-digit numeric code found at the bottom of your cheque leaf, printed in a unique font that can be read by magnetic scanners even if the cheque is crumpled or stained.

- Digits 1-3: City Code (aligns with the first three digits of your PIN code).

- Digits 4-6: Bank Code.

- Digits 7-9: Branch Code.

When to use it: You need MICR primarily for Cheque Clearing and ECS (Electronic Clearing Service).

The 2026 "Speed" Impact:

Previously, if a MICR code was slightly smudged or outdated, a human officer might manually clear it during the 2-day processing window.

As of January 3, 2026, the RBI moved to Continuous Cheque Clearing (Phase 2). Cheques are now processed in 3-hour windows. Automated scanners accept or reject instruments instantly. If your cheque book predates your bank's latest system integration, it will be rejected as "Non-Compliant Instrument" immediately.

3. SWIFT: The Passport for Your Money

The Society for Worldwide Interbank Financial Telecommunication (SWIFT) code (also known as a BIC - Bank Identifier Code) is what you need for international transactions.

- Structure: 8 or 11 characters.

- First 4: Bank Code (e.g., CITI).

- Next 2: Country Code (e.g., IN for India).

- Next 2: Location Code (e.g., BB for Mumbai).

- Last 3 (Optional): Branch Code.

The 2026 Twist: ISO 20022 Compliance

The biggest change you need to know about right now is the global shift to ISO 20022.

As of November 2025, the global banking system (SWIFT) stopped supporting "unstructured" messages.

- What this means for you: You can no longer just give a friend in New York your name and SWIFT code. You must provide your Full Structured Address (House No, Street, City, Pin) that matches your bank records exactly. If the address data is missing or vague, the incoming funds will be blocked by the intermediary bank before they even reach India.

When to use it: Only for cross-border transfers. Do not use SWIFT for domestic transfers; it will fail.

Impact on Your Daily Life

You might think these codes only matter when you fill out a form, but in 2026, they affect your automated financial life:

- EMIs & Auto-Debits (NACH): If you have an old auto-debit set up for a Home Loan using a MICR from a merged entity (e.g., Vijaya Bank), the National Automated Clearing House (NACH) 3.0 update may finally reject it this year. You need to submit a "Modification Form" with your new bank's MICR.

- Income Tax Refunds: The Income Tax Department has migrated to a "Validated Account Only" refund system. If your IFSC on the e-filing portal hasn't been updated to the new anchor bank's code, your refund will stay "pending" indefinitely.

- Salary Credits: HR systems now validate beneficiary details in real-time. If your employee portal has an old IFSC, the payroll software will likely refuse to process the payout to prevent a "credit return" fee.

Actionable Checklist: What You Need to Do Immediately

- Audit Your Checkbook: Look at the cheque leaf. If the bank logo is from a pre-merger entity (e.g., United Bank of India, Lakshmi Vilas Bank), destroy it. The 2026 clearing scanners will not accept it. Order a new one via your app today.

- Verify the 5th Digit: When adding a beneficiary, always double-check that the 5th character of the IFSC is a Zero (0) and not the letter 'O'. This remains the #1 cause of failed IMPS transactions.

- Update "Me-to-Me" Transfers: If you transfer money between your own accounts (e.g., Salary Account -> Savings Account), delete the old beneficiary entry and re-add it with the fresh IFSC to ensure it complies with the new "Name Match" rules.

- Ask for "Structured" SWIFT Details: If you receive money from abroad, ask your branch specifically for their "ISO 20022 Compliant Inward Remittance Instructions." This will ensure you get the exact address format needed to avoid delays.

Frequently Asked Questions (FAQ)

1. Can I use my old IFSC code if my bank merged three years ago?

No. While there was a "sunset period," as of 2026, the old systems are largely decommissioned. Using a legacy IFSC (like ALLA for Allahabad Bank) will result in an "Invalid Bank Code" error immediately.

2. Is the SWIFT code the same as the IFSC code?

No. IFSC is for Domestic (within India) and SWIFT is for International (cross-border). You cannot use an IFSC to receive money from the USA, and you cannot use SWIFT to pay your landlord in Mumbai.

3. Where can I find my MICR code if I don't have a checkbook?

It is usually available in your Mobile Banking App under "Account Details" or "Nominee & Passbook" section. It is also printed on the first page of your physical passbook.

4. Why did my transaction fail even though the IFSC was correct?

Under the 2026 Risk-Based Authentication rules, if the "Beneficiary Name" you entered does not match the name registered with that IFSC at the receiving bank, the transaction may be blocked to prevent fraud. Ensure the name matches exactly.

5. Does a change in IFSC mean my account number also changes?

Usually, no. In most Indian bank mergers, account numbers remained the same to minimize disruption, but the IFSC and MICR were updated to reflect the new parent entity's routing.

Related Blogs

Published on Mar 09, 2026

NEFT vs RTGS vs IMPS vs UPI: Which Transfer Method Should You Use?

NEFT, RTGS, IMPS, or UPI — which transfer method should you use? Compare limits, timing, charges and best use cases. Full guide with 2025 RBI & NPCI figures.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Aug 09, 2025

What to Do if You Transfer Money to the Wrong IFSC Code: A Recovery Guide

Money sent to wrong IFSC? Don't panic! Learn what steps to take immediately to recover your funds and prevent future mistakes.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Jul 27, 2025

Understanding the 11-Digit IFSC Structure: Why the Fifth Character is Always Zero

Decode the IFSC structure! Understand why the 5th character is always zero and what each digit means for fund transfers.

Arjun Sharma

Content Lead – Banking & Payments

Published on Jul 14, 2025

The Role of the Reserve Bank of India (RBI) in Regulating Digital Payment Codes

Learn how the RBI regulates digital payment codes like IFSC, UPI, and SWIFT. Understand compliance and security in Indian banking.

Arjun Sharma

Content Lead – Banking & Payments

Published on Jul 12, 2025

SBI Net Banking Registration 2026: The "No-Nonsense" Guide for New Users

New to banking? This practical guide covers essentials like accounts, cards, digital banking, and safety tips for Indian users.

Priya Nair

Senior Compliance Editor at IFSC.co

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

A Comprehensive Guide to Home Loan Interest Rates: Fixed vs. Floating in 2026

A detailed 2026 guide to home loan interest rates comparing fixed, floating, and hybrid options. Learn the real cost difference, EMI impact, risks, RBI policies, and which option saves you more over 20 years.

EMI & Loans • 8 MINS READ

Mutual Fund Returns Calculator: How It Works, Accuracy & FAQs Explained

A Mutual Fund Returns Calculator helps you estimate the future value of your mutual fund investment using inputs like investment amount, tenure, contributions, and expected returns. It uses compounding to project potential growth and helps you plan smarter investment decisions.

SIP & Investing • 6 MINS READ

NEFT vs RTGS vs IMPS vs UPI: Which Transfer Method Should You Use?

NEFT, RTGS, IMPS, or UPI — which transfer method should you use? Compare limits, timing, charges and best use cases. Full guide with 2025 RBI & NPCI figures.

Banking & Transfers • 16 MINS READ

New Tax Regime vs Old Tax Regime: A Real-Numbers Comparison for Salaried Indians (FY 2025-26)

New vs old tax regime FY 2025-26 — compare real tax on ₹6L, ₹10L & ₹15L salaries. See who pays zero tax and find your break-even point.

Tax & Financial Planning • 15 MINS READ

Planning an FD? Don’t Miss These Top Questions About FD Calculators

Curious how FD calculators work? This guide answers the top questions to help you calculate returns, compare plans, and invest smarter in fixed deposits.

FD, PPF & Savings • 5 MINS READ