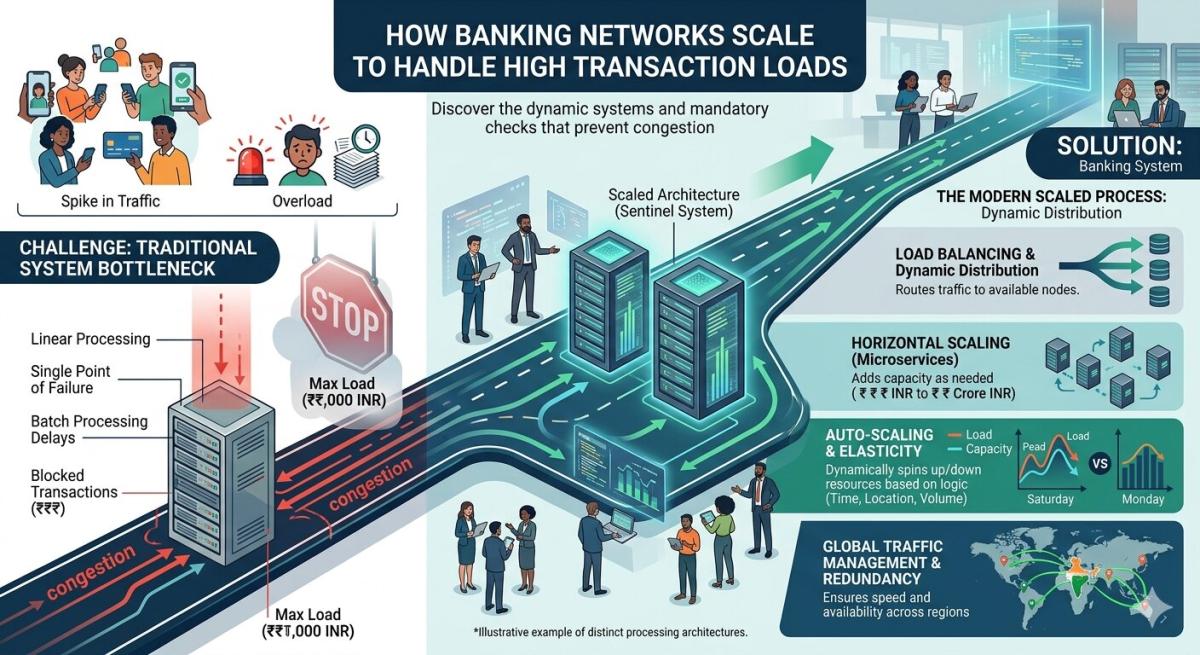

How Banking Networks Scale to Handle High Transaction Loads

Learn how banking networks handle high transaction volumes using ACH, RTGS, SWIFT, cloud infrastructure, AI fraud detection, and real-time payments in 2026.

Table of Contents

Have you ever paused to consider the sheer complexity behind a simple tap of your card or a quick online transfer? It’s a moment that often goes unappreciated, yet beneath the surface lies an intricate, high-stakes ballet of technology and coordination. Just last month, during a particularly frantic holiday shopping surge, I found myself marveling at how smoothly every transaction processed, despite millions of people doing the exact same thing simultaneously. This isn’t magic; it’s the result of decades of innovation designed to answer the fundamental question: How banking network handles high transaction load? It’s a system built for volume, speed, and ironclad security, constantly evolving to meet ever-growing demands.

The Unseen Ballet of Transaction Processing

Every financial transaction, from a small coffee purchase to a multi-million dollar corporate transfer, embarks on a complex journey through a bank’s internal systems. At its core, this involves sophisticated ledger management, where every debit and credit is meticulously recorded and reconciled. These core banking systems are the central nervous system, ensuring that your account balance accurately reflects your real-time financial position. They perform immediate validity checks, verifying sufficient funds, account status, and compliance with internal rules, all within milliseconds of your initial request.

Once initial internal checks pass, the transaction often moves to a payment gateway or a bank’s internal switch. These intelligent routers direct the transaction to the appropriate network for authorization and settlement. For card payments, this involves communicating with card networks like Visa or Mastercard. For direct transfers, it might be an interbank network. The efficiency of these switches is paramount; they act as traffic controllers, optimizing pathways to minimize latency and prevent bottlenecks, especially during peak hours when millions of requests are flooding the system.

The Crucial Role of Interbank Networks

When your transaction needs to cross bank boundaries, it relies on global interbank networks designed for secure and rapid communication. SWIFT (Society for Worldwide Interbank Financial Telecommunication) is perhaps the most well-known, providing a highly secure messaging service that allows financial institutions worldwide to send and receive information about financial transactions. While SWIFT doesn’t hold funds, it facilitates the instructions that enable banks to move money between accounts across different countries, handling an enormous volume of messages daily with robust encryption.

Domestically, high transaction loads are managed through systems like Automated Clearing Houses (ACH) for batch processing of large volumes of non-urgent payments, and Real-Time Gross Settlement (RTGS) systems for immediate, high-value transfers. ACH networks are crucial for payroll, bill payments, and direct deposits, efficiently bundling transactions to reduce individual processing costs. RTGS systems, conversely, settle transactions individually and immediately, providing finality of payment in real-time, which is essential for critical interbank transfers and ensuring systemic stability.

Optimizing for Real-Time Payments

The global push towards instant payments is fundamentally reshaping how banking networks handle transaction loads, demanding even greater speed and 24/7 availability. Systems like Faster Payments in the UK, SEPA Instant Credit Transfer in Europe, and FedNow in the US (launched in 2026) allow money to move between accounts at different banks in seconds, rather than hours or days. This requires a complete overhaul of traditional batch processing, necessitating always-on infrastructure, advanced fraud detection running in parallel, and robust liquidity management to ensure banks can meet immediate settlement obligations. The shift represents a significant technological and operational challenge, yet it’s undeniably the direction the industry is heading by 2026.

Architecting for Scalability and Resilience

To withstand the fluctuating demands of high transaction loads, banking networks are engineered for extreme scalability and resilience. This involves leveraging distributed system architectures, where processing power and data storage are spread across multiple servers and locations. Load balancers intelligently distribute incoming transaction requests across these resources, preventing any single server from becoming overwhelmed. Cloud computing has become a game-changer, allowing banks to dynamically scale their infrastructure up or down in response to real-time transaction volumes, offering unparalleled flexibility and cost efficiency compared to traditional on-premise solutions.

Resilience is equally paramount, as any downtime can have catastrophic financial consequences. Banks employ rigorous disaster recovery and business continuity plans, often involving redundant systems in geographically dispersed data centers. If a primary system fails, a secondary system can take over almost instantaneously, ensuring uninterrupted service. These failover mechanisms are tested regularly, sometimes several times a year, to ensure they can handle unexpected outages, cyberattacks, or natural disasters, safeguarding the integrity and availability of financial services around the clock.

Fortifying Defenses Against Digital Threats

With high transaction loads comes an amplified risk of cyberattacks and fraud, making security an absolute cornerstone of banking network operations. Banks deploy multi-layered security protocols, starting with robust encryption for all data in transit and at rest, protecting sensitive financial information from interception. Firewalls, intrusion detection systems, and advanced authentication methods are standard, creating formidable barriers against unauthorized access. The constant cat-and-mouse game with cybercriminals means banks are perpetually investing in the latest security technologies and threat intelligence.

The battle against fraud is particularly intense, with sophisticated schemes attempting to exploit high transaction volumes. Banks now heavily rely on artificial intelligence and machine learning algorithms to detect fraudulent activity in real-time. These systems analyze vast datasets of historical transactions, identifying unusual patterns, anomalies, and behavioral deviations that might indicate fraud. By flagging suspicious transactions instantly, often before they are fully processed, banks can prevent significant losses and protect their customers, a capability that continues to grow more sophisticated by 2026.

The Road Ahead: Innovation in 2026 and Beyond

The banking network continues its relentless evolution, driven by technological innovation and shifting consumer expectations. Blockchain technology, for instance, holds significant promise for cross-border payments, potentially offering faster, more transparent, and more cost-effective settlement compared to traditional methods. While mainstream adoption faces regulatory and scalability hurdles, pilot programs and niche applications are already demonstrating its potential to disrupt parts of the existing financial infrastructure. The distributed ledger technology could, in the long run, revolutionize how banks manage and verify transactions on a global scale.

Open Banking and the API (Application Programming Interface) economy are also redefining financial services, enabling seamless integration between banks and third-party providers. This fosters innovation, allowing customers to manage finances more effectively through a wider array of services and applications. As financial ecosystems become more interconnected, the underlying banking networks must become even more agile and robust, capable of handling an explosion of API calls alongside traditional transaction volumes. The focus for 2026 and beyond will be on creating highly interoperable, secure, and scalable financial infrastructure that can support this increasingly complex digital landscape, empowering a new generation of financial products and services.

Key Takeaways

- Banking networks utilize complex core systems, payment gateways, and interbank networks like SWIFT and domestic ACH/RTGS to manage vast transaction volumes.

- The shift towards real-time payment systems (e.g., FedNow) demands always-on infrastructure, advanced fraud detection, and immediate settlement capabilities, pushing the boundaries of existing financial technology.

- Scalability and resilience are achieved through distributed system architectures, cloud computing, load balancing, and robust disaster recovery plans, ensuring continuous service even during peak loads or outages.

- Multi-layered security protocols, including encryption and AI-driven fraud detection, are critical for protecting transactions and customer data from an ever-evolving landscape of cyber threats.

Frequently Asked Questions

What is the difference between ACH and RTGS?

ACH (Automated Clearing House) systems are typically used for batch processing of non-urgent, high-volume transactions like payroll, bill payments, and direct deposits. They are cost-effective but take longer to settle, often a few business days. RTGS (Real-Time Gross Settlement) systems, conversely, process and settle transactions individually and immediately, providing finality of payment within seconds. RTGS is used for high-value, urgent interbank transfers and plays a crucial role in maintaining financial stability.

How do banks prevent fraud during high transaction loads?

Banks employ sophisticated, multi-layered fraud prevention strategies. This includes real-time transaction monitoring powered by AI and machine learning algorithms that analyze behavioral patterns and flag anomalies instantly. They also use advanced encryption, multi-factor authentication, and robust security protocols across their networks. During high transaction loads, these automated systems are critical as manual oversight would be impossible, ensuring rapid detection and prevention of fraudulent activities.

What role does cloud computing play in handling banking transaction loads?

Cloud computing provides banks with unparalleled flexibility and scalability to handle fluctuating transaction loads. Instead of maintaining vast, expensive on-premise infrastructure that might only be fully utilized during peak times, banks can leverage cloud resources to dynamically scale their processing power and storage up or down as needed. This allows them to efficiently manage sudden spikes in transaction volume, reduce operational costs, and deploy new services more rapidly, enhancing overall resilience and agility.

Are cryptocurrencies and blockchain affecting traditional banking networks?

Yes, cryptocurrencies and blockchain technology are beginning to influence traditional banking networks, primarily by inspiring innovation in payment processing. While direct integration is still nascent, banks are exploring blockchain for cross-border payments, trade finance, and improved settlement efficiency. The underlying distributed ledger technology offers potential for greater transparency, speed, and cost reduction, prompting traditional networks to evolve and adopt similar principles or integrate with these emerging technologies to remain competitive and efficient.

Conclusion

The ability of banking networks to seamlessly handle immense transaction loads is a testament to continuous innovation and robust engineering. From the moment you initiate a payment to its final settlement, a complex web of core systems, interbank networks, and advanced security measures works in concert, often without you even noticing. As we look towards 2026 and beyond, the ongoing evolution towards instant payments, AI-driven security, and cloud-based infrastructure will only make these systems more resilient, efficient, and capable of supporting the increasingly digital global economy. It’s a field where passion for problem-solving truly translates into everyday convenience and financial stability for millions.

Related Blogs

Published on Apr 09, 2026

IFSC Code Explained: How Banks & Branches Connect Internally

Ever wonder how banks communicate? Explore the internal mechanics of how the IFSC code links your branch to the national payment network for NEFT, RTGS, and IMPS.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Transaction Cut-Off Times: Avoid Fund Transfer Delays

Learn how transaction cut-off times affect fund transfers, ACH payments, wire transfers, and real-time payments to avoid delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Bank Transactions Are Delayed on Weekends & Holidays

Learn why bank transactions are delayed on weekends and holidays, including ACH processing, bank cut-off times, fraud checks, and interbank settlement delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Bank Processing Times Differ Between Banks

Learn why bank processing times vary between banks, including ACH, wire transfers, SWIFT, compliance checks, cut-off times, and banking technology in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Are Bank Transfers So Slow? The Real Reasons Revealed

Discover why bank transfers are slow, including legacy banking systems, ACH processing, fraud checks, intermediary banks, and cut-off times in 2026.

Arjun Sharma

Content Lead – Banking & Payments

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ