The Impact of 2025-2026 Bank Mergers on Your Old IFSC and Branch Details

Understand how bank mergers in 2025-2026 affect IFSC codes and branch details. Update your banking information to avoid transaction failures.

Table of Contents

If you tried to deposit a cheque from an old "Syndicate Bank" or "Oriental Bank of Commerce" chequebook this morning, you likely got a rude shock. Instead of the usual "processing" SMS, you might have received an immediate "Instrument Rejected" notification.

Why? Because as of January 3, 2026, the Indian banking system has fundamentally changed.

For the last few years, we lived in a "grace period." The Reserve Bank of India (RBI) allowed old IFSC codes and MICR bands to work via redirect systems. You could use an old cheque, and the backend would quietly map it to the new "Anchor Bank."

That safety net is now gone.

With the full implementation of the RBI’s "Continuous Clearing" (Phase 2) earlier this month, the tolerance for legacy banking codes has dropped to zero. In 2026, using an old IFSC code isn't just a minor administrative error—it’s a guaranteed transaction failure.

Here is everything you need to know about how the 2025-26 merger finalization affects your money, your loans, and your peace of mind.

Before vs. After: The "Continuous Clearing" Era

To understand why your old details are suddenly invalid, you need to look at the plumbing of the banking system. The RBI has shifted from "Batch Processing" to "Real-Time Settlement."

|

Feature |

Old Rules (Pre-2025) |

New Rules (Jan 2026 Onwards) |

|

Cheque Clearing |

Batch System: Cheques were collected physically and processed in 1-2 days. Humans could override minor code errors. |

Continuous Clearing: Cheques are scanned and validated in 3-hour windows (T+3). Automation rejects invalid MICR codes instantly. |

|

IFSC Routing |

Redirects Active: Sending money to an old ORBC (Oriental Bank) code was auto-forwarded to PUNB (PNB). |

Strict Validation: Old codes are deleted from the NPCI master grid. Transfer attempts return an "Invalid Beneficiary" error immediately. |

|

Auto-Debits (NACH) |

Soft Failures: Banks often manually mapped old mandates to new account structures. |

Hard Bounces: The 2026 NACH Protocol requires the mandate's MICR to match the live core banking system exactly. |

|

Merger Status |

Transition Phase: "System Integration" was ongoing. |

Final Purge: All pre-merger databases have been decommissioned under the Nov 2025 Master Directions. |

Deep Dive: Why Did the Rules Change Now?

You might be asking, "My bank merged years ago. Why is this biting me in 2026?"

It comes down to Technology Standardization.

When banks like Allahabad Bank merged into Indian Bank, they didn't just merge logos; they had to merge two massive, incompatible computer systems (e.g., BaNCS vs. Finacle). For years, banks ran "patch" software to bridge the gap.

However, the RBI Master Directions on Digital Payment Security (November 2025) mandated that all banks must move to a single, unified Core Banking System (CBS) to enable the new High-Speed Clearing Grid.

The "T+3 Hour" Rule

Under the new Phase 2 rules effective January 3rd, when a cheque is presented, the paying bank has only 3 hours to confirm or deny the payment.

- The Problem: The old "redirect" software that mapped your old MICR code to the new one takes too long (milliseconds matter now).

- The Solution: To meet the 3-hour deadline, banks have disabled the redirect lookup. If the MICR on your cheque doesn't match the current database exactly, the system auto-rejects it as "Item Expired" or "Invalid Instrument."

Regulatory Alert: The RBI has stated that "Customer negligence in updating routing details" is a valid ground for banks to charge cheque return fees in 2026. If your EMI bounces because you didn't update the MICR, the penalty falls on you.

Impact on Your Daily Life: The Hidden Failures

The obvious impact is that your old chequebook is useless. But the dangerous impact is invisible.

1. The "SIP" Trap

If you started a Mutual Fund SIP in 2019 using an Andhra Bank account, that mandate is linked to the old MICR. Till 2025, Union Bank (the anchor bank) honored it. But with the 2026 system purge, your SIP might fail this month.

- Result: Your investment streak breaks, and you might be charged a "Bank Rejection Fee" by the Mutual Fund house.

2. Income Tax Refunds

The Income Tax Department has migrated to a "Validated Account Only" refund system. If your profile on the e-filing portal still lists the old IFSC, the system will not issue the refund. It won't even try. It will simply show "Validation Failed."

3. The "Saved Beneficiary" Risk

Open your phone's UPI app or Net Banking. Look at your saved beneficiaries. Do you have a landlord or vendor saved from 4 years ago? If their bank was merged, that "Saved" template uses the old IFSC.

- Attempting a transfer in 2026: The money won't leave your account. You'll get an error code: AC-10 (Invalid Credit Account).

IFSC Relevance: Decoding Your New Identity

If your branch was part of a merger, your account number likely stayed the same (with some exceptions), but your "Digital Address" (IFSC) has 100% changed.

Here is the cheat sheet for the Big 4 Mergers that are fully finalized in 2026:

- Oriental Bank of Commerce (OBC) / United Bank $\rightarrow$ Punjab National Bank (PNB)

- Old Code Starts With: ORBC... / UTBI...

- New Code Starts With: PUNB0...

- Syndicate Bank $\rightarrow$ Canara Bank

- Old Code Starts With: SYNB...

- New Code Starts With: CNRB0...

- Andhra Bank / Corporation Bank $\rightarrow$ Union Bank of India

- Old Code Starts With: ANDB... / CORP...

- New Code Starts With: UBIN0...

- Allahabad Bank $\rightarrow$ Indian Bank

- Old Code Starts With: ALLA...

- New Code Starts With: IDIB0...

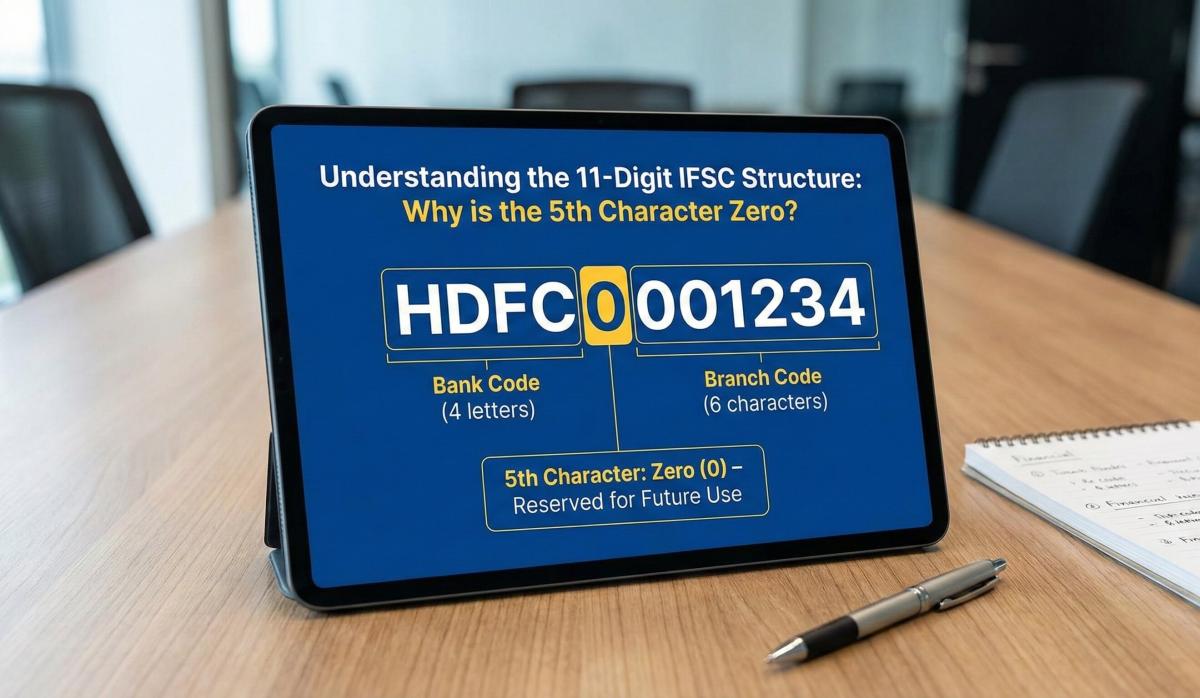

Why is the 5th Character '0'?

In all these new codes (e.g., CNRB0...), the 5th digit is zero. This is crucial. Many users mistype it as the letter 'O' because they are used to the old bank's acronym. The RBI system strictly reads the 5th character as a numeric zero to route the transaction to the correct "partition" of the bank's server.

Actionable Checklist: What You Need to Do Immediately

Don't wait for a transaction to fail. Do this today:

- The "Chequebook Purge": Open your drawer. If you see a chequebook with a logo of a bank that no longer exists (e.g., Dena Bank, Vijaya Bank), shred it. Order a new one via your banking app immediately. The new cheque leaves will have the "2026 Standard" magnetic ink.

- Update Loan Mandates: If you have a Home or Car Loan running from a different bank, check if the auto-debit is pulling from a merged account. If yes, submit a "NACH Mandate Update Form" with the new MICR code to avoid bounce charges.

- Check Your "Linked Accounts" in UPI: Go to GPay/PhonePe/Paytm. If your bank account shows the old bank logo, unlink and re-link it. This forces the UPI app to fetch the fresh IFSC from the NPCI backend.

- Verify IT Portal: Log in to the Income Tax e-filing portal. Go to "My Bank Accounts." If the status is "Validation Pending," re-validate it using the new IFSC.

Frequently Asked Questions (FAQ)

1. Will my old chequebook work if I manually write the new IFSC on it?

No. The sorting machines read the MICR code at the bottom (the magnetic numbers), not your handwriting. If the MICR is old, the machine rejects it in the T+3 scanning window.

2. My account number hasn't changed. Why do I need to update the IFSC?

Think of it this way: Your house (Account Number) is the same, but the street name and pin code (IFSC) have changed. The postman (RBI) needs the new pin code to deliver the money.

3. I sent money to an old IFSC by mistake today. Is it lost?

In 2026, you are safer than before. The system will likely reject it instantly. If it does go through, it will hit a "Dead End" at the receiving bank and bounce back to your account within T+1 hour under the new reversal norms.

4. Are there any more mergers coming in 2026?

The government is currently finalizing the privatization of IDBI Bank (expected completion late 2026). If you are an IDBI customer, keep an eye out for alerts, but for now, your codes remain valid.

5. How do I find my new IFSC code?

Do not Google it blindly.

- Open your Mobile Banking App.

- Go to "Account Info" or "Passbook."

- The code displayed there is the only official one. Alternatively, use trusted verification sites like ifsc.co which update directly from RBI master lists.

Related Blogs

Published on Mar 09, 2026

NEFT vs RTGS vs IMPS vs UPI: Which Transfer Method Should You Use?

NEFT, RTGS, IMPS, or UPI — which transfer method should you use? Compare limits, timing, charges and best use cases. Full guide with 2025 RBI & NPCI figures.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Aug 09, 2025

What to Do if You Transfer Money to the Wrong IFSC Code: A Recovery Guide

Money sent to wrong IFSC? Don't panic! Learn what steps to take immediately to recover your funds and prevent future mistakes.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Jul 27, 2025

Understanding the 11-Digit IFSC Structure: Why the Fifth Character is Always Zero

Decode the IFSC structure! Understand why the 5th character is always zero and what each digit means for fund transfers.

Arjun Sharma

Content Lead – Banking & Payments

Published on Jul 14, 2025

The Role of the Reserve Bank of India (RBI) in Regulating Digital Payment Codes

Learn how the RBI regulates digital payment codes like IFSC, UPI, and SWIFT. Understand compliance and security in Indian banking.

Arjun Sharma

Content Lead – Banking & Payments

Published on Jul 12, 2025

SBI Net Banking Registration 2026: The "No-Nonsense" Guide for New Users

New to banking? This practical guide covers essentials like accounts, cards, digital banking, and safety tips for Indian users.

Priya Nair

Senior Compliance Editor at IFSC.co

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

A Comprehensive Guide to Home Loan Interest Rates: Fixed vs. Floating in 2026

A detailed 2026 guide to home loan interest rates comparing fixed, floating, and hybrid options. Learn the real cost difference, EMI impact, risks, RBI policies, and which option saves you more over 20 years.

EMI & Loans • 8 MINS READ

Mutual Fund Returns Calculator: How It Works, Accuracy & FAQs Explained

A Mutual Fund Returns Calculator helps you estimate the future value of your mutual fund investment using inputs like investment amount, tenure, contributions, and expected returns. It uses compounding to project potential growth and helps you plan smarter investment decisions.

SIP & Investing • 6 MINS READ

NEFT vs RTGS vs IMPS vs UPI: Which Transfer Method Should You Use?

NEFT, RTGS, IMPS, or UPI — which transfer method should you use? Compare limits, timing, charges and best use cases. Full guide with 2025 RBI & NPCI figures.

Banking & Transfers • 16 MINS READ

New Tax Regime vs Old Tax Regime: A Real-Numbers Comparison for Salaried Indians (FY 2025-26)

New vs old tax regime FY 2025-26 — compare real tax on ₹6L, ₹10L & ₹15L salaries. See who pays zero tax and find your break-even point.

Tax & Financial Planning • 15 MINS READ

Planning an FD? Don’t Miss These Top Questions About FD Calculators

Curious how FD calculators work? This guide answers the top questions to help you calculate returns, compare plans, and invest smarter in fixed deposits.

FD, PPF & Savings • 5 MINS READ