Transaction Cut-Off Times: Avoid Fund Transfer Delays

Learn how transaction cut-off times affect fund transfers, ACH payments, wire transfers, and real-time payments to avoid delays in 2026.

Table of Contents

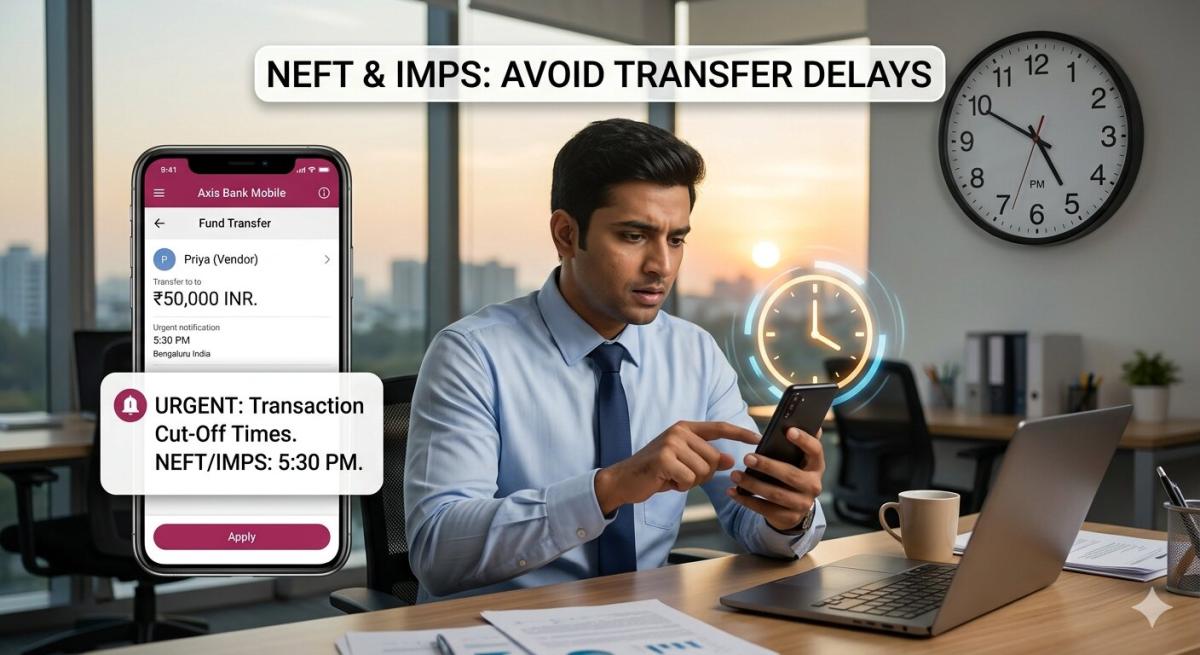

I still remember the heart-stopping moment: it was a Friday afternoon, 4:35 PM, and I’d just initiated a critical wire transfer for a vendor, assuming it would arrive that very day. My bank’s cut-off time? A mere 4:30 PM. That 5-minute oversight meant the payment wouldn’t process until Monday, triggering a late fee and a very uncomfortable conversation. This personal experience vividly illustrates the profound Transaction Cut Off Timing Impact On Fund Transfer, a concept often overlooked until it causes real-world headaches. Understanding these crucial deadlines isn’t just about avoiding fees; it’s about maintaining trust, managing cash flow, and ensuring the smooth operation of your financial life, whether personal or business.

The Undeniable Reality of Banking Hours

Every financial institution, from the largest global bank to the smallest credit union, operates within specific timeframes for processing transactions. These “cut-off times” are not arbitrary; they are meticulously established to allow banks sufficient time to reconcile accounts, conduct necessary fraud checks, and prepare batches of transactions for clearing through various payment networks. Think of it as the daily deadline for getting your financial “mail” into the system for same-day delivery.

Missing these deadlines means your transaction, regardless of when you initiated it online or through an app, will simply be held until the next business day’s processing window. This isn’t a punitive measure but a logistical necessity. Banks must adhere to strict operational schedules set by payment network operators like the Federal Reserve, ACH (Automated Clearing House), and SWIFT, which themselves have their own processing windows and settlement cycles. It’s a complex ballet of data and money movement, all orchestrated around these critical timings.

Immediate Repercussions for Urgent Payments

The most immediate and often painful consequence of overlooking transaction cut-off times is the delay of urgent payments. Imagine needing to cover an overdraft, make a time-sensitive investment, or send funds for a medical emergency. If you initiate a transfer even minutes past the cut-off, that crucial payment will not reach its destination until the following business day, potentially causing significant stress or financial penalties.

For businesses, the stakes are even higher. Payroll processing, vendor payments, and loan repayments are all highly sensitive to timing. A missed cut-off can lead to late payroll, strained vendor relationships, or even default on loan agreements, incurring hefty late fees and damaging credit scores. In today’s fast-paced economy, a single day’s delay can have a cascading effect, disrupting supply chains and impacting a company’s reputation.

Diverse Payment Rails, Diverse Rules

The world of fund transfers is not monolithic; it’s a tapestry woven with different payment rails, each with its unique operational characteristics and, crucially, its own set of cut-off times. A domestic ACH transfer, for instance, typically has later cut-off times than a wire transfer, but often takes 1-3 business days to settle. International wire transfers via networks like SWIFT can have even earlier cut-offs due to time zone differences and the complexities of correspondent banking relationships, often requiring initiation well before the end of the business day for same-day processing in the recipient country.

Understanding these distinctions is paramount. Relying on the same cut-off assumption for all transfer types is a common pitfall. Banks often provide detailed schedules for each service, and it’s incumbent upon the sender to consult these, especially for high-value or time-critical transactions. The choice of payment rail directly dictates the speed and finality of the transfer, making it a critical decision in managing the Transaction Cut Off Timing Impact On Fund Transfer effectively.

Real-Time Payments: The Game Changer

In stark contrast to traditional payment systems, Real-Time Payments (RTP) networks, such as The Clearing House’s RTP network in the U.S. or SEPA Instant Credit Transfer in Europe, operate 24 hours a day, 7 days a week, 365 days a year. These systems largely bypass the concept of “cut-off times” as we know them, offering immediate settlement and availability of funds to the recipient. This capability is revolutionizing urgent payments, enabling instant transfers even on weekends and holidays, eliminating the anxiety associated with traditional banking hours.

The Far-Reaching Ripple Effect

The impact of transaction cut-off timing extends far beyond the sender and immediate recipient. Consider a business paying its suppliers. If a payment is delayed due to a missed cut-off, that supplier might face cash flow issues, potentially delaying their own payments to their employees or sub-contractors. This creates a domino effect throughout the economic chain, highlighting how interconnected our financial systems truly are.

On a personal level, missing a loan payment due to a cut-off oversight can trigger late fees, negatively affect credit scores, and even lead to more severe consequences like repossessions. Similarly, delaying a down payment for a property or a critical tuition fee can lead to significant complications. Proactively managing your payment schedules and understanding the definitive Transaction Cut Off Timing Impact On Fund Transfer ensures that your financial commitments are met precisely when they are due, protecting your financial well-being and relationships.

Strategies for Seamless Fund Transfers

Navigating the intricacies of transaction cut-off times requires a proactive and informed approach. First and foremost, always verify the specific cut-off times for the type of transfer you intend to make with your financial institution; these can vary significantly even between different branches or online platforms. Many banks publish these schedules prominently on their websites or within their online banking portals. For instance, the J.P. Morgan website offers detailed information for its clients.

Secondly, consider leveraging payment scheduling features offered by most banking platforms. Setting up payments in advance, with a buffer of at least one full business day before the actual due date, is a robust strategy to mitigate risks. For time-critical payments, especially as we approach 2026, explore real-time payment options if available through your bank, as these often circumvent traditional cut-off limitations entirely. Building a habit of checking these times ensures peace of mind and financial accuracy.

Key Takeaways

- Cut-off times are non-negotiable deadlines: They dictate whether a transaction processes on the same business day or is deferred to the next. Ignoring them leads directly to delays.

- Different transfer types have distinct cut-offs: Wire transfers, ACH payments, and international transfers each operate under unique timing rules. Always verify the specific cut-off for your chosen method.

- Delays have real-world consequences: Missed deadlines can result in late fees, damaged credit scores, strained business relationships, and significant personal stress, particularly for urgent financial commitments.

- Proactive planning is essential: Always check your bank’s published cut-off times, schedule payments with ample lead time, and consider using real-time payment options for critical, time-sensitive transfers in 2026 and beyond.

Frequently Asked Questions

What happens if I initiate a transfer after the cut-off?

If you initiate a transfer after the specified cut-off time, your financial institution will typically hold the transaction and process it on the next available business day. This means the funds will not reach the recipient until that following business day, potentially causing delays and, in some cases, incurring late fees or other penalties.

Do cut-off times vary by bank or type of transfer?

Absolutely. Cut-off times can vary significantly between different banks and even within the same bank for different types of transfers (e.g., domestic wire vs. international wire, ACH vs. bill pay). It’s crucial to consult your specific bank’s official schedule for each service you intend to use.

Are there ways to avoid cut-off delays for urgent payments?

Yes, several strategies can help. Always initiate payments well in advance of the deadline, ideally with a day or two buffer. For truly urgent needs, explore if your bank offers Real-Time Payments (RTP), which process 24/7/365. Additionally, some banks might offer expedited wire services for an extra fee, though these still have their own, albeit often later, cut-off times.

How do weekends and holidays affect cut-off times?

Weekends and bank holidays significantly impact cut-off times. If a cut-off falls on a non-business day, any transaction initiated after the preceding business day’s cut-off will not be processed until the next business day following the holiday or weekend. This is why planning is crucial for payments due around these periods, especially as we plan for major financial movements in 2026.

Conclusion

The seemingly mundane detail of transaction cut-off timing holds surprising power over the swift and successful movement of your money. It’s a fundamental aspect of modern finance that, when understood and respected, can prevent a myriad of potential headaches, from late fees to damaged relationships. By embracing proactive planning, familiarizing yourself with your bank’s specific deadlines, and leveraging modern payment solutions, you can confidently navigate the financial landscape and ensure your funds always arrive precisely when and where they’re needed. Don’t let a simple time stamp dictate your financial success.

Related Blogs

Published on Apr 09, 2026

IFSC Code Explained: How Banks & Branches Connect Internally

Ever wonder how banks communicate? Explore the internal mechanics of how the IFSC code links your branch to the national payment network for NEFT, RTGS, and IMPS.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Bank Transactions Are Delayed on Weekends & Holidays

Learn why bank transactions are delayed on weekends and holidays, including ACH processing, bank cut-off times, fraud checks, and interbank settlement delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Bank Processing Times Differ Between Banks

Learn why bank processing times vary between banks, including ACH, wire transfers, SWIFT, compliance checks, cut-off times, and banking technology in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Are Bank Transfers So Slow? The Real Reasons Revealed

Discover why bank transfers are slow, including legacy banking systems, ACH processing, fraud checks, intermediary banks, and cut-off times in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

How Banking Networks Scale to Handle High Transaction Loads

Learn how banking networks handle high transaction volumes using ACH, RTGS, SWIFT, cloud infrastructure, AI fraud detection, and real-time payments in 2026.

Arjun Sharma

Content Lead – Banking & Payments

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ