How to Choose the Best Savings Account in 2026: Comparing Interest Rates & Fees

Find the best savings account for 2026. Compare interest rates, features, and services to make the right choice for your financial goals.

Table of Contents

- The 2026 Snapshot: Who Pays What?

- Deep Dive: The Top Contenders for 2026

- The "Sweep-In" Hack: Getting FD Rates on Savings

- Senior Editor’s Verdict: The "Hub and Spoke" Strategy

- The Math: Why a 4% Difference Matters

- Is it Safe? (The DICGC Safety Net)

- The Hidden Fees of 2026: What to Watch Out For

- Actionable Checklist: Switching Banks in 2026

- Frequently Asked Questions (FAQ)

If you are still keeping your emergency fund in a legacy savings account that earns 2.70%, you are not just "saving" money—you are actively losing it.

In 2026, the Indian banking landscape has fractured into two distinct realities. On one side, we have the "Too Big to Fail" giants like SBI, HDFC, and ICICI. They are flush with liquidity and have zero incentive to offer you higher rates. On the other side, aggressive Small Finance Banks (SFBs) and "Digital-First" challengers are fighting tooth and nail for your deposits, offering rates that rival Fixed Deposits.

With retail inflation hovering around 5.2% this year, a standard savings account offering 3% delivers a negative real return. Effectively, the purchasing power of your idle cash is eroding by roughly 2% every year.

However, moving your money isn't just about chasing the highest number. In 2026, with the rise of AI-driven fraud and the new RBI Master Directions on Digital Security, you also need to factor in app safety, customer support, and hidden "non-maintenance" fees.

Here is your definitive, deep-dive guide to navigating the 2026 savings account market.

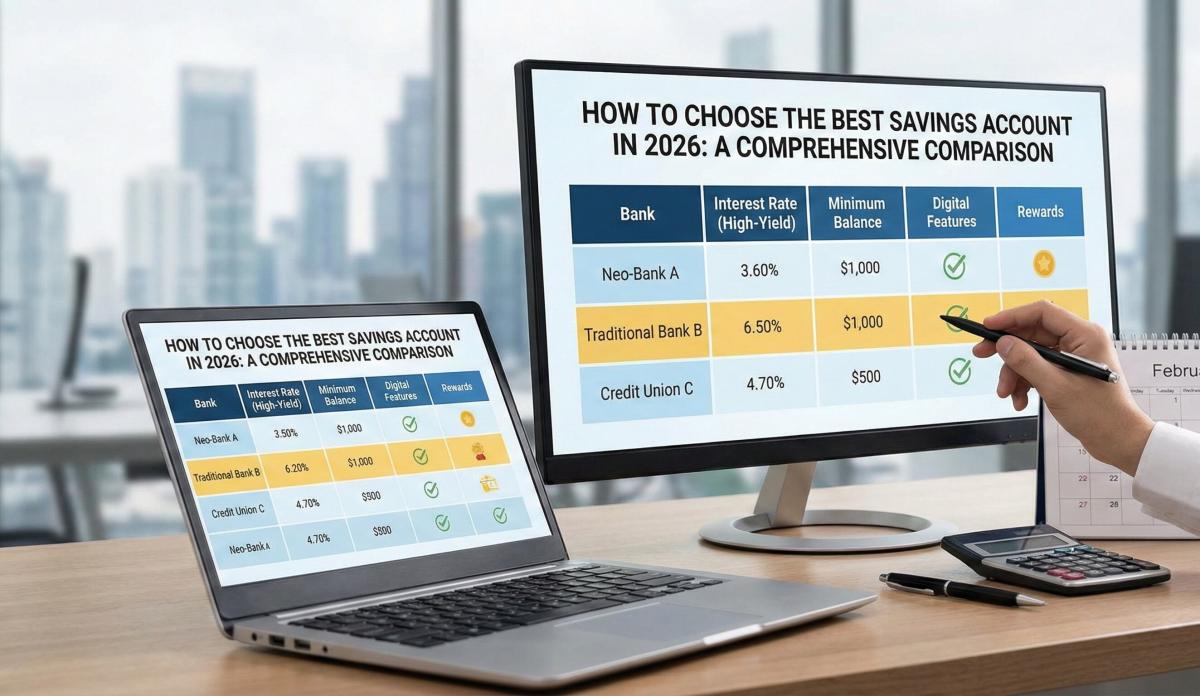

The 2026 Snapshot: Who Pays What?

Let’s stop guessing and look at the raw numbers. I have analyzed the "Effective Annual Yield" for the top contenders as of January 2026. Note that "High Yield" accounts often come with specific tier requirements.

|

Bank Category |

Best For... |

Interest Rate (p.a.) |

Min. Avg Balance (MAB) |

The Catch |

|

Unity / Equitas SFB |

High Yield |

7.00% – 7.50%* |

₹2,500 – ₹10,000 |

Highest rates often apply only to balances above ₹1 Lakh. |

|

IDFC First Bank |

The Balancer |

3.00% – 6.50% |

₹10,000 – ₹25,000 |

Tiered Rate Alert: You only earn 6.5% on amounts above ₹10 Lakhs. Balances <₹1L earn ~3%. |

|

Kotak Mahindra |

Digital Users |

3.50% – 4.00% |

Zero / ₹10,000 |

"ActivMoney" (Sweep-in) is required to hit higher yields (approx 7%). |

|

SBI / PNB |

Safety First |

2.70% Flat |

Zero / ₹500 |

Very low returns. Tech can be sluggish compared to private peers. |

|

HDFC / ICICI |

Primary Hub |

3.00% – 3.50% |

₹10,000 (Urban) |

High non-maintenance charges (₹600+ per quarter). |

> Note: Rates marked with () are subject to balance tiers. For example, a bank might advertise "Up to 7.5%," but that rate may only apply to the slice of money between ₹5 Lakhs and ₹2 Crores. Always check the "Rate Card" before opening.*

Deep Dive: The Top Contenders for 2026

1. The "Yield Hunter" Choice: Unity Small Finance Bank / Equitas SFB

If your primary goal is to beat inflation while keeping money accessible, Small Finance Banks (SFBs) are currently the only game in town.

- The "Why": These banks lend to high-growth sectors (small businesses, micro-loans) where they earn higher interest margins (15-20%). They pass a share of this profit to you to attract deposits.

- The Pros: They are offering 7.00% to 7.50% on savings balances, which is higher than what big banks offer on 1-year FDs.

- The Cons: Their branch network is thin. You will be relying almost entirely on their mobile app. If the app goes down, you cannot just walk down the street to a branch.

- Ideal User: The digital native who wants to park their emergency fund (₹3L–₹5L) and forgets about it.

2. The "Smart Middle" Choice: IDFC First Bank

IDFC First continues to be a favorite in 2026 because of its "Customer First" philosophy, specifically their Monthly Interest Credit feature.

- The Pros: Unlike most banks that credit interest quarterly, IDFC pays you every month. This allows for slightly faster compounding. Their app experience is arguably the best in the industry, with zero clutter.

- The Cons: In 2026, they have restructured their tiers. The "Peak Rate" of 6.50% now kicks in only for balances above ₹10 Lakhs. For smaller amounts (₹1L–₹5L), the rate drops to ~5%, which is still better than SBI but no longer the "highest" in the market.

- Ideal User: Someone who keeps a healthy floating balance (₹5L+) and values a premium app experience over squeezing every last basis point of interest.

3. The "Legacy" Choice: SBI / HDFC Bank

You probably already have one of these. In 2026, their role has changed.

- The Pros: Unmatched trust. If the internet goes down or a cyber-attack hits the banking grid, you can walk into one of 20,000 branches. Their "Senior Citizen" schemes are also more robust.

- The Cons: At 2.70% – 3.00%, your money is stagnating.

- Ideal User: This should be your "Payment Hub." Use this for UPI, salary credits, and bill payments, but sweep excess funds out immediately.

The "Sweep-In" Hack: Getting FD Rates on Savings

If you are risk-averse and don't want to open a new account with a Small Finance Bank, you must utilize the Auto-Sweep facility (branded as "ActivMoney" by Kotak, "Money2World" by others).

How it works:

- You set a threshold, say ₹25,000.

- Any money in your savings account above ₹25,000 is automatically turned into a "Flexi-Fixed Deposit."

- This FD portion earns 6.5% – 7.00% interest.

- The Magic: If you write a cheque or make a UPI payment that exceeds your savings balance, the bank automatically breaks the FD (in multiples of ₹1 or ₹1000) to honor the payment.

The Catch in 2026:

Most banks now charge a "Pre-mature penalty" even on Sweep-in FDs if they are broken within 7 days. Ensure you read the fine print.

Senior Editor’s Verdict: The "Hub and Spoke" Strategy

In 2026, looking for one perfect bank is a mistake. The best financial setup uses a "System" approach.

"My advice? Don't keep all your eggs in the lowest-yielding basket. Adopt the Hub & Spoke model."

- The Hub (Transactional): Keep your SBI or HDFC account for your salary credit, EMIs, and UPI payments. Keep only 1 month's expenses here. This protects your main liquidity from the volatility of smaller banks.

- The Spoke (Parking): Open a Small Finance Bank (SFB) account. Link it to your Hub. Every month, move your surplus savings here. You get the safety of the big bank for payments and the high growth of the SFB for your idle cash.

The Math: Why a 4% Difference Matters

Does moving banks really make a difference? Let’s look at the numbers.

Suppose you park ₹5 Lakhs (your emergency fund) for 1 year.

- Scenario A (SBI @ 2.70%):

- Interest Earned: ₹13,500

- Scenario B (Unity/Equitas @ 7.00%):

- Interest Earned: ₹35,000

The Difference: ₹21,500.

That is essentially a free round-trip flight within India, a year's worth of broadband bills, or a new mid-range smartphone—just for changing where your money sleeps. Over 5 years, due to compounding, this difference widens to over ₹1.2 Lakhs.

Is it Safe? (The DICGC Safety Net)

This is the #1 question I get asked when I recommend Small Finance Banks.

"Is my money safe in these new banks?"

The Answer: Yes, up to ₹5 Lakhs.

All scheduled commercial banks (including SFBs like Unity, Equitas, Ujjivan) are covered by the Deposit Insurance and Credit Guarantee Corporation (DICGC).

- The Rule: If the bank collapses, the RBI guarantees the return of your principal + interest up to ₹5 Lakhs.

- The Strategy: If you have ₹20 Lakhs to park, do not put it all in one SFB. Split it across 4 different banks (e.g., ₹5L in Equitas, ₹5L in Ujjivan, ₹5L in AU Small Finance) to ensure 100% of your corpus is insured.

The Hidden Fees of 2026: What to Watch Out For

Banks in 2026 have become creative with fees to offset their technology costs. Watch out for these:

- SMS Alert Charges: Even "Zero Balance" accounts often charge ₹15/quarter for SMS alerts. You can usually disable this and rely on App Notifications to save money.

- Debit Card Annual Fees: High-yield accounts often come with "Premium" debit cards that cost ₹500–₹1000 per year. If you don't need the lounge access, ask for a basic "Virtual RuPay Card" which is often free.

- IMPS Charges: While NEFT is largely free, many banks still charge ₹5 + GST for IMPS transactions. Use UPI for amounts up to ₹1 Lakh to avoid this.

Actionable Checklist: Switching Banks in 2026

- Check Your Aadhaar Link: ensure your mobile number is updated in Aadhaar. You cannot open a Video KYC account without it.

- Open the "Spoke" Account: Download the app of your chosen high-yield bank (e.g., IDFC/Equitas). Complete the V-KYC during working hours (9 AM - 5 PM) for the fastest approval.

- Test the Transfer: Transfer ₹100 from your main bank to the new one, and then transfer it back. This "whitelists" the beneficiary in the banking backend.

- Update Nominee: Never skip this. In 2026, claiming funds without a registered nominee is a procedural nightmare.

- Set Standing Instructions: Automate your savings. Set a rule to transfer ₹X amount to the high-yield account on the 5th of every month (after salary day).

Frequently Asked Questions (FAQ)

1. Is the interest I earn tax-free?

Only partially. Under Section 80TTA, interest up to ₹10,000 per financial year is tax-free for individuals below 60. Anything above that is added to your income and taxed at your slab rate.

For Senior Citizens: Under Section 80TTB, the exemption limit is significantly higher at ₹50,000.

2. What about Neo-Banks like Jupiter or Fi? Are they safe?

Neo-banks are technically "layers" built on top of traditional banks (e.g., Jupiter partners with Federal Bank). Your money sits with the partner bank, so it enjoys the same DICGC insurance. However, customer support can sometimes be a ping-pong match between the App and the Bank.

3. Why do SFBs offer such high rates? Is something wrong?

No. It is a cost-of-funds calculation. SFBs don't have the massive base of "cheap" salary account deposits that SBI has. To compete, they must offer higher rates to attract funds. They can afford this because they lend at higher rates to niche markets.

4. Can I open these high-yield accounts online?

Yes. In 2026, Video KYC (V-KYC) is the standard. You can open a fully functional Equitas or IDFC account in about 15 minutes sitting on your couch, with just your PAN and Aadhaar.

5. Does a "Zero Balance" account truly mean zero fees?

Rarely. "Zero Balance" usually means no monthly maintenance penalty. However, they will still charge for debit cards, cheque books, and sometimes even for declining a transaction due to insufficient funds. Always download the 'Schedule of Charges' PDF before applying.

Related Blogs

Published on Mar 09, 2026

NEFT vs RTGS vs IMPS vs UPI: Which Transfer Method Should You Use?

NEFT, RTGS, IMPS, or UPI — which transfer method should you use? Compare limits, timing, charges and best use cases. Full guide with 2025 RBI & NPCI figures.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Aug 09, 2025

What to Do if You Transfer Money to the Wrong IFSC Code: A Recovery Guide

Money sent to wrong IFSC? Don't panic! Learn what steps to take immediately to recover your funds and prevent future mistakes.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Jul 27, 2025

Understanding the 11-Digit IFSC Structure: Why the Fifth Character is Always Zero

Decode the IFSC structure! Understand why the 5th character is always zero and what each digit means for fund transfers.

Arjun Sharma

Content Lead – Banking & Payments

Published on Jul 14, 2025

The Role of the Reserve Bank of India (RBI) in Regulating Digital Payment Codes

Learn how the RBI regulates digital payment codes like IFSC, UPI, and SWIFT. Understand compliance and security in Indian banking.

Arjun Sharma

Content Lead – Banking & Payments

Published on Jul 12, 2025

SBI Net Banking Registration 2026: The "No-Nonsense" Guide for New Users

New to banking? This practical guide covers essentials like accounts, cards, digital banking, and safety tips for Indian users.

Priya Nair

Senior Compliance Editor at IFSC.co

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

A Comprehensive Guide to Home Loan Interest Rates: Fixed vs. Floating in 2026

A detailed 2026 guide to home loan interest rates comparing fixed, floating, and hybrid options. Learn the real cost difference, EMI impact, risks, RBI policies, and which option saves you more over 20 years.

EMI & Loans • 8 MINS READ

Mutual Fund Returns Calculator: How It Works, Accuracy & FAQs Explained

A Mutual Fund Returns Calculator helps you estimate the future value of your mutual fund investment using inputs like investment amount, tenure, contributions, and expected returns. It uses compounding to project potential growth and helps you plan smarter investment decisions.

SIP & Investing • 6 MINS READ

NEFT vs RTGS vs IMPS vs UPI: Which Transfer Method Should You Use?

NEFT, RTGS, IMPS, or UPI — which transfer method should you use? Compare limits, timing, charges and best use cases. Full guide with 2025 RBI & NPCI figures.

Banking & Transfers • 16 MINS READ

New Tax Regime vs Old Tax Regime: A Real-Numbers Comparison for Salaried Indians (FY 2025-26)

New vs old tax regime FY 2025-26 — compare real tax on ₹6L, ₹10L & ₹15L salaries. See who pays zero tax and find your break-even point.

Tax & Financial Planning • 15 MINS READ

Planning an FD? Don’t Miss These Top Questions About FD Calculators

Curious how FD calculators work? This guide answers the top questions to help you calculate returns, compare plans, and invest smarter in fixed deposits.

FD, PPF & Savings • 5 MINS READ