Why Bank Transactions Are Delayed on Weekends & Holidays

Learn why bank transactions are delayed on weekends and holidays, including ACH processing, bank cut-off times, fraud checks, and interbank settlement delays in 2026.

Table of Contents

Have you ever desperately needed a payment to clear, only to find it stuck in limbo over a long weekend? I certainly have. Years ago, I wired funds for a critical medical expense on a Friday afternoon, only to realize with a sinking feeling that it wouldn’t arrive until Tuesday. That experience really drove home a common frustration for many: Why transactions are delayed on weekends and holidays. It’s a question that plagues individuals and businesses alike, leading to missed deadlines, cash flow headaches, and sometimes, genuine anxiety. Understanding the intricate machinery behind financial transactions reveals that these delays aren’t arbitrary; they’re a systemic reality rooted in how our global financial infrastructure operates.

The Human Element: Bank Staffing and Operations

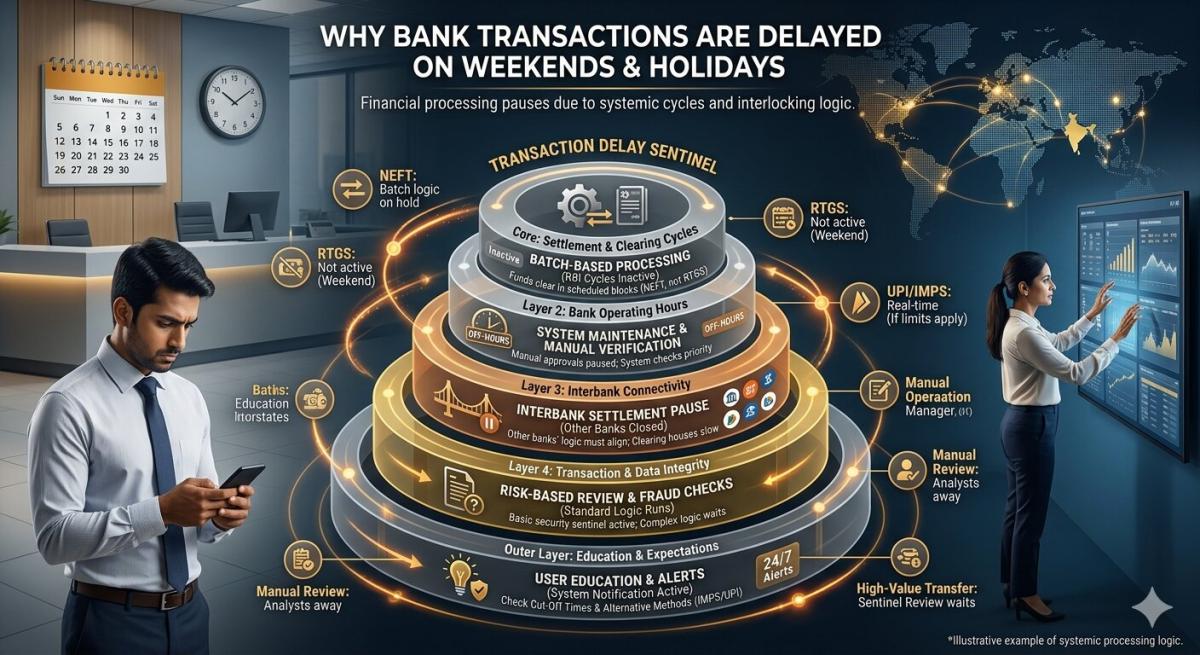

At the heart of many transaction delays lies the simple fact that banks, like most businesses, observe standard working hours, weekends, and public holidays. While digital platforms allow us to initiate transfers 24/7, the actual processing often relies on human oversight and manual intervention, particularly for complex or high-value transactions. Bank employees, from tellers to compliance officers, are not typically working around the clock on Christmas Day or the Fourth of July. This means that any transaction requiring a manual review, fraud check, or specific authorization will simply wait until the next business day.

Moreover, the back-office operations, which are crucial for reconciling accounts and settling funds, also adhere to these schedules. Think of it as a factory line; even if you submit an order digitally, the physical production and shipping only happen during operating hours. This is especially true for traditional banking services and older payment rails. Even in 2026, despite advancements, the foundational structure of many financial institutions still relies on a Monday-to-Friday workflow for critical, non-automated tasks, impacting the speed at which funds move across different entities.

Interbank Networks and Clearing Houses

The vast majority of money transfers aren’t just moving within a single bank; they’re traversing interbank networks. When you send money from Bank A to Bank B, those two institutions need to communicate, verify, and ultimately settle the transaction. This process is typically facilitated by clearing houses and central banks, such as the Federal Reserve in the U.S. or the Bank of England. These central bodies operate on specific schedules, often closing their systems down during non-business hours, weekends, and public holidays.

These networks act as crucial intermediaries, ensuring the integrity and security of the financial system. For instance, the Automated Clearing House (ACH) network, widely used for direct deposits and bill payments in the U.S., processes transactions in batches, not in real-time. While same-day ACH has become more prevalent, even it has specific cutoff times. If you initiate an ACH payment after these cutoffs on a Friday, it won’t even begin processing until the following Monday, pushing its final settlement to Tuesday or even Wednesday, depending on bank holidays. The operational hours of these critical infrastructures directly dictate when funds can be officially moved and verified.

Understanding ACH Processing Windows

The ACH network, managed by Nacha, is a prime example of a system with defined processing windows. Unlike instant payment systems, ACH transactions are collected throughout the day and then sent for processing in scheduled batches. Typically, there are multiple processing windows daily, but these cease operation entirely on weekends and federal holidays. If a transaction misses the final processing window on a Friday, it effectively sits in a queue until the next available processing window, which will be Monday morning. This batch-oriented approach is a fundamental reason why many common electronic payments experience delays over non-business days, even in our increasingly digital financial landscape.

Regulatory Frameworks and Compliance Deadlines

Financial transactions are heavily regulated to prevent fraud, money laundering, and terrorist financing. Regulatory bodies impose strict compliance requirements on financial institutions, dictating how transactions must be monitored, verified, and reported. Many of these compliance checks, particularly for larger sums or international transfers, require human review or adhere to specific daily reporting deadlines set by government agencies. These deadlines, naturally, only apply to business days.

Furthermore, international transactions often involve multiple jurisdictions, each with its own banking holidays and regulatory calendar. A transfer initiated on a Friday from the US to, say, Germany, might encounter delays not only due to US weekend closures but also German public holidays. These layered complexities mean that even if one part of the chain is operational, another might be closed, effectively halting the transaction’s progress. Adherence to these strict rules, while vital for security, inherently builds in processing pauses aligned with traditional business days globally. You can learn more about global payment systems from resources like the Bank for International Settlements.

The Role of Payment Types

Not all payment methods are created equal when it comes to speed. The type of transaction you initiate significantly impacts its susceptibility to weekend and holiday delays. Real-time payment systems, like Zelle or certain instant payment rails in other countries, are designed to process transactions almost instantaneously, regardless of the day or time. However, these systems often have lower transaction limits and are not universally adopted for all types of payments, especially large corporate transfers or international wires.

Conversely, traditional methods like paper checks or standard wire transfers are notoriously slow. Checks need to be physically deposited and then undergo a clearing process that can take several business days. Wire transfers, while faster than checks, still rely on bank operating hours for initiation and settlement, making them highly vulnerable to weekend and holiday delays. Even in 2026, while instant payment adoption grows, many legacy systems remain integral, perpetuating these traditional processing cycles.

Fraud Prevention and Security Checks

In our increasingly digital world, the threat of financial fraud is ever-present. Banks invest heavily in sophisticated fraud detection systems that flag suspicious transactions for review. While automated systems handle a significant portion of this, certain alerts or high-risk transactions still require manual investigation by fraud analysts. These analysts, again, operate during standard business hours, meaning a transaction flagged for review on a Friday evening might not be cleared until Monday morning or even later if the volume is high.

These security measures are a critical safeguard for both the bank and its customers. Imagine if a fraudulent transaction went through unchecked simply because it was a Saturday. While inconvenient, these delays serve to protect your funds and the integrity of the financial system. Balancing speed with security is a constant challenge for financial institutions, and on weekends and holidays, the pendulum often swings towards caution, leading to necessary pauses in processing while critical personnel are off-duty. The need for robust security is paramount, making these deliberate delays a necessary evil in many cases.

Key Takeaways

- Operational Hours of Financial Institutions: Banks and central clearing houses operate on standard business days, Monday to Friday, and close on weekends and public holidays. This directly impacts the processing of any transaction that requires manual review, reconciliation, or settlement through these systems.

- Batch Processing for Many Payment Types: Systems like the Automated Clearing House (ACH) process transactions in batches with specific cutoff times. If a transaction misses a cutoff, especially on a Friday, it will not be processed until the next available batch on the following business day, leading to multi-day delays.

- Regulatory and Compliance Requirements: Strict financial regulations and reporting deadlines, designed to prevent fraud and money laundering, often require human oversight and adherence to business day schedules. International transfers further complicate matters with varying global holiday calendars.

- The Balance Between Speed and Security: While instant payment systems exist, many transaction types still pass through rigorous fraud prevention and security checks. These manual reviews, crucial for protecting funds, are typically conducted during standard banking hours, causing necessary delays on non-business days.

Frequently Asked Questions

Why can I send money instantly with apps like Zelle but not via a bank transfer?

Apps like Zelle operate on real-time payment rails that are distinct from traditional bank transfers (like ACH or wire transfers). These real-time networks are designed for immediate settlement, often for smaller, person-to-person transactions. Traditional bank transfers, especially those involving different banks, typically use older, batch-processed systems that adhere to conventional banking hours for clearing and settlement.

Are international transactions more susceptible to weekend and holiday delays?

Yes, absolutely. International transactions face compounded delays because they must navigate the operational calendars and regulatory frameworks of multiple countries. A public holiday in either the originating or receiving country, or any country through which the funds are routed, can cause significant additional delays beyond what a domestic transfer might experience.

What can I do to avoid transaction delays on weekends?

To minimize delays, always plan ahead. Initiate critical transactions well before Friday afternoon, ideally early in the week. Understand the specific cutoff times for your chosen payment method (e.g., ACH, wire transfer). For urgent needs, explore instant payment options if available and suitable for your transaction type and amount, but always verify their limits and fees.

Will all transactions eventually become instant, even on holidays, by 2026?

While the trend towards instant payments is strong and growing rapidly, it’s unlikely that all transactions will be instant by 2026. Complex transactions, large corporate payments, and international transfers often involve more layers of security, regulation, and interbank coordination that are harder to automate for real-time processing. However, we can expect a significant increase in instant payment availability for everyday consumer and small business needs.

Conclusion

The reasons why transactions are delayed on weekends and holidays are multifaceted, stemming from a complex interplay of human operations, interbank network schedules, regulatory requirements, specific payment type characteristics, and vital fraud prevention measures. While the digital age has certainly accelerated many aspects of banking, the foundational infrastructure for moving money often still adheres to a conventional business week. Understanding these inherent limitations allows us to better plan our financial activities, manage expectations, and appreciate the intricate systems working behind the scenes to keep our money safe and sound, even if it sometimes takes a little longer to arrive.

Related Blogs

Published on Apr 09, 2026

IFSC Code Explained: How Banks & Branches Connect Internally

Ever wonder how banks communicate? Explore the internal mechanics of how the IFSC code links your branch to the national payment network for NEFT, RTGS, and IMPS.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Transaction Cut-Off Times: Avoid Fund Transfer Delays

Learn how transaction cut-off times affect fund transfers, ACH payments, wire transfers, and real-time payments to avoid delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Bank Processing Times Differ Between Banks

Learn why bank processing times vary between banks, including ACH, wire transfers, SWIFT, compliance checks, cut-off times, and banking technology in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Are Bank Transfers So Slow? The Real Reasons Revealed

Discover why bank transfers are slow, including legacy banking systems, ACH processing, fraud checks, intermediary banks, and cut-off times in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

How Banking Networks Scale to Handle High Transaction Loads

Learn how banking networks handle high transaction volumes using ACH, RTGS, SWIFT, cloud infrastructure, AI fraud detection, and real-time payments in 2026.

Arjun Sharma

Content Lead – Banking & Payments

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ