The Role of the Reserve Bank of India (RBI) in Regulating Digital Payment Codes

Learn how the RBI regulates digital payment codes like IFSC, UPI, and SWIFT. Understand compliance and security in Indian banking.

Table of Contents

If you have ever wondered why your money reaches a vendor in Mumbai and not a stranger in Chennai within seconds, the answer isn’t just "the internet." It is a rigid, highly surveilled framework of digital codes managed by one entity: the Reserve Bank of India (RBI).

In 2026, the RBI is no longer just the printer of currency notes; it is the traffic controller of the world's largest real-time payment ecosystem. With the recent implementation of the Payment Vision 2028 roadmap and the Master Direction on Digital Payment Security (April 2026), the Central Bank has fundamentally changed how payment codes like IFSC, MICR, and LEI operate.

Gone are the days when these codes were static labels. Today, they are dynamic security tools. If you are still treating your IFSC code as a simple "branch address," you are missing the bigger picture—and potentially putting your transactions at risk.

Here is a deep dive into how the RBI regulates the DNA of your money transfers in 2026.

Before vs. After: The RBI’s Regulatory Shift (2020–2026)

The last five years have seen a massive shift from "Post-Facto Settlement" (fixing errors after they happen) to "Pre-Transaction Validation" (stopping errors before they start).

|

Feature |

Old Regulatory Era (Pre-2025) |

New Regulatory Era (2026 Standards) |

|

Code Validation |

Passive. IFSC syntax checked; name matching was optional. |

Active & Mandatory. "Beneficiary Name Lookup" is now required via API before transfer initiation. |

|

Merger Management |

Codes remained active for years post-merger (e.g., e-UBI codes). |

Strict Sunset Clauses. RBI now mandates a "Hard Stop" on legacy codes 12 months post-merger. |

|

Fraud Detection |

Reactive. Fraud reported to RBI after money was lost. |

Predictive. The "Daksh" supervision system flags suspicious routing codes in real-time. |

|

Cross-Border |

SWIFT used largely independently of domestic identifiers. |

Interlinked. RBI has harmonized LEI (Legal Entity Identifier) with domestic NEFT/RTGS for large value txns. |

Deep Dive: The Science Behind the Codes

Why does the RBI care so much about an 11-character string? Because in a digital economy, Standardization = Trust.

1. The IFSC: The RBI’s "Digital Pin Code"

The Indian Financial System Code (IFSC) is not generated by your bank; it is allocated by the RBI under the Electronic Fund Transfer (EFT) System Regulations.

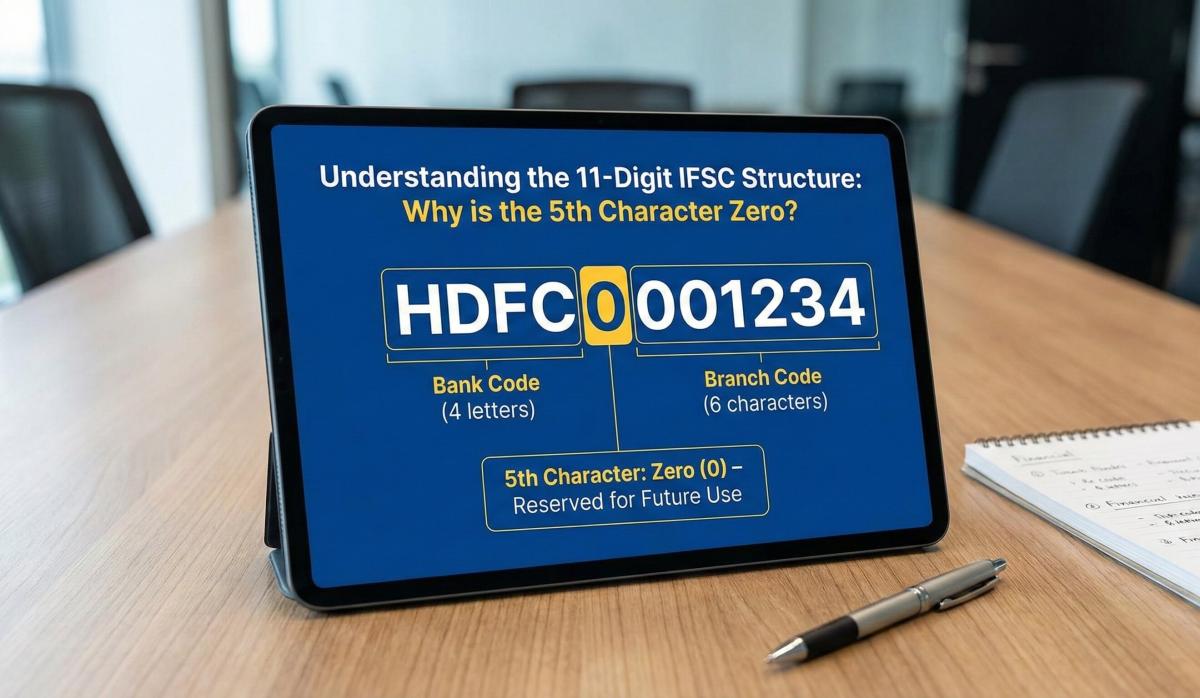

- The "Zero" Logic: You’ve noticed the 5th character is always ‘0’. This isn’t random. The RBI mandated this in the early 2000s as a "reserved buffer."

- In 2026 Context: We are finally seeing why. With the launch of Digital Banking Units (DBUs) that have no physical brick-and-mortar existence, the RBI is utilizing this buffer logic to assign virtual routing codes that distinguish "Neo-Banks" from traditional branches without breaking the legacy 11-character architecture.

2. MICR: The Legacy Sentinel

Even in 2026, the RBI strictly regulates Magnetic Ink Character Recognition (MICR) standards under the CTS-2010 (and now CTS-2025) guidelines.

- The Regulation: The RBI dictates the specific "magnetic signal strength" of the ink used on your cheque. If a bank tries to cut costs with cheap ink, the RBI’s central processing centers (managed by NPCI) will reject the batch. This ensures that the automated sorting machines—which now run at triple the speed of 2020—don’t jam or misread data.

3. LEI: The New Heavyweight

For business owners reading this, the RBI’s push for the Legal Entity Identifier (LEI) is the biggest change.

- The Rule: As of 2026, the RBI mandates that any non-individual entity transferring above ₹5 Crores (internationally or domestically via RTGS) must map their transaction to a 20-digit global LEI code. This is to prevent "Shell Companies" from moving black money through the banking arteries.

Impact on User: Why This Matters to You

You might think, "I'm just paying my electricity bill, why do I care about RBI backend rules?"

Because the RBI’s tightening of code regulations directly impacts your transaction success rate.

- The "Positive Pay" Impact:

If you issue a cheque above ₹50,000, you are now often required to digitally re-confirm the MICR and beneficiary details to the bank. This is an RBI mandate. If you don't, and the cheque is presented via the high-speed CTS-2026 clearing grid, it will be dishonored.

- The "Freezing" of Old Mandates:

Do you have an old SIP or insurance premium auto-debit set up in 2018? If that mandate uses an IFSC from a bank that has since merged (like the old Syndicate Bank), the RBI’s 2026 "Clean Slate" directive means those mandates will start bouncing this year. You cannot blame the bank; they are following the Central Bank's order to purge "Zombie Codes."

- Real-Time Name Validation:

When you add a beneficiary in 2026, you might notice a small "Verified" tick mark appear next to their name. This is the RBI’s Centralised Mapper at work. It confirms that the Account Number + IFSC combination actually belongs to "Rahul Kumar" and not a fraudster. If you override this warning, you lose your right to grievance redressal.

IFSC Relevance: The "Centralised" Truth

A common misconception is that branch managers assign IFSC codes. They do not.

The RBI Department of Payment and Settlement Systems (DPSS) maintains the master list.

- Creation: When a bank opens a new branch, it applies to the RBI.

- Validation: The RBI verifies the branch has the secure "Leased Line" connectivity to the IDRBT (Institute for Development and Research in Banking Technology) network.

- Activation: Only then is an IFSC generated and pushed to the Global Routing Table.

Regulatory Alert: In 2026, simply finding an IFSC on Google is risky. Third-party sites often have "cached" data. The RBI has strictly warned that banks are only liable for transfers made using codes verified on their own platforms or the official NPCI/RBI repository.

Actionable Checklist: The 2026 Compliance Audit

To stay on the right side of RBI’s strict new digital norms, here is your immediate to-do list:

- Check Your "Saved Beneficiaries": Go through your net banking list. If you see any grayed-out names or "Invalid IFSC" tags, delete them. Do not try to edit them; delete and re-add to trigger the new 2026 Verification API.

- Review Loan Mandates: If your Home Loan EMI is deducted via ECS/NACH, check your loan statement. If the "Debit Bank" details show a legacy bank name, file a "Mandate Update Form" immediately to avoid bounce charges.

- Business Owners - Get LEI: If you run a company and plan to send large payments, apply for your Legal Entity Identifier via the CCIL (Clearing Corporation of India). Without it, your RTGS transactions will be blocked by the RBI firewall.

- Download the "RBI Kehta Hai" 2026 App: The RBI now has a consumer-facing app that allows you to instantly verify if a specific digital lending app or payment code is authorized or blacklisted.

Frequently Asked Questions (FAQ)

1. Does the RBI directly refund me if I send money to a wrong IFSC?

No. The RBI acts as the regulator/referee, not the player. They set the rules for grievance redressal (the Ombudsman Scheme), but you must file the complaint with your bank first. If the bank fails to resolve it within 30 days, then you approach the RBI Ombudsman.

2. Why did the RBI deactivate my old chequebook?

Under the CTS-2026 efficiency standards, old cheque leaves (Non-CTS 2010 standards) cannot be read by the new AI-driven sorting machines. Allowing them would slow down the entire national clearing grid, so they are banned.

3. Can a bank change its IFSC code without RBI permission?

Never. An IFSC is a sovereign identifier issued by the Central Bank. A bank can request a change (usually during a merger or relocation), but only the RBI can approve and broadcast the new code to the payment network.

4. What is the "5th Digit" rule I keep hearing about?

It is the standard that the 5th character of an IFSC must be ‘0’ (Zero). If you see a code with an alphabet ‘O’ or any other number there, it is invalid and likely a scam attempt or a typo. The RBI hard-coded this rule into the NEFT/RTGS software to prevent errors.

5. How often does the RBI update the master list of IFSC codes?

In 2026, the update is near real-time. Previously, it was a monthly Excel sheet update. Now, via APIs, a new branch code is live across the payment network within hours of RBI authorization.

Related Blogs

Published on Mar 09, 2026

NEFT vs RTGS vs IMPS vs UPI: Which Transfer Method Should You Use?

NEFT, RTGS, IMPS, or UPI — which transfer method should you use? Compare limits, timing, charges and best use cases. Full guide with 2025 RBI & NPCI figures.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Aug 09, 2025

What to Do if You Transfer Money to the Wrong IFSC Code: A Recovery Guide

Money sent to wrong IFSC? Don't panic! Learn what steps to take immediately to recover your funds and prevent future mistakes.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Jul 27, 2025

Understanding the 11-Digit IFSC Structure: Why the Fifth Character is Always Zero

Decode the IFSC structure! Understand why the 5th character is always zero and what each digit means for fund transfers.

Arjun Sharma

Content Lead – Banking & Payments

Published on Jul 12, 2025

SBI Net Banking Registration 2026: The "No-Nonsense" Guide for New Users

New to banking? This practical guide covers essentials like accounts, cards, digital banking, and safety tips for Indian users.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Jul 08, 2025

The Impact of 2025-2026 Bank Mergers on Your Old IFSC and Branch Details

Understand how bank mergers in 2025-2026 affect IFSC codes and branch details. Update your banking information to avoid transaction failures.

Priya Nair

Senior Compliance Editor at IFSC.co

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

A Comprehensive Guide to Home Loan Interest Rates: Fixed vs. Floating in 2026

A detailed 2026 guide to home loan interest rates comparing fixed, floating, and hybrid options. Learn the real cost difference, EMI impact, risks, RBI policies, and which option saves you more over 20 years.

EMI & Loans • 8 MINS READ

Mutual Fund Returns Calculator: How It Works, Accuracy & FAQs Explained

A Mutual Fund Returns Calculator helps you estimate the future value of your mutual fund investment using inputs like investment amount, tenure, contributions, and expected returns. It uses compounding to project potential growth and helps you plan smarter investment decisions.

SIP & Investing • 6 MINS READ

NEFT vs RTGS vs IMPS vs UPI: Which Transfer Method Should You Use?

NEFT, RTGS, IMPS, or UPI — which transfer method should you use? Compare limits, timing, charges and best use cases. Full guide with 2025 RBI & NPCI figures.

Banking & Transfers • 16 MINS READ

New Tax Regime vs Old Tax Regime: A Real-Numbers Comparison for Salaried Indians (FY 2025-26)

New vs old tax regime FY 2025-26 — compare real tax on ₹6L, ₹10L & ₹15L salaries. See who pays zero tax and find your break-even point.

Tax & Financial Planning • 15 MINS READ

Planning an FD? Don’t Miss These Top Questions About FD Calculators

Curious how FD calculators work? This guide answers the top questions to help you calculate returns, compare plans, and invest smarter in fixed deposits.

FD, PPF & Savings • 5 MINS READ