IFSC Code Explained: How Banks & Branches Connect Internally

Ever wonder how banks communicate? Explore the internal mechanics of how the IFSC code links your branch to the national payment network for NEFT, RTGS, and IMPS.

Table of Contents

It was a chaotic Tuesday morning at the bank. The power had flickered, and for a fleeting moment, all digital systems went dark. I remember the hushed panic, the scramble, and then the collective sigh of relief as everything came back online. In that instant, I truly appreciated the intricate, often invisible, architecture that keeps our financial world running. While we often focus on account numbers, the unsung hero quietly working behind the scenes, ensuring your money reaches the right destination, is the IFSC code. It’s the unique digital fingerprint that tells the system exactly how IFSC Code connects bank and branch internally, making seamless electronic fund transfers possible in a vast, complex banking network.

Understanding the IFSC Code’s Anatomy

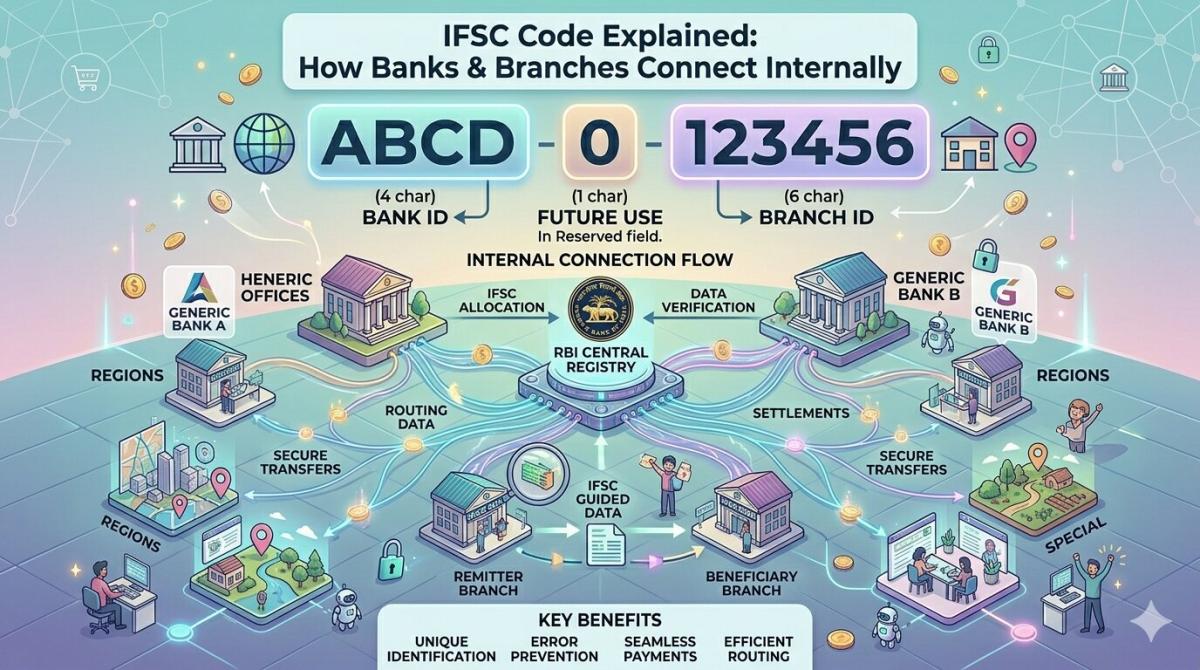

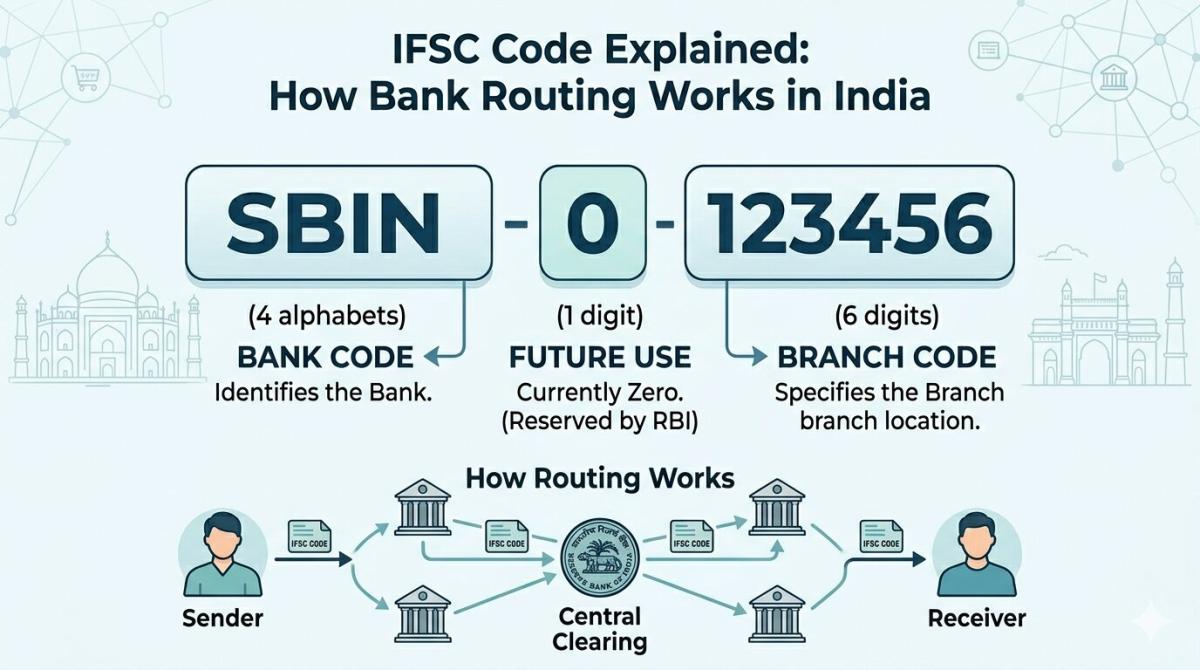

The Indian Financial System Code (IFSC) is a remarkable 11-character alphanumeric code, a vital identifier for every bank branch participating in India’s electronic payment systems. It’s not just a random string; it’s meticulously structured to convey critical information. The first four characters denote the bank name, followed by a zero (a control character reserved for future use), and the final six characters represent the specific branch code. This systematic design ensures that each branch has a unique digital address, essential for distinguishing between hundreds of thousands of branches across the country.

Think of the IFSC as a postal code for digital money. Just as a physical postal code directs a letter to the correct post office and street, the IFSC directs digital funds to the precise bank and branch. Without this granular level of identification, the sheer volume of interbank transactions would be prone to errors and delays. It’s the primary tool that allows various electronic payment systems like NEFT, RTGS, and IMPS to operate with unparalleled efficiency and accuracy, ensuring your funds are routed correctly every single time.

The Backbone of Electronic Fund Transfers

When you initiate an NEFT or RTGS transaction, the IFSC code is not merely an optional field; it’s the lynchpin of the entire process. The sending bank’s system uses this code to identify the recipient’s bank and, crucially, the specific branch where the beneficiary holds an account. This identification allows the payment system to accurately route the funds, ensuring they don’t get lost in the vast network of India’s more than 150,000 bank branches. It’s a testament to its design that billions of rupees move daily with minimal issues.

The journey of your digital rupee, facilitated by the IFSC code, is a marvel of modern banking. Once you input the beneficiary’s IFSC, account number, and amount, your bank’s system validates the code. It then communicates with the central payment clearing house (like those managed by the Reserve Bank of India or NPCI), which uses the IFSC to pinpoint the destination bank and branch. The funds are then transferred and settled, often within minutes, making real-time transactions a reality. This intricate dance underscores how IFSC Code connects bank and branch internally, making digital payments ubiquitous.

Routing and Error Prevention

Beyond simple identification, the IFSC code plays a critical role in the sophisticated routing mechanisms of India’s payment infrastructure. It acts as a routing key, guiding transactions through the correct channels from the originating bank to the destination branch. This precise routing minimizes the chances of funds being misdirected or delayed, which could otherwise lead to significant financial and operational headaches. Its structured format allows automated systems to process transactions at high speeds with remarkable accuracy, a cornerstone of financial stability.

In a system processing millions of transactions daily, even a small error rate can have monumental consequences. The IFSC code is a primary defense against such errors. By uniquely identifying each branch, it prevents ambiguity that could arise from similar-sounding branch names or locations. This precision reduces the need for manual intervention, cuts down on transaction failures, and enhances the overall trust in digital payment systems. It’s this commitment to accuracy that gives users confidence in the system, knowing their money will reach its intended target.

IFSC’s Role in Modern Banking Infrastructure

The IFSC code is deeply embedded within the core banking systems (CBS) of virtually every financial institution in India. It’s not an add-on but an integral part of how these systems communicate and process interbank transactions. From initial account opening to daily transaction processing, the IFSC is a constant, ensuring that all internal records align with the external payment networks. This integration is vital for maintaining data consistency and operational integrity across disparate banking platforms, making it a foundational element of the country’s financial tech stack.

The User Experience and Common Pitfalls

For the end-user, the IFSC code is a familiar, if sometimes forgotten, piece of information required for most online fund transfers. While typically found on cheque books, passbooks, or bank websites, its accurate input is paramount. A single incorrect character can lead to transaction failure or, worse, funds being sent to an unintended recipient, requiring complex reversal procedures. This highlights the user’s responsibility in ensuring the correctness of this vital code, reinforcing its importance in everyday financial interactions.

A common misconception is that the IFSC code is interchangeable between different branches of the same bank, or even that it’s a personal identifier. Neither is true. Each branch, regardless of its parent bank, has its own unique IFSC. Furthermore, the IFSC is not tied to an individual account holder; it identifies the branch where the account is held. Always double-check the code for the specific branch you intend to send money to. The Reserve Bank of India provides a lookup tool, and major banks often publish their branch IFSC codes on their official websites, like ICICI Bank’s official branch locator, for easy verification.

Evolution and Future of Financial Identifiers

The IFSC code was introduced to streamline electronic fund transfers, replacing older, less efficient methods of interbank communication. Its advent marked a significant leap forward in India’s financial infrastructure, paving the way for the digital payment revolution we see today. Before IFSC, manual reconciliation and slower processing times were common, making large-scale electronic payments cumbersome. The code’s robust design has allowed it to remain relevant and effective for years, adapting to increasing transaction volumes.

Looking ahead to 2026 and beyond, while new financial identifiers and payment methods might emerge, the fundamental need for a unique branch identifier like the IFSC will likely persist. Its established integration into core banking systems and its role in regulatory compliance make it incredibly difficult to supersede entirely. Any future advancements, such as potentially more advanced API-driven payment rails or cross-border payment innovations, will likely build upon or integrate with the existing IFSC framework, rather than completely replacing it, given its deep roots in the Indian financial system. You can learn more about its regulatory framework by visiting the Reserve Bank of India website.

Key Takeaways

- Unique Branch Identification: The IFSC code is an 11-character alphanumeric code uniquely identifying each bank branch in India, crucial for distinguishing between hundreds of thousands of locations.

- Foundation of Electronic Transfers: It is the indispensable component for NEFT, RTGS, and IMPS transactions, enabling accurate routing of funds from the sender’s bank to the beneficiary’s specific branch.

- Error Prevention and Security: Its precise structure minimizes transaction errors, reduces misdirection of funds, and enhances the overall security and efficiency of the digital payment ecosystem, thereby building user trust.

- Integrated into Core Banking: The IFSC is deeply embedded within banks’ core banking systems, serving as a fundamental piece of infrastructure for internal record-keeping and external payment network communication.

Frequently Asked Questions

What does IFSC stand for and what is its primary purpose?

IFSC stands for Indian Financial System Code. Its primary purpose is to uniquely identify every bank branch participating in India’s electronic funds transfer systems, such as NEFT, RTGS, and IMPS, ensuring that money is routed to the correct destination branch.

Can two different bank branches have the same IFSC code?

No, absolutely not. Each bank branch in India has its own unique IFSC code. Even if two branches belong to the same bank and are in the same city, their IFSC codes will always be distinct, typically differing in the last six characters.

What happens if I enter an incorrect IFSC code during a transaction?

If you enter an incorrect IFSC code, the transaction will typically fail immediately, as the system won’t be able to identify a valid destination branch. In rare cases, if the incorrect code happens to correspond to a different valid branch, funds might be misdirected, requiring a complex reversal process.

Where can I find the correct IFSC code for a bank branch?

You can usually find the correct IFSC code printed on your cheque book, bank passbook, or on the bank’s official website. Authoritative sources like the Reserve Bank of India’s website or the National Payments Corporation of India (NPCI) also provide lookup tools for verification, ensuring accuracy for your 2026 transactions.

Conclusion

The IFSC code, often an overlooked detail, is a monumental piece of India’s financial architecture. It’s the silent workhorse that ensures billions of digital transactions flow smoothly and accurately, connecting banks and branches internally with unparalleled precision. My years of observing financial systems have shown me that such foundational identifiers are the bedrock of trust and efficiency in modern banking. Understanding its role isn’t just academic; it empowers you as a user and provides a deeper appreciation for the seamless financial world we inhabit, a testament to thoughtful design.

Related Blogs

Published on Apr 09, 2026

IFSC Code Explained: How Bank Routing Works in India

Understand the step-by-step routing process of bank transfers in India. Learn how IFSC codes guide NEFT, RTGS, and IMPS transactions in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Transaction Cut-Off Times: Avoid Fund Transfer Delays

Learn how transaction cut-off times affect fund transfers, ACH payments, wire transfers, and real-time payments to avoid delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Bank Transactions Are Delayed on Weekends & Holidays

Learn why bank transactions are delayed on weekends and holidays, including ACH processing, bank cut-off times, fraud checks, and interbank settlement delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Bank Processing Times Differ Between Banks

Learn why bank processing times vary between banks, including ACH, wire transfers, SWIFT, compliance checks, cut-off times, and banking technology in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Are Bank Transfers So Slow? The Real Reasons Revealed

Discover why bank transfers are slow, including legacy banking systems, ACH processing, fraud checks, intermediary banks, and cut-off times in 2026.

Arjun Sharma

Content Lead – Banking & Payments

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ