Banking System Resilience: Responding to Network Failures

Explore the hidden systems that protect your money during a banking network outage. From AI-driven monitoring to ACID data integrity, learn how banks ensure 2026 resilience.

Table of Contents

- The Invisible Threat: Why Networks Fail

- The First Line of Defense: Automated Systems

- The Role of Distributed Ledger Technology (DLT)

- Human Intervention: Crisis Management & Communication

- Data Integrity and Transaction Reconciliation

- Regulatory Compliance and Future-Proofing

- Key Takeaways

- Frequently Asked Questions

- Conclusion

Imagine the heart-stopping moment: you’re at the ATM, about to withdraw cash, or perhaps attempting to finalize a crucial online payment, and suddenly… nothing. The screen freezes, the transaction times out, and a vague error message appears. This isn’t just an inconvenience; it’s a tangible demonstration of how deeply we rely on the seamless operation of our financial infrastructure. Such scenarios highlight the critical importance of a robust banking system response during network failure, a topic often overlooked until the digital gears grind to a halt. As someone who has spent over a decade dissecting the intricacies of financial technology, I can tell you that beneath the surface of every transaction lies an elaborate ballet of redundant systems, human expertise, and meticulous planning designed precisely for these moments.

The Invisible Threat: Why Networks Fail

Network failures in the banking sector are not always dramatic, catastrophic events; often, they stem from a confluence of seemingly minor issues. Hardware malfunctions, software bugs, human error during routine maintenance, or even localized power outages can trigger widespread disruptions. Cyberattacks, evolving in sophistication daily, represent an increasingly prevalent and malicious cause, aiming to compromise data integrity or simply cripple operations. The complexity of modern banking networks, interconnected globally and reliant on countless third-party services, creates an intricate web where a single point of failure can cascade rapidly, affecting millions of customers and billions in transactions.

The immediate repercussions of a banking network outage are far-reaching and financially significant. ATMs become inoperable, point-of-sale systems fail, online banking portals crash, and interbank transfers halt. This not only creates immense frustration for customers but also poses a severe threat to economic stability, disrupting commerce and trust. Therefore, the urgency for banks to implement resilient architectures and comprehensive disaster recovery plans cannot be overstated. A proactive, multi-layered approach is essential to minimize downtime, restore services swiftly, and ensure the continued flow of capital, even when the digital arteries experience a blockage.

The First Line of Defense: Automated Systems

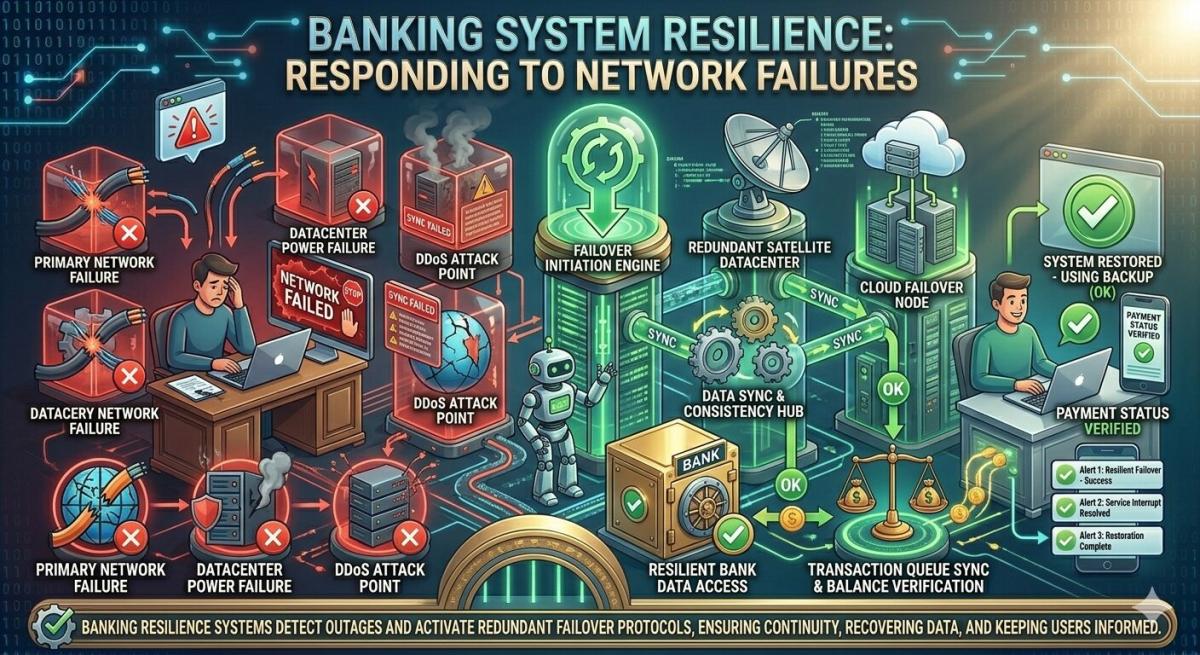

At the forefront of any banking system response during network failure are sophisticated automated systems designed to prevent total collapse. These include redundant network paths, often geographically dispersed, ensuring that if one link goes down, traffic can be rerouted instantly. Automated failover mechanisms detect component failures and seamlessly switch operations to backup servers or data centers, often without any perceptible interruption to the end-user. Load balancing across multiple servers also plays a crucial role, distributing traffic efficiently and preventing single points of congestion or overload that could trigger a wider outage.

Beyond simple redundancy, modern banking infrastructure heavily relies on real-time monitoring and anomaly detection powered by artificial intelligence and machine learning. These systems constantly analyze network traffic, transaction patterns, and system performance metrics, identifying deviations that could signal an impending failure or a security breach. Automated alerts are immediately dispatched to technical teams, enabling them to intervene proactively, sometimes even before customers notice an issue. This predictive capability is becoming increasingly vital, allowing banks to move from reactive problem-solving to proactive mitigation, enhancing overall resilience significantly by 2026.

The Role of Distributed Ledger Technology (DLT)

While not yet fully integrated into core banking systems for transactional processing, Distributed Ledger Technology (DLT), including blockchain, offers an intriguing model for network resilience. Its decentralized nature means that data is replicated across multiple nodes, making it inherently resistant to single points of failure. If one node goes offline, the network can continue operating with the remaining nodes, ensuring data availability and integrity. As banks explore new operational models, DLT’s potential to enhance the banking system response during network failure, particularly for interbank settlements or cross-border payments, is a fascinating area of development for the coming years.

Human Intervention: Crisis Management & Communication

No matter how advanced automated systems become, human expertise remains indispensable during a network crisis. Dedicated incident response teams, often comprising IT specialists, cybersecurity experts, and operational managers, are critical for coordinating the recovery effort. These teams follow meticulously planned escalation protocols, ensuring that the right people are engaged at each stage of a disruption, from initial detection to full restoration. Decision-making under pressure is paramount, often involving complex trade-offs between speed of recovery and data integrity, requiring seasoned professionals to navigate these challenges effectively.

Equally vital during a network failure is transparent and timely communication, both internally and externally. Internally, clear communication channels ensure that all departments are aware of the situation and coordinated in their response, preventing misinformation and duplicated efforts. Externally, banks must communicate clearly and honestly with customers, regulators, and the public about the nature of the outage, its expected duration, and steps being taken to resolve it. This proactive communication builds trust and manages expectations, mitigating panic and reputational damage. Institutions like the Federal Reserve often emphasize the importance of robust communication strategies in their operational resilience guidance.

Data Integrity and Transaction Reconciliation

The paramount concern during and after any network failure is maintaining data integrity. Financial transactions must adhere to the ACID properties – Atomicity, Consistency, Isolation, and Durability – to ensure that money is never lost, duplicated, or incorrectly recorded. Banks employ sophisticated journaling and logging mechanisms that record every transaction step, allowing for precise rollback or forward recovery. This ensures that even if a system crashes mid-transaction, the data can be restored to a consistent state, preventing financial discrepancies that could erode customer confidence and lead to significant financial losses.

Post-recovery, a rigorous process of transaction reconciliation is undertaken to verify the accuracy of all financial records. This involves comparing system logs, identifying any “orphaned” transactions that might have been initiated but not completed, and meticulously ensuring that all accounts reflect the correct balances. Advanced reconciliation software helps automate this complex task, flagging discrepancies for human review. This painstaking attention to detail is a non-negotiable aspect of the banking system response during network failure, safeguarding both the bank’s assets and its customers’ trust, ensuring that every penny is accounted for.

Regulatory Compliance and Future-Proofing

Regulatory bodies worldwide impose stringent requirements on financial institutions regarding operational resilience and disaster recovery planning. Frameworks like Basel III and various local financial authority guidelines mandate that banks demonstrate robust capabilities to withstand and recover from significant disruptions. Non-compliance can result in substantial fines, reputational damage, and even operational restrictions. Banks must regularly test their disaster recovery plans through simulations and drills, proving their ability to restore critical services within predefined recovery time objectives (RTOs) and recovery point objectives (RPOs), often audited by external parties.

Looking ahead to 2026 and beyond, the banking sector is continuously investing in future-proofing its infrastructure against evolving threats. This includes accelerating the adoption of cloud-native architectures for enhanced scalability and resilience, exploring quantum-resistant encryption to protect against future cyber threats, and embracing advanced AI for predictive maintenance and threat detection. The proactive pursuit of innovation and continuous investment in resilient technology are not merely competitive advantages but fundamental necessities for ensuring the enduring stability and trustworthiness of the global financial system. The Bank for International Settlements regularly publishes insights on these future trends.

Key Takeaways

- Layered Resilience is Non-Negotiable: A robust banking system response to network failure relies on multiple layers of defense, from automated failover and redundant infrastructure to sophisticated monitoring and human crisis management. No single solution is sufficient; a holistic approach is critical.

- Data Integrity is Paramount: Ensuring the Atomicity, Consistency, Isolation, and Durability (ACID properties) of transactions is the core objective during and after an outage. Meticulous logging, journaling, and post-recovery reconciliation are essential to prevent financial discrepancies and maintain trust.

- Communication Builds Trust: Transparent, timely, and honest communication with customers, regulators, and internal teams during a network disruption is crucial. It manages expectations, mitigates panic, and protects the institution’s reputation, proving that preparedness extends beyond technology.

- Continuous Investment and Regulatory Adherence: Banks must continually invest in advanced technologies like AI, cloud solutions, and quantum-resistant encryption, while rigorously adhering to evolving regulatory mandates for operational resilience. This proactive stance is vital for safeguarding financial stability in an increasingly complex digital landscape through 2026 and beyond.

Frequently Asked Questions

How do banks ensure my money is safe during a network outage?

Banks employ rigorous data integrity protocols, including redundant data storage, transaction journaling, and automated backup systems. Even if a network fails mid-transaction, these systems ensure that your money is either fully processed or restored to its original state, preventing loss. Post-outage, extensive reconciliation processes verify all account balances.

Can I still use my debit or credit card if a bank’s network is down?

It depends on the nature and scope of the network failure. If the bank’s core processing network is affected, card transactions linked directly to your account with that bank may fail. However, some systems might have offline processing capabilities for smaller transactions, or if the outage is localized, other payment networks might still function. It’s often a good idea to have some cash as a backup.

What should I do if my online banking is unavailable due to an outage?

First, check the bank’s official website or social media channels for updates. Most banks will provide status reports during an outage. Avoid trying to log in repeatedly, as this can sometimes exacerbate issues. If urgent, consider calling their customer service line, though wait times may be longer. Often, the best course of action is patience while the bank works to restore services.

How long does it typically take for banks to recover from a major network failure?

Recovery times vary significantly depending on the cause and severity of the failure. Minor issues might be resolved in minutes or hours due to automated failover. More complex incidents, especially those involving cyberattacks or extensive hardware damage, could take several hours or even a few days to fully restore all services, though critical functions are usually prioritized for faster recovery.

Conclusion

The intricate dance of technology and human expertise underpinning the banking system’s response during network failure is a testament to the industry’s commitment to stability. While no system can be entirely immune to disruption, the continuous evolution of robust infrastructure, proactive monitoring, and meticulous crisis management ensures that financial services remain resilient. As we look towards 2026, the ongoing investment in advanced technologies and adherence to stringent regulatory standards will only strengthen this foundation, safeguarding our financial lives even when the digital superhighway encounters a bump in the road.

Related Blogs

Published on Apr 09, 2026

IFSC Code Explained: How Banks & Branches Connect Internally

Ever wonder how banks communicate? Explore the internal mechanics of how the IFSC code links your branch to the national payment network for NEFT, RTGS, and IMPS.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Transaction Cut-Off Times: Avoid Fund Transfer Delays

Learn how transaction cut-off times affect fund transfers, ACH payments, wire transfers, and real-time payments to avoid delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Bank Transactions Are Delayed on Weekends & Holidays

Learn why bank transactions are delayed on weekends and holidays, including ACH processing, bank cut-off times, fraud checks, and interbank settlement delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Bank Processing Times Differ Between Banks

Learn why bank processing times vary between banks, including ACH, wire transfers, SWIFT, compliance checks, cut-off times, and banking technology in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Are Bank Transfers So Slow? The Real Reasons Revealed

Discover why bank transfers are slow, including legacy banking systems, ACH processing, fraud checks, intermediary banks, and cut-off times in 2026.

Arjun Sharma

Content Lead – Banking & Payments

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ