Why Bank Processing Times Differ Between Banks

Learn why bank processing times vary between banks, including ACH, wire transfers, SWIFT, compliance checks, cut-off times, and banking technology in 2026.

Arjun Sharma

Content Lead – Banking & Payments

10 min read

Table of Contents

Have you ever stared at your online banking app, refreshing it repeatedly, wondering why a payment you sent or received hasn’t cleared yet? Or perhaps you’ve been on the receiving end of a frustrated client asking why their invoice hasn’t been paid, only to find out it’s stuck in banking limbo. I certainly have. It was a crucial international wire transfer for a project milestone, and the bank processing time variation between different banks nearly cost me a client. This isn’t just an inconvenience; it’s a fundamental aspect of financial operations that often puzzles individuals and businesses alike. Understanding the intricate factors at play is key to navigating the modern financial landscape, and it’s far more complex than a simple “fast” or “slow” label.

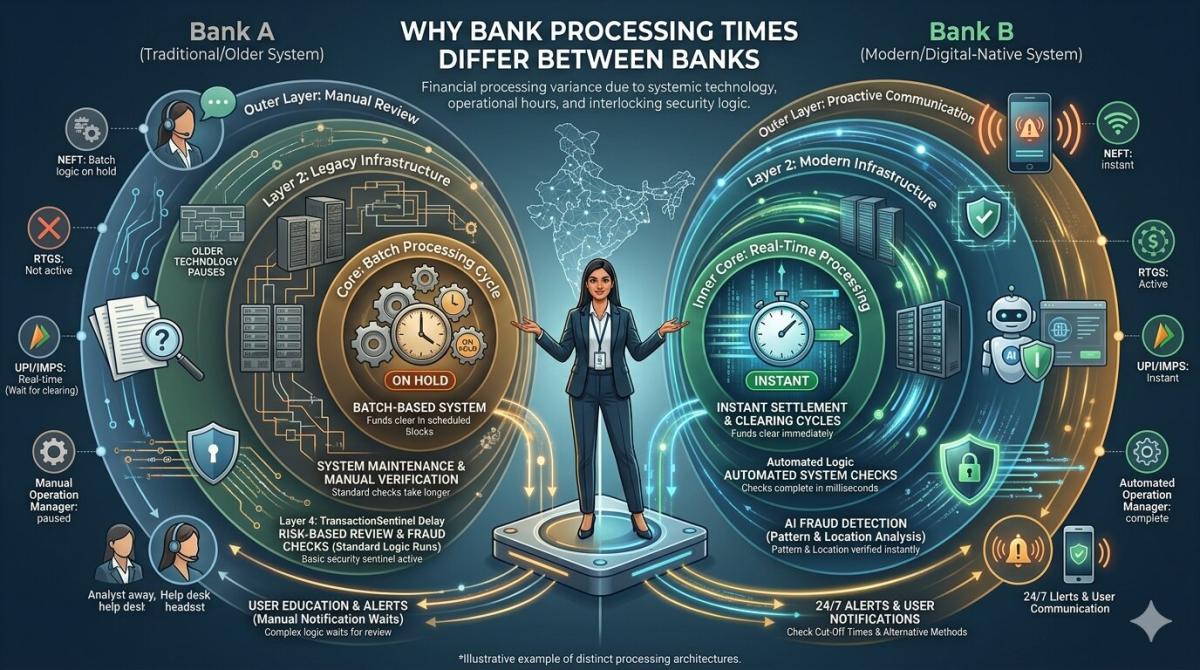

The Core Infrastructure Divide

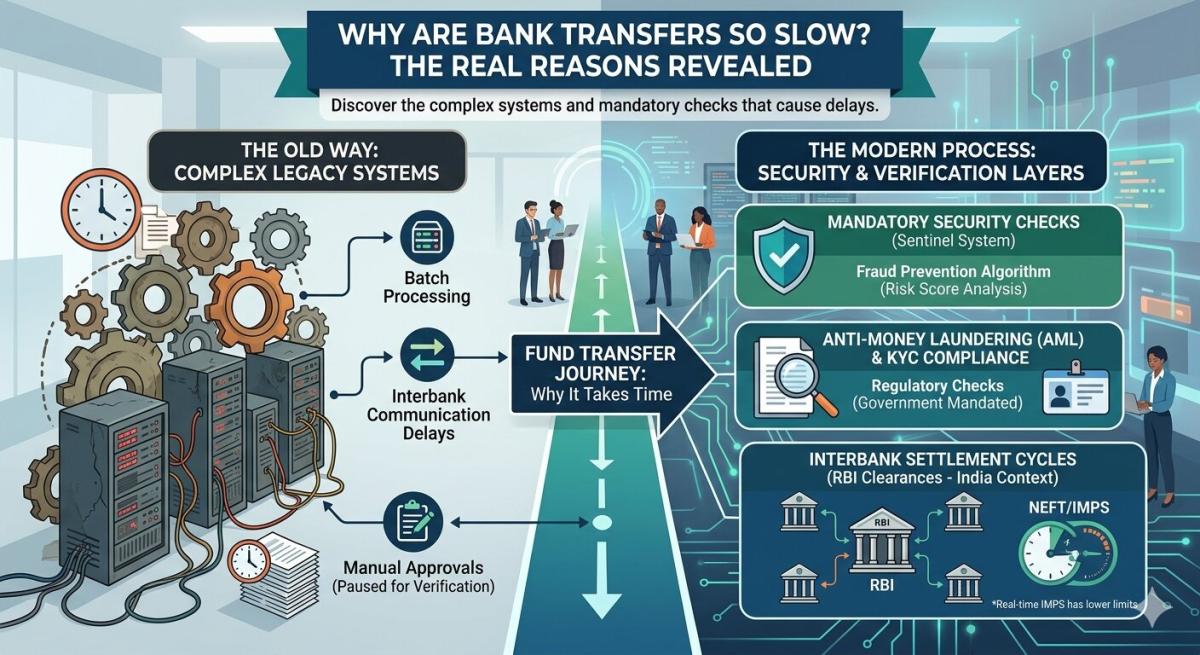

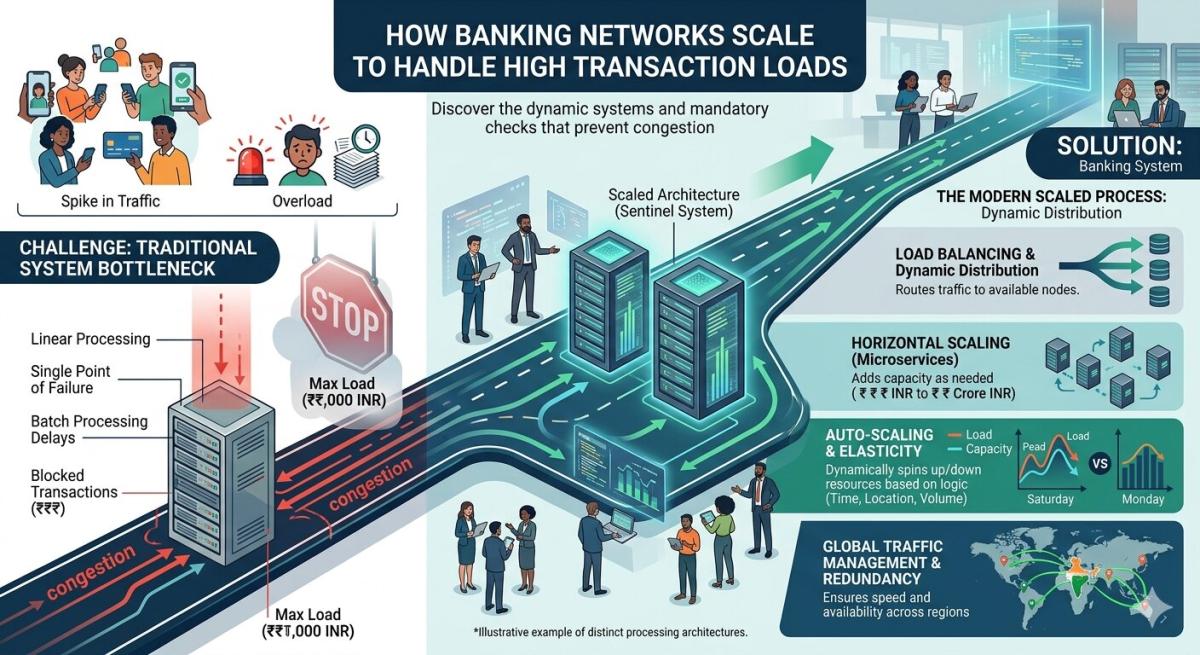

One of the most significant contributors to the disparity in bank processing times lies deep within the technological infrastructure of financial institutions. Many established, older banks still rely on legacy systems that were designed decades ago. These systems often operate on a batch processing model, where transactions are collected throughout the day and then processed together at specific intervals, rather than individually in real-time. This foundational architecture inherently builds in delays, as the system waits for these scheduled processing windows, much like an old train waiting for its next departure time.

Conversely, many newer banks and fintech-driven institutions have built their systems from the ground up using modern cloud-based technologies and APIs (Application Programming Interfaces). These advanced platforms enable near real-time processing, allowing transactions to be validated and cleared almost instantaneously. This isn’t merely an upgrade; it’s a paradigm shift from a batch-oriented approach to a continuous flow, significantly reducing the internal latency for tasks like transferring funds or updating account balances. This technological chasm is a primary driver of the processing speed differences we observe today.

Regulatory Frameworks and Compliance

Beyond technology, the regulatory environment plays a colossal role in dictating how quickly banks can process transactions. Each country, and often specific regions within them, has its own set of rules governing financial transactions, particularly concerning anti-money laundering (AML) and know-your-customer (KYC) protocols. International transfers, for instance, are subject to a labyrinth of cross-border regulations, requiring multiple layers of verification and screening against sanctions lists. These stringent checks, while absolutely vital for global financial security, inevitably add to processing times as banks diligently comply.

Domestically, even within a single country, different types of transactions might fall under various regulatory umbrellas. For example, a simple interbank transfer might be subject to different settlement rules than a large commercial payment. Furthermore, banking holidays, which vary significantly by region and nation, can bring processing to a standstill. A transfer initiated on a Friday afternoon before a long weekend in Europe might not even begin its journey until the following Tuesday, a frustrating reality for anyone expecting immediate funds.

Transaction Type and Value

The nature of the transaction itself is a major determinant of processing speed. Not all money movements are created equal, and banks employ different “rails” or networks depending on what’s being sent. For example, an Automated Clearing House (ACH) transfer in the United States, commonly used for payroll or bill payments, is known for its lower cost but typically takes 1-3 business days to settle. This is in stark contrast to a same-day wire transfer, which, while more expensive, offers near-instantaneous movement of funds because it utilizes a different, faster network designed for high-value, urgent transactions.

Moreover, the monetary value of a transaction can trigger additional scrutiny. Larger sums often undergo enhanced fraud detection and compliance checks, regardless of the bank or network used. This is a risk mitigation strategy; a bank’s algorithms might flag an unusually large transfer, prompting a manual review by a human agent. This extra layer of due diligence, while safeguarding against illicit activities, inherently introduces delays that wouldn’t apply to smaller, routine transactions. It’s a necessary friction point in the pursuit of financial security.

The SWIFT vs. ACH Divide

When discussing transaction types, the distinction between SWIFT and ACH is particularly illuminating for understanding bank processing time variation between different banks. SWIFT (Society for Worldwide Interbank Financial Telecommunication) is a global messaging network used primarily for international wire transfers. It’s not a payment system itself but a secure messaging service that facilitates communication between banks to initiate and settle payments. Due to its global reach and the multi-bank intermediary chain involved, SWIFT transfers can often take 1-5 business days, sometimes longer, depending on time zones and correspondent banks. ACH, on the other hand, is a domestic U.S. network, designed for bulk processing of lower-value payments like direct deposits or bill payments, and while it’s cheaper, its standard settlement times are slower than wires, typically 1-3 business days. Understanding which network your bank uses for different transaction types is crucial for setting expectations.

Bank Size and Operational Efficiency

It’s tempting to assume that larger banks, with their vast resources, would always be faster. However, this isn’t always the case. The sheer size and complex organizational structures of some multinational banking giants can paradoxically lead to slower processing times. Multiple departments, layers of bureaucracy, and disparate internal systems (often the result of mergers and acquisitions over decades) can create bottlenecks. Information might need to pass through several internal gateways before a transaction is fully cleared, adding precious hours or even days to the process. This internal friction can be a significant drag on efficiency.

Conversely, smaller, more agile community banks or digital-first challenger banks often boast streamlined operations. With fewer legacy systems to contend with and a more integrated internal workflow, they can sometimes process transactions with surprising speed. Their focus on specific customer segments or digital innovation allows them to optimize processes for efficiency, bypassing the bureaucratic hurdles that plague their larger counterparts. It’s not always about raw computing power, but about the fluidity of internal operations and the absence of institutional inertia. I’ve personally seen smaller institutions integrate new payment technologies by 2026 far quicker than some of the established giants.

The Human Element and Cut-off Times

Despite the increasing automation in banking, the human element still plays a critical, albeit sometimes delaying, role. Many transactions, especially those flagged for unusual activity or large sums, require manual review by a bank employee. Fraud detection algorithms are sophisticated, but human judgment is often the final arbiter, and this human intervention naturally introduces a delay. These teams operate during business hours, meaning a transaction flagged late on a Friday afternoon might not be reviewed until the next business day, compounding the waiting period.

Furthermore, every bank operates with daily “cut-off times” for different types of transactions. Payments initiated after these specified times are typically processed on the next business day. These cut-off times vary significantly between banks and even for different services within the same bank. Weekends and public holidays further complicate matters, as banks and payment networks are often closed, pushing processing to the next available business day. Understanding these critical deadlines is essential for anyone needing to send or receive time-sensitive payments, and they are a major source of the bank processing time variation between different banks.

Key Takeaways

- Technological Infrastructure is Paramount: Older banks often rely on batch-processing legacy systems, leading to inherent delays, while modern fintechs leverage real-time processing for significantly faster transactions. Your bank’s core tech stack directly impacts its speed.

- Regulatory Compliance Adds Layers of Scrutiny: International and high-value transactions are subject to extensive AML/KYC checks and varying global regulations, which, while crucial for security, inevitably extend processing times. Domestic rules and banking holidays also play a significant role.

- Transaction Type Dictates the “Rails”: Different payment networks (e.g., ACH for bulk domestic, SWIFT for international wires, real-time payments like FedNow) have distinct settlement speeds and costs. Selecting the right method for your urgency and value is critical.

- Operational Efficiency and Human Review Matter: Bank size and internal bureaucracy can create bottlenecks, while smaller banks often benefit from streamlined processes. Manual fraud reviews and strict daily cut-off times also introduce unavoidable delays, especially outside standard business hours.

Frequently Asked Questions

Why do international transfers take longer than domestic ones?

International transfers involve multiple banks (sender, correspondent, recipient), different regulatory environments, varying banking holidays, and time zones. They often use the SWIFT network, which is a messaging system, meaning the actual transfer of funds can take several days as banks communicate and settle. Domestic transfers typically use more integrated, faster national networks with fewer intermediary steps.

Can I speed up a bank transfer?

Generally, yes, by choosing a faster payment method. For urgent domestic payments, a wire transfer is usually faster than an ACH transfer, though it comes at a higher cost. For international transfers, some banks offer expedited services, but the underlying network limitations often still apply. Real-time payment systems like FedNow are also becoming more prevalent in the U.S. by 2026, offering near-instant domestic transfers.

Do all banks have the same cut-off times?

No, cut-off times vary significantly from bank to bank and even between different services within the same bank. For instance, the cut-off for an outgoing wire transfer might be earlier than for an internal transfer. It’s always best to check with your specific bank for their detailed schedules, especially for time-sensitive transactions, as missing a cut-off means processing won’t begin until the next business day.

Why does my bank hold funds even after a deposit shows in my account?

Even if a deposit appears in your account balance, the funds might not be immediately available for withdrawal or spending. This is a common practice for risk management, especially for checks or larger deposits. Banks need time to verify the funds are legitimate and will clear from the originating institution. The specific hold period is regulated and can vary based on your account history, the type of deposit, and the amount, ensuring the bank is protected against bounced checks or fraud.

Conclusion

Navigating the nuances of bank processing time variation between different banks is truly an art form in today’s interconnected world. It’s a complex interplay of outdated systems versus modern tech, stringent regulations, diverse transaction types, and the human element. For individuals and businesses alike, understanding these underlying mechanisms isn’t just academic; it’s pragmatic. By anticipating potential delays and choosing the right banking partner and transaction method for your needs, you can mitigate financial friction and ensure your money moves efficiently, rather than leaving you in frustrating limbo.

Related Blogs

Published on Apr 09, 2026

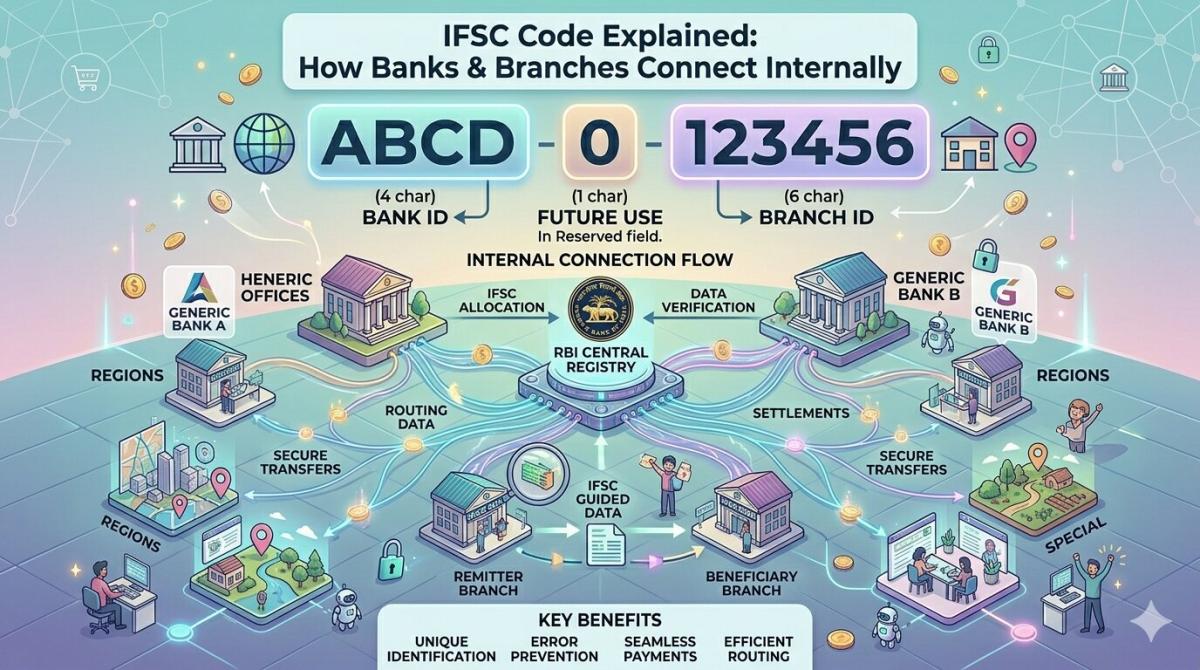

IFSC Code Explained: How Banks & Branches Connect Internally

Ever wonder how banks communicate? Explore the internal mechanics of how the IFSC code links your branch to the national payment network for NEFT, RTGS, and IMPS.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Transaction Cut-Off Times: Avoid Fund Transfer Delays

Learn how transaction cut-off times affect fund transfers, ACH payments, wire transfers, and real-time payments to avoid delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

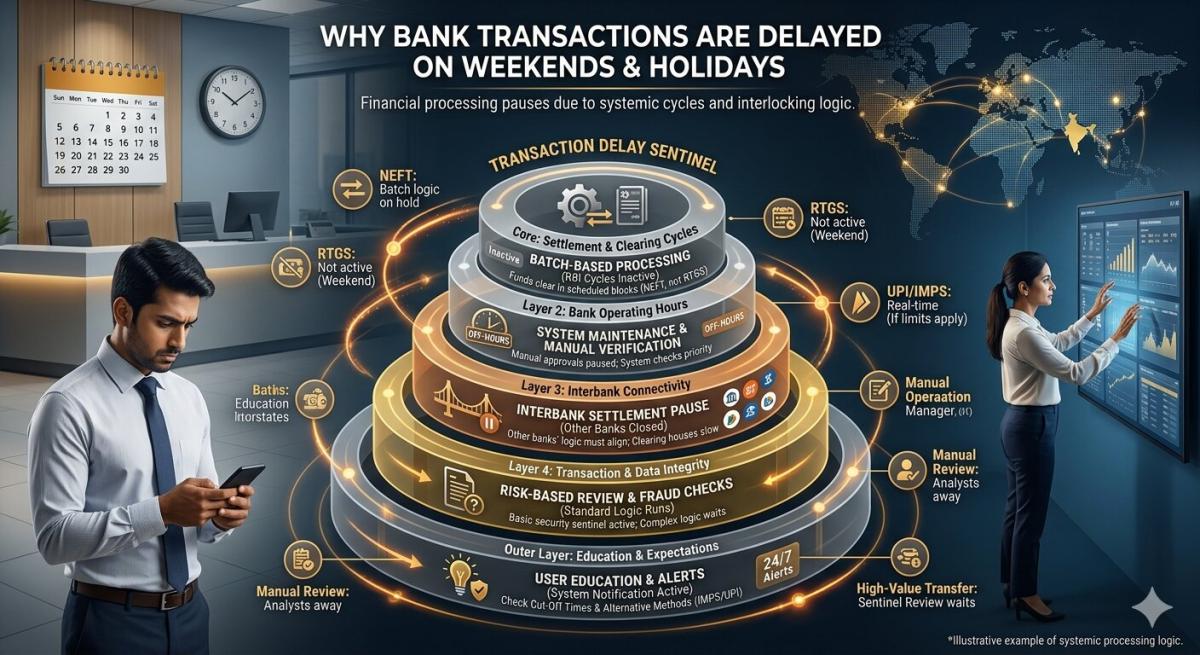

Why Bank Transactions Are Delayed on Weekends & Holidays

Learn why bank transactions are delayed on weekends and holidays, including ACH processing, bank cut-off times, fraud checks, and interbank settlement delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Are Bank Transfers So Slow? The Real Reasons Revealed

Discover why bank transfers are slow, including legacy banking systems, ACH processing, fraud checks, intermediary banks, and cut-off times in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

How Banking Networks Scale to Handle High Transaction Loads

Learn how banking networks handle high transaction volumes using ACH, RTGS, SWIFT, cloud infrastructure, AI fraud detection, and real-time payments in 2026.

Arjun Sharma

Content Lead – Banking & Payments

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ