Understanding the 11-Digit IFSC Structure: Why the Fifth Character is Always Zero

Decode the IFSC structure! Understand why the 5th character is always zero and what each digit means for fund transfers.

Table of Contents

How many times have you squinted at your phone screen, trying to figure out if that character in the middle of an IFSC code is the letter 'O' or the number '0'?

Here is the deal—it is always the number zero.

In the high-speed world of 2026 digital banking, where the RBI has just rolled out stricter Risk-Based Authentication (RBA) protocols, getting this wrong isn't just a typo—it’s a transaction failure waiting to happen. Whether you are setting up a new SIP, transferring rent, or approving an auto-debit, that tiny '0' plays a massive role in the Indian banking backbone.

Today, we are decoding the 11-digit Indian Financial System Code (IFSC), specifically focusing on why that fifth character is a zero, and why this knowledge is critical for your financial health in 2026.

The 2026 Landscape: Why This Matters Now

As of April 2026, the Indian banking sector has stabilized after the massive "Mega Merger" waves that consolidated 27 Public Sector Banks (PSBs) into just 12. If you are still holding onto an old chequebook from a pre-merger bank (like Syndicate Bank or Allahabad Bank), your payments will bounce. The RBI's new April 2026 Payment Settlement Directive has made the validation of beneficiary details stricter than ever to prevent fraud.

Before vs. After: The Merger Impact

If you are using an old IFSC code, you are routing money to a "ghost" branch. Here is a quick look at how codes have shifted for major banks:

|

Bank (Pre-Merger) |

Old IFSC Example |

New Parent Bank |

New IFSC Example |

Status in 2026 |

|

Syndicate Bank |

SYNB0002407 |

Canara Bank |

CNRB0002407 |

Active |

|

Allahabad Bank |

ALLA0210217 |

Indian Bank |

IDIB000A632 |

Active |

|

Oriental Bank (OBC) |

ORBC0100222 |

Punjab National Bank |

PUNB0100222 |

Active |

|

United Bank of India |

UTBI0RUB567 |

Punjab National Bank |

PUNB0RUB567 |

Active |

|

Corporation Bank |

CORP0000456 |

Union Bank of India |

UBIN0900456 |

Active |

Regulatory Alert: As per the RBI's 2026 Master Direction on Digital Payments, transactions initiated with invalid or retired IFSC codes are no longer auto-reversed instantly. The refund process now involves a T+3 day reconciliation window. Accuracy is your only defense against locked funds.

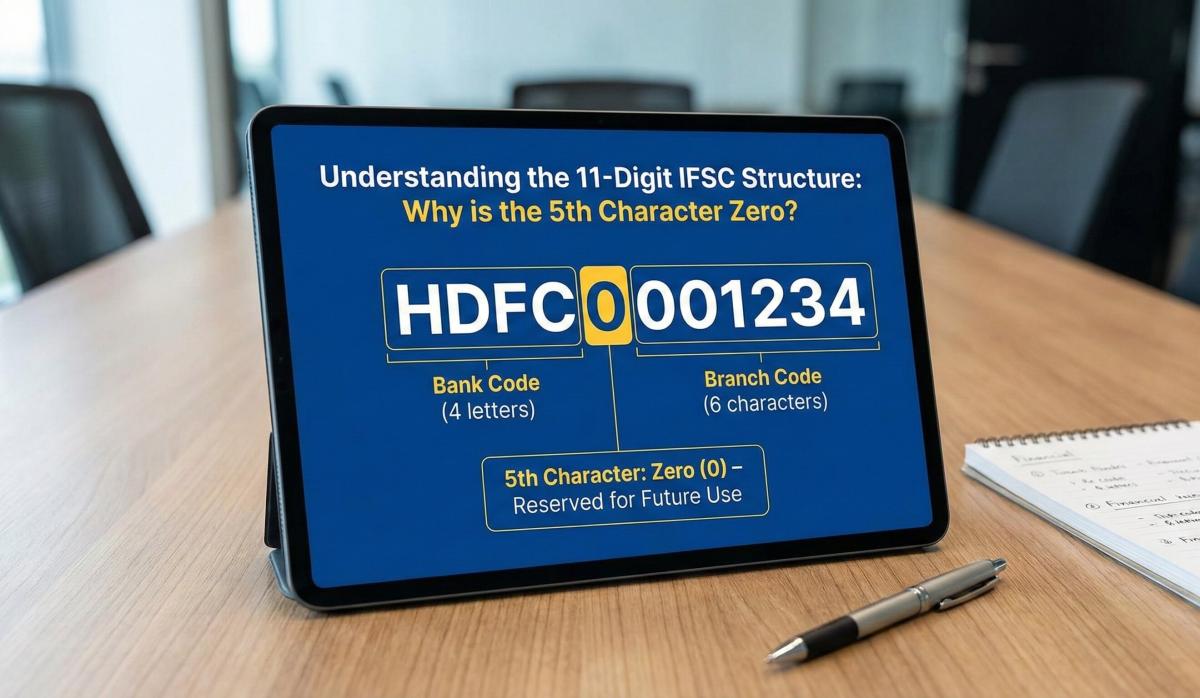

Deep Dive: The Anatomy of an 11-Digit IFSC

The IFSC is not just a random string of characters; it is a logical address for your money. It is divided into three distinct parts:

[ A A A A ] [ 0 ] [ 1 2 3 4 5 6 ]

1. First 4 Characters: The Bank Code

This represents the bank's name.

- SBIN = State Bank of India

- HDFC = HDFC Bank

- ICIC = ICICI Bank

- CNRB = Canara Bank

2. The 5th Character: The "Central Switch" (Always Zero)

This is the source of all confusion. The fifth character is always the digit 0 (Zero).

Why is it Zero?

- Future Proofing: When the system was designed, the RBI anticipated that the number of branches in India might one day explode beyond what a 6-digit branch code could handle. The '0' is a placeholder. If we ever run out of branch codes in the last 6 digits, the RBI can change this '0' to a '1' or 'A' to create a whole new set of possibilities.

- Control Character: In tech terms, it acts as a "separator" or a control check that helps banking software differentiate between the bank name and the specific branch location.

- Standardization: It ensures that every single IFSC code in India follows the exact same 4-1-6 format, making it easier for computer systems to validate transfers instantly.

3. Last 6 Characters: The Branch Code

These denote the specific physical branch.

- They are usually numeric (e.g., 000123) but can be alphanumeric (e.g., 00A123) to accommodate more branches.

- Note: For many banks, the branch code matches the MICR code's last digits, but not always.

Impact on Your Daily Life in 2026

You might think, "Who cares about a zero?" But in the current financial ecosystem, this single digit affects you more than you realize.

1. The "O" vs. "0" Error in Beneficiary Setup

When adding a beneficiary on a mobile banking app, the most common error code (Error 909) is "Invalid IFSC Format." This almost always happens because users type the capital letter 'O' instead of the number '0'.

- Consequence: In 2026, banking apps with Real-Time Account Validation will reject this instantly. However, if you are filling out a physical NEFT/RTGS form at a branch, a handwriting error can cause your money to be stuck in a suspense account for days.

2. EMI and SIP Rejections

If you have set up an older NACH (National Automated Clearing House) mandate using a pre-merger IFSC, it might have worked for a grace period. That grace period is largely over in 2026.

- Scenario: Your Home Loan EMI bounces because the underlying IFSC (e.g., from Dena Bank) is now invalid.

- Result: You get hit with a "Cheque Bounce" penalty (approx. ₹500 + GST) and a hit to your CIBIL score.

3. International Remittances

When receiving money from abroad (via SWIFT), the foreign bank requires your exact branch IFSC to route the money locally in India. Foreign keyboards and banking systems often don't have the same validation checks as Indian apps. If the sender types 'O', the SWIFT message may fail to decode at the RBI gateway, delaying your funds by weeks.

Actionable Checklist: What You Need to Do Immediately

Trust me on this—spending 10 minutes on this list today can save you weeks of headache.

- Audit Your Payees: Open your net banking and delete any beneficiaries from merged banks (e.g., Syndicate, Allahabad, Dena). Re-add them with their new IFSCs.

- Check Your Chequebook: If your cheque leaves still bear the old bank's name or IFSC, destroy them. Request a new chequebook via your banking app immediately.

- Update SIPs/Mutual Funds: Log in to CAMS or KFintech and check your registered bank mandates. If they show an old IFSC, submit a "Change of Bank Mandate" form.

- Verify Before Sending: Use the IFSC Search Tool on ifsc.co before making any transfer above ₹10,000. We update our database daily to reflect the latest RBI changes.

Frequently Asked Questions (FAQ)

Q1: Will the 5th character ever change from 0?

Answer: Currently, it remains 0 for all banks. The RBI has reserved it for future use, meaning it could change if the banking network grows massively, but as of 2026, it is strictly zero.

Q2: I accidentally typed 'O' instead of '0' for a transfer. What happens?

Answer: Most modern banking apps will give you an "Invalid Format" error and stop you. However, if you wrote it on a physical paper form, the bank clerk might misinterpret it, leading to a rejection of the transfer.

Q3: Can I still use my Syndicate Bank cheque in 2026?

Answer: No. Syndicate Bank has fully merged into Canara Bank. Old cheques are no longer valid legal tender for clearing. You must use a Canara Bank cheque with the new CNRB IFSC code.

Q4: Does the IFSC code change if I move my account to a different branch?

Answer: Yes! The IFSC represents the branch, not just the bank. If you transfer your home branch from Mumbai to Delhi, your account number might stay the same, but your IFSC code will change.

Q5: How do I find the correct IFSC for a merged bank branch?

Answer: Do not guess. Visit the official website of the parent bank (e.g., PNB or Canara Bank) or use a trusted directory like ifsc.co. Look for the "Amalgamated IFSC Mapping" list to find your new code.

Conclusion

The 11-digit IFSC is the DNA of your transaction. While the system is complex, the rule for the 5th character is simple: It is always zero. In the tightening regulatory environment of 2026, ensuring your codes are accurate is the smartest financial habit you can build.

Related Blogs

Published on Mar 09, 2026

NEFT vs RTGS vs IMPS vs UPI: Which Transfer Method Should You Use?

NEFT, RTGS, IMPS, or UPI — which transfer method should you use? Compare limits, timing, charges and best use cases. Full guide with 2025 RBI & NPCI figures.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Aug 09, 2025

What to Do if You Transfer Money to the Wrong IFSC Code: A Recovery Guide

Money sent to wrong IFSC? Don't panic! Learn what steps to take immediately to recover your funds and prevent future mistakes.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Jul 14, 2025

The Role of the Reserve Bank of India (RBI) in Regulating Digital Payment Codes

Learn how the RBI regulates digital payment codes like IFSC, UPI, and SWIFT. Understand compliance and security in Indian banking.

Arjun Sharma

Content Lead – Banking & Payments

Published on Jul 12, 2025

SBI Net Banking Registration 2026: The "No-Nonsense" Guide for New Users

New to banking? This practical guide covers essentials like accounts, cards, digital banking, and safety tips for Indian users.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Jul 08, 2025

The Impact of 2025-2026 Bank Mergers on Your Old IFSC and Branch Details

Understand how bank mergers in 2025-2026 affect IFSC codes and branch details. Update your banking information to avoid transaction failures.

Priya Nair

Senior Compliance Editor at IFSC.co

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

A Comprehensive Guide to Home Loan Interest Rates: Fixed vs. Floating in 2026

A detailed 2026 guide to home loan interest rates comparing fixed, floating, and hybrid options. Learn the real cost difference, EMI impact, risks, RBI policies, and which option saves you more over 20 years.

EMI & Loans • 8 MINS READ

Mutual Fund Returns Calculator: How It Works, Accuracy & FAQs Explained

A Mutual Fund Returns Calculator helps you estimate the future value of your mutual fund investment using inputs like investment amount, tenure, contributions, and expected returns. It uses compounding to project potential growth and helps you plan smarter investment decisions.

SIP & Investing • 6 MINS READ

NEFT vs RTGS vs IMPS vs UPI: Which Transfer Method Should You Use?

NEFT, RTGS, IMPS, or UPI — which transfer method should you use? Compare limits, timing, charges and best use cases. Full guide with 2025 RBI & NPCI figures.

Banking & Transfers • 16 MINS READ

New Tax Regime vs Old Tax Regime: A Real-Numbers Comparison for Salaried Indians (FY 2025-26)

New vs old tax regime FY 2025-26 — compare real tax on ₹6L, ₹10L & ₹15L salaries. See who pays zero tax and find your break-even point.

Tax & Financial Planning • 15 MINS READ

Planning an FD? Don’t Miss These Top Questions About FD Calculators

Curious how FD calculators work? This guide answers the top questions to help you calculate returns, compare plans, and invest smarter in fixed deposits.

FD, PPF & Savings • 5 MINS READ