Why Are Bank Transfers So Slow? The Real Reasons Revealed

Discover why bank transfers are slow, including legacy banking systems, ACH processing, fraud checks, intermediary banks, and cut-off times in 2026.

Table of Contents

Have you ever hit “send” on a bank transfer, then watched the days tick by, wondering where your money was? I certainly have. Once, I needed to pay a contractor urgently for a project, sent the money, and then spent two agonizing days explaining to them why it hadn’t arrived, despite my bank confirming it was “sent.” It felt like sending a letter by carrier pigeon in the age of email. This common frustration leads many to ask: what is the real reason behind slow bank transfer processing? It’s not always about your bank being inefficient; often, it’s a complex interplay of outdated systems, rigorous security protocols, and a global financial architecture that was never designed for the instant gratification we expect in 2026.

The Weight of Legacy Infrastructure

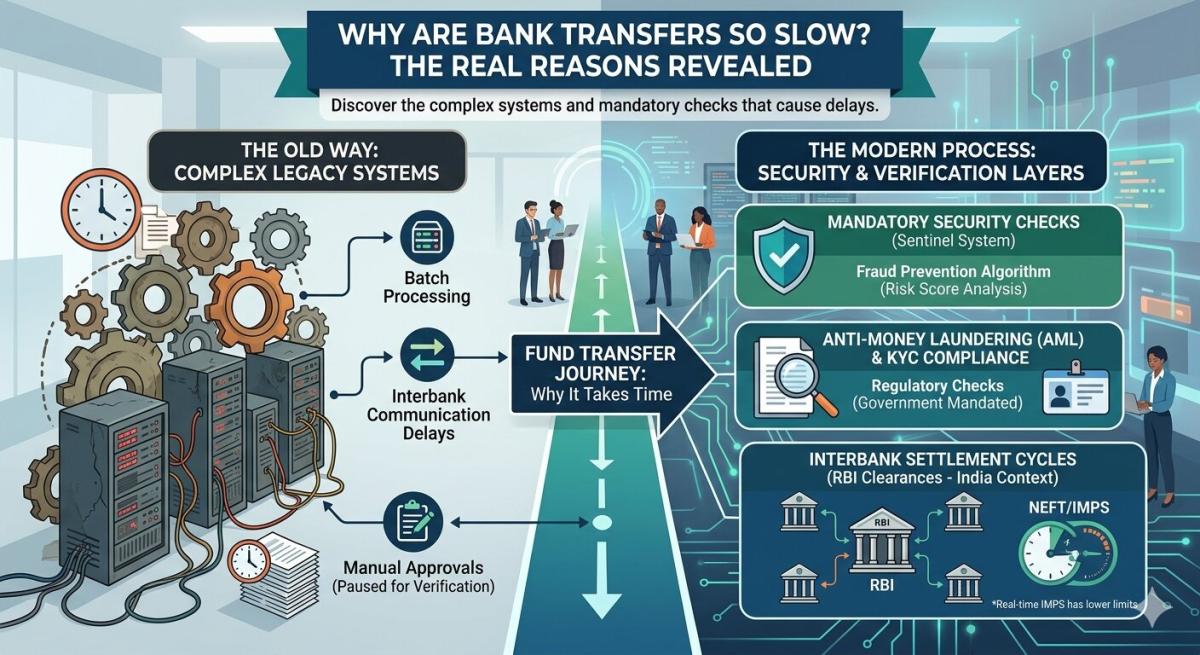

One of the most significant contributors to slow bank transfers is the sheer age and complexity of the underlying banking infrastructure. Many financial institutions still rely on systems built decades ago – mainframes and batch processing operations that were state-of-the-art in the 1970s and 80s. These systems collect transactions throughout the day and process them in large batches, typically overnight, rather than individually in real-time. This method, while incredibly robust and secure, inherently introduces delays, as your transaction waits its turn in a digital queue before it can move to the next stage.

Upgrading these core banking systems is an monumental undertaking, often costing billions and taking years, fraught with significant risks. Consequently, many banks opt for piecemeal updates, bolting on newer technologies to ancient foundations. This creates a complex, sometimes clunky, hybrid environment where different systems might not communicate seamlessly. Think of it as a sprawling city where modern skyscrapers stand next to ancient aqueducts; everything works, but the overall flow can be less than optimal, leading directly to the perceived sluggishness in processing your digital payments.

Vigilant Fraud Prevention & Compliance

Another crucial, often underestimated, factor in delayed transfers is the extensive network of fraud prevention and compliance checks. Every single transaction, regardless of size or destination, is subjected to rigorous scrutiny. Banks are legally obligated to detect and prevent financial crimes such as money laundering (AML), terrorist financing, and various forms of fraud. This isn’t just a courtesy; failure to comply can result in massive fines, reputational damage, and even loss of operating licenses for financial institutions.

These checks involve sophisticated algorithms and, crucially, human oversight. If a transaction triggers certain flags – perhaps an unusually large amount, a destination in a high-risk country, or a pattern inconsistent with your usual activity – it will be held for manual review. This manual intervention, while absolutely vital for protecting consumers and the financial system, inherently adds time to the processing period. It’s a necessary evil that prioritizes security and legality over raw speed, ensuring the integrity of your money and the wider economic landscape.

Detecting Suspicious Activity

When a transaction is flagged, it enters a specialized queue for deeper investigation. This involves checking against sanctions lists published by governments (like OFAC in the US), identifying politically exposed persons (PEPs), and analyzing transaction data for anomalies that could indicate illicit activity. For instance, a sudden large transfer to a new beneficiary in a country you’ve never transacted with before might warrant a closer look. These sophisticated systems are designed to protect against evolving threats, and the human analysts involved are highly trained experts, but this thoroughness requires time, often extending transfer processing by hours or even days.

The Intermediary Bank Network

For international transfers, the process becomes significantly more complex due to the involvement of intermediary, or correspondent, banks. Unlike domestic transfers that might go directly between two banks, cross-border payments often need to traverse a web of financial institutions. Your bank might not have a direct relationship with the recipient’s bank, necessitating the use of one or more intermediate banks to facilitate the transfer of funds. Each intermediary bank adds a step to the process, which inevitably adds time.

The SWIFT network, while globally ubiquitous, is primarily a messaging system, not a direct funds transfer mechanism. It tells banks where and how to move money, but the actual funds movement still relies on the correspondent banking relationships. Each bank in the chain has its own processing times, cut-off hours, and compliance checks. Furthermore, differences in time zones, operating hours, and local banking holidays across different countries can further compound delays, making a “next-day” international transfer often stretch into several business days.

Cut-off Times and Non-Business Days

Bank processing isn’t a 24/7 operation in the way that digital platforms often are. Most banks operate with strict “cut-off times” for processing daily transactions. If you initiate a transfer after this designated time – which can vary, but is often late afternoon – your transaction won’t begin processing until the next business day. It simply sits in a queue, awaiting the start of the new processing cycle. This is a fundamental operational reality that often catches people off guard when expecting instant results.

Moreover, the impact of weekends and public holidays cannot be overstated. A transfer initiated on a Friday afternoon after the cut-off time will likely not begin processing until Monday morning. Add a public holiday to that weekend, and suddenly a transfer that felt instant on your app could take four or five days to clear. This isn’t your money being lost; it’s simply waiting for the banking system’s operational calendar to align, a common reason for perceived slowness that is entirely predictable once understood. For more details on banking operations, you can often find resources on the Federal Reserve’s payment systems page.

The Payment Network Labyrinth

The specific payment network chosen for your transfer also plays a critical role in its speed. In the US, for instance, the Automated Clearing House (ACH) network is used for many common transfers like direct deposits, bill payments, and standard bank-to-bank transfers. ACH is highly efficient and low-cost, but it’s designed for batch processing, meaning transactions typically take 1-3 business days to clear. It’s not built for instant settlement, though initiatives like FedNow are changing this landscape in 2026 and beyond.

Conversely, wire transfers offer near real-time settlement, often clearing within hours domestically, but they come at a higher cost due to their expedited nature and direct processing. International wire transfers, while faster than some alternatives, still contend with the intermediary bank complexities mentioned earlier. Understanding these different payment rails – ACH, wire, SWIFT, and newer real-time payment systems – is key to managing expectations. The “slow” transfer is often just the default, cost-effective method, not an indication of inefficiency.

Key Takeaways

- Legacy Systems Persist: Many banks still rely on older, batch-processing infrastructure that wasn’t built for instant digital transfers, leading to inherent delays as transactions are queued and processed in cycles.

- Security Over Speed: Rigorous fraud prevention, anti-money laundering (AML), and compliance checks are mandated by law and are critical for financial security, often requiring manual review for flagged transactions, which adds processing time.

- Intermediaries Add Complexity: International transfers frequently involve multiple correspondent banks, each with its own processing times and cut-off schedules, extending the overall duration of the transaction.

- Operational Realities Matter: Bank cut-off times, weekends, and public holidays significantly impact when a transfer actually begins and completes processing, often adding several days to the perceived transfer time.

Frequently Asked Questions

Why are international transfers so much slower?

International transfers are slower due to the involvement of multiple intermediary banks, differences in time zones, varying operational hours, and the need for more extensive compliance and fraud checks across different regulatory jurisdictions. The SWIFT network, while facilitating messages, doesn’t instantly move money itself.

Can I speed up a bank transfer?

You can often choose faster options like wire transfers for a fee, which offer quicker settlement than standard ACH transfers. For international payments, some newer fintech services leverage different rails or pre-funded accounts to offer faster, though not always instant, services. Always initiate transfers well before cut-off times and avoid weekends.

What’s the difference between ACH and Wire?

ACH (Automated Clearing House) transfers are typically batch-processed, low-cost, and take 1-3 business days. They’re common for payroll and bill payments. Wire transfers are processed individually, offer near real-time settlement (often within hours domestically), but come with higher fees due to their expedited and direct nature.

Are “instant” payments truly instant?

Newer “instant” payment systems, like FedNow in the US or SEPA Instant Credit Transfer in Europe, facilitate near real-time transfer and settlement 24/7/365. While technically instant between participating banks, the availability depends on both sender and receiver banks supporting the specific instant payment rail. They represent a significant shift from traditional processing.

Conclusion

The reality of slow bank transfer processing is less about individual bank inefficiency and more about the intricate, layered architecture of the global financial system. From legacy technology and rigorous security protocols to the web of international intermediaries and operational cut-off times, each element plays a part. While the frustration is understandable, recognizing these underlying complexities helps demystify the process. As we move towards 2026, the industry continues to evolve with faster payment rails, promising a future where instant transfers become the norm, not the exception.

Related Blogs

Published on Apr 09, 2026

IFSC Code Explained: How Banks & Branches Connect Internally

Ever wonder how banks communicate? Explore the internal mechanics of how the IFSC code links your branch to the national payment network for NEFT, RTGS, and IMPS.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Transaction Cut-Off Times: Avoid Fund Transfer Delays

Learn how transaction cut-off times affect fund transfers, ACH payments, wire transfers, and real-time payments to avoid delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Bank Transactions Are Delayed on Weekends & Holidays

Learn why bank transactions are delayed on weekends and holidays, including ACH processing, bank cut-off times, fraud checks, and interbank settlement delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

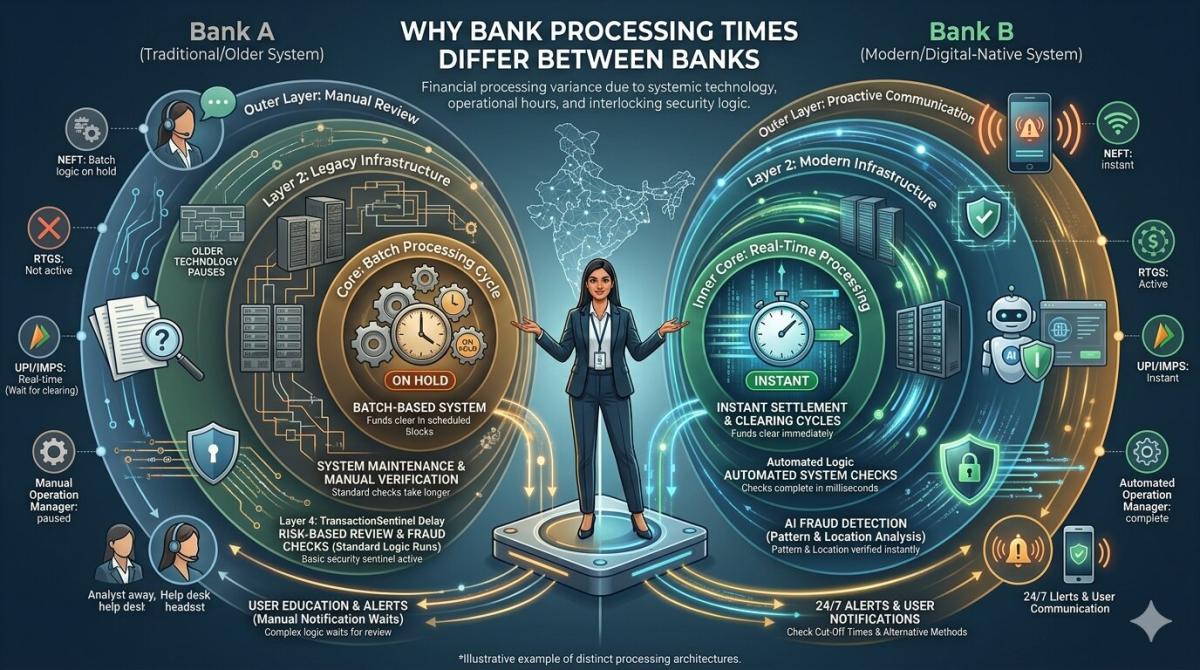

Why Bank Processing Times Differ Between Banks

Learn why bank processing times vary between banks, including ACH, wire transfers, SWIFT, compliance checks, cut-off times, and banking technology in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

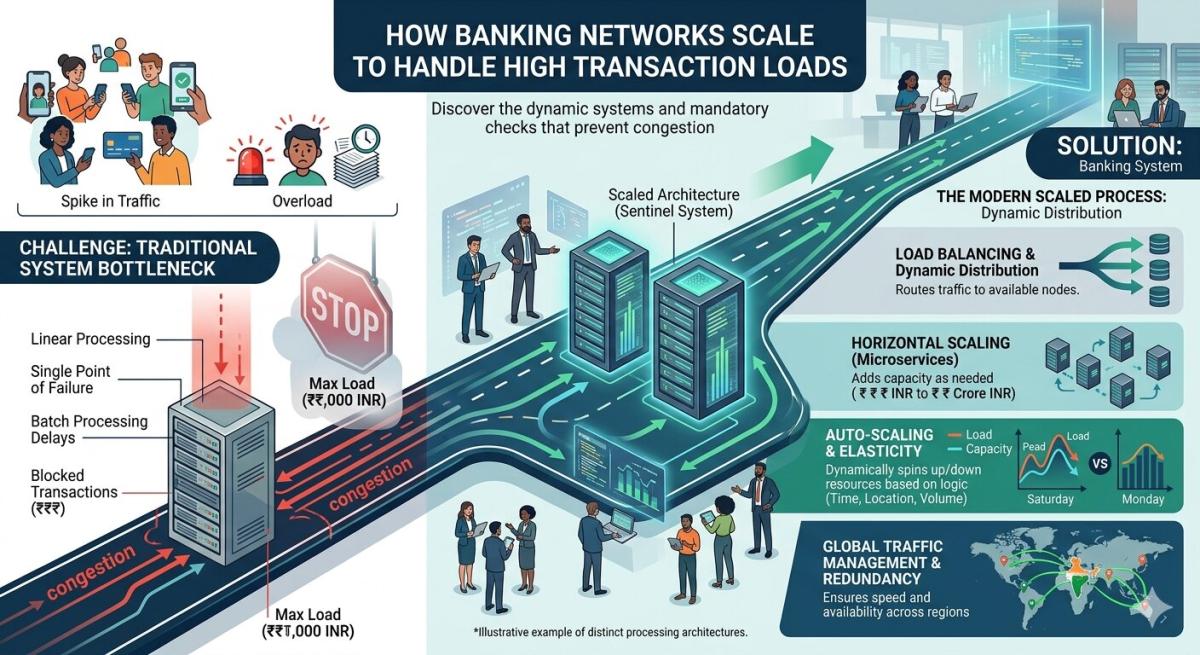

How Banking Networks Scale to Handle High Transaction Loads

Learn how banking networks handle high transaction volumes using ACH, RTGS, SWIFT, cloud infrastructure, AI fraud detection, and real-time payments in 2026.

Arjun Sharma

Content Lead – Banking & Payments

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ