RTGS Transaction Internal Flow: A Step-by-Step Guide

How does RTGS work? Discover the internal flow of Real-Time Gross Settlement, from RBI processing to instant beneficiary credit in our 2026 banking guide.

Table of Contents

Imagine a scenario where a critical, time-sensitive payment absolutely had to reach its destination within minutes – perhaps for a property deal closing, an urgent medical expense, or to avoid a hefty late fee. In such moments, the traditional banking cadence feels agonizingly slow. This is precisely where Real-Time Gross Settlement (RTGS) steps in, offering a robust, instantaneous solution for large-value interbank transfers. Understanding the step by step internal flow of an RTGS transaction isn’t just for financial professionals; it offers a fascinating glimpse into the secure, high-speed backbone of modern financial infrastructure, ensuring your significant funds move with incredible efficiency and finality.

The Initiation: Your Bank’s First Move

The journey of an RTGS transaction begins the moment you, the remitter, submit your request to your bank. Whether you’re filling out a physical form at a branch or initiating it through your bank’s secure online portal, this initial step involves providing crucial details: the beneficiary’s name, account number, the amount, and critically, the Indian Financial System Code (IFSC) of the beneficiary’s bank and branch. My personal experience has shown that double-checking these details meticulously at this stage can save hours of potential headaches later, as even a minor discrepancy can cause delays or outright rejection.

Upon receiving your request, your bank immediately undertakes a series of internal validations. This isn’t just a cursory glance; it’s a sophisticated check. First, they verify your identity and ensure that your account holds sufficient funds to cover the transaction amount, including any applicable service charges. This real-time fund blockage is a critical safeguard, preventing overdrafts and ensuring the payment’s integrity. Furthermore, the bank’s system cross-references the beneficiary’s IFSC code to confirm its validity and existence within the banking network, a crucial step before the funds even begin their digital journey.

Entering the RTGS Network

Once your bank’s internal validations are complete, the transaction is prepared for transmission into the RTGS network. Your bank’s core banking system (CBS) generates a payment message, meticulously formatted to meet the strict standards required by the Reserve Bank of India (RBI). This message isn’t just raw data; it’s a structured instruction, often adhering to global messaging standards like SWIFT or India’s own Secured Financial Messaging System (SFMS), encapsulating all the details necessary for settlement, including unique transaction identifiers.

This formatted message is then securely transmitted from your originating bank to the RBI’s central RTGS gateway. This transmission is highly encrypted and takes place over dedicated, secure communication channels, ensuring data integrity and confidentiality. It’s a testament to the robust infrastructure that these high-value transactions traverse digital pathways designed for maximum security and minimal latency. The speed at this stage is truly remarkable, often taking mere seconds for the message to reach the central processing system.

RBI’s Central Role in Processing

The Reserve Bank of India (RBI) acts as the central clearinghouse for all RTGS transactions, a role it performs with remarkable efficiency. Upon receiving the payment message from the originating bank, the RBI’s sophisticated RTGS system immediately validates its format, authenticity, and completeness. It checks for duplicate transactions and ensures that the remitting bank has sufficient balance in its current account with the RBI to cover the payment – a critical aspect of gross settlement, where each transaction is settled individually without netting.

This is where the “Real-Time Gross Settlement” truly lives up to its name. Each transaction is settled on an individual, one-to-one basis, meaning there’s no waiting for other transactions to accumulate. This avoids systemic risk inherent in net settlement systems, where the failure of one participant could cascade. The RBI’s system debits the remitting bank’s account and simultaneously credits the beneficiary bank’s account with the RBI, finalizing the interbank transfer aspect almost instantaneously. For more on the RBI’s role in payment systems, you can refer to their official website.

The Liquidity Management Aspect

A crucial, often overlooked, aspect of the RTGS flow is the liquidity management required by participating banks. Since each transaction is settled individually and in real-time, banks must ensure they always maintain sufficient balances in their current accounts with the RBI. This isn’t just about having enough funds; it’s about dynamic management. Banks constantly monitor their liquidity positions, sometimes needing to borrow short-term funds or manage inflows and outflows to ensure they can meet their RTGS obligations without delay. This proactive approach by banks is essential for the smooth, uninterrupted functioning of the entire RTGS system, preventing payment gridlocks and ensuring timely settlements.

Funds Reaching the Beneficiary Bank

Once the RBI has successfully settled the transaction by debiting the remitting bank and crediting the beneficiary bank’s account with the central bank, a notification message is swiftly dispatched to the beneficiary bank. This message contains all the pertinent details of the incoming payment, including the amount, the remitter’s information, and the unique transaction reference. It’s the digital equivalent of an express delivery notification, informing the recipient bank that funds are now available for their customer.

Upon receiving this settlement message, the beneficiary bank then undertakes its final internal processing. Their core banking system verifies the beneficiary’s account details and credits the specified amount to the customer’s account. This crediting process is typically completed within a very short timeframe, often within seconds or minutes of the beneficiary bank receiving the RBI’s notification. It’s this rapid final leg that makes RTGS so indispensable for urgent, high-value transfers, ensuring funds are accessible almost as soon as they are sent.

Confirmation and Reconciliation

The final stage in the step by step internal flow of an RTGS transaction involves confirmations and meticulous reconciliation. After the beneficiary’s account has been credited, the beneficiary bank sends a confirmation message back to the RBI, acknowledging receipt and successful processing. The RBI, in turn, informs the originating bank of the successful completion. This comprehensive loop ensures transparency and accountability at every stage. Both the remitter and beneficiary typically receive SMS or email notifications from their respective banks, confirming the successful credit or debit, providing peace of mind.

Beyond individual notifications, banks engage in continuous reconciliation processes to ensure that all RTGS transactions are accurately recorded and settled. This involves matching messages, debits, and credits, identifying and resolving any discrepancies. While errors are rare given the system’s robustness, reconciliation ensures that audit trails are pristine and that all financial records align perfectly. This ongoing diligence is crucial for maintaining the integrity and trustworthiness of the RTGS system, which we expect to be even more seamless by 2026, handling an ever-increasing volume of critical payments.

Key Takeaways

- Instantaneous and Final Settlement: RTGS transactions are settled individually and in real-time, offering immediate finality of payment, which significantly reduces settlement risk compared to batch processing systems.

- High-Value Transaction Focus: Designed specifically for large-value transfers, RTGS ensures that significant sums of money move securely and swiftly across the banking network, making it ideal for corporate payments, property transactions, and interbank settlements.

- Robust Security and Reliability: The entire process, from initiation to confirmation, is underpinned by advanced encryption, secure communication channels, and stringent validation protocols implemented by both banks and the RBI, ensuring unparalleled safety.

- Critical for Economic Stability: By facilitating rapid and secure movement of capital, RTGS plays a vital role in maintaining liquidity within the financial system, supporting economic activity, and bolstering confidence in the national payment infrastructure for years to come, certainly well into 2026.

Frequently Asked Questions

What is RTGS and why is it important?

RTGS stands for Real-Time Gross Settlement. It’s an electronic payment system that facilitates large-value interbank fund transfers on a real-time and gross basis. Its importance lies in providing immediate, final settlement of high-value transactions, minimizing systemic risk in the financial system and ensuring swift movement of capital critical for economic operations.

How fast is an RTGS transaction completed?

An RTGS transaction is completed incredibly fast. Once initiated and validated by the remitting bank, the funds are typically settled by the RBI and credited to the beneficiary’s account within minutes, often within 30 minutes to an hour at most under normal operating conditions. This speed is a cornerstone of its utility.

Are there any limits for RTGS transactions?

Yes, there are limits. The minimum amount for an RTGS transaction is typically ₹2,00,000 (Two Lakh Indian Rupees), making it suitable for large-value transfers. While there’s generally no upper limit set by the RBI, individual banks may impose their own upper limits for online RTGS transactions as a security measure, which can usually be increased by visiting a branch.

What happens if an RTGS transaction fails?

If an RTGS transaction fails due to reasons like incorrect beneficiary details, insufficient funds, or technical issues, the remitting bank is immediately notified by the RBI. The funds are then typically reversed and credited back to the remitter’s account. The remitting bank usually informs the customer about the failure and the reversal, advising them to correct the details and re-initiate the transaction.

Conclusion

The step by step internal flow of an RTGS transaction is a masterclass in financial engineering, a testament to how meticulous design and robust technology underpin the modern economy. It’s more than just a transfer; it’s a guarantee of rapid, secure, and final settlement for significant sums, empowering businesses and individuals alike with unparalleled financial agility. As we look towards 2026, the foundational principles of RTGS will continue to ensure that large-value payments remain the bedrock of a stable and efficient financial landscape, evolving only to become even more seamless and integrated.

Related Blogs

Published on Apr 09, 2026

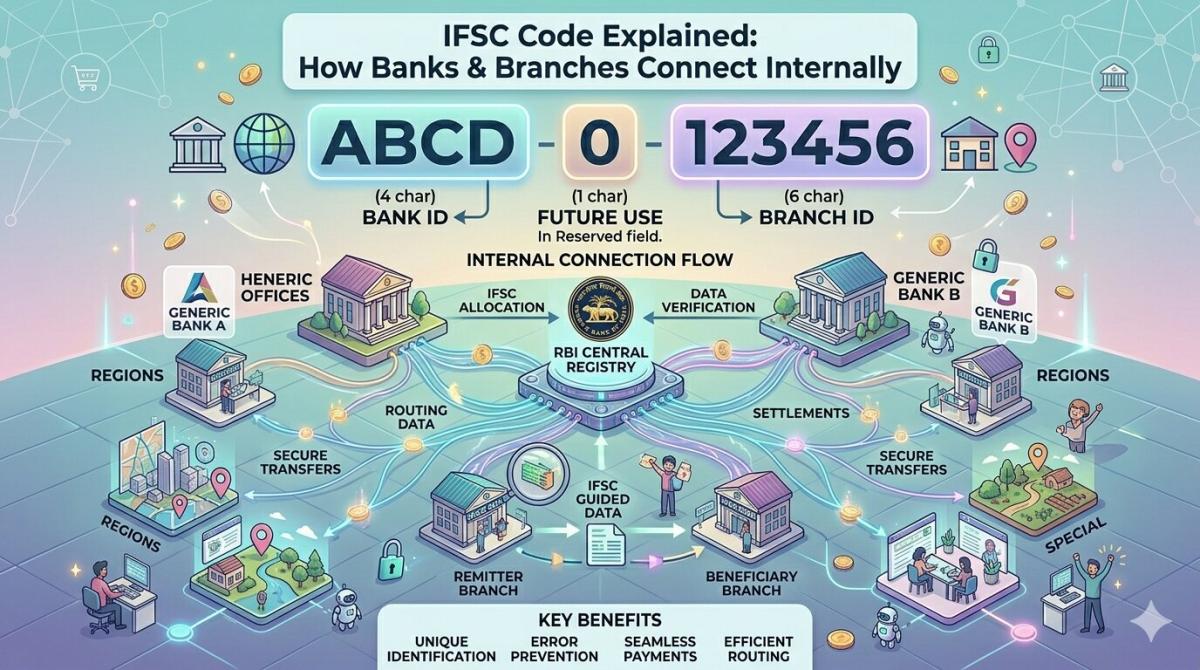

IFSC Code Explained: How Banks & Branches Connect Internally

Ever wonder how banks communicate? Explore the internal mechanics of how the IFSC code links your branch to the national payment network for NEFT, RTGS, and IMPS.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

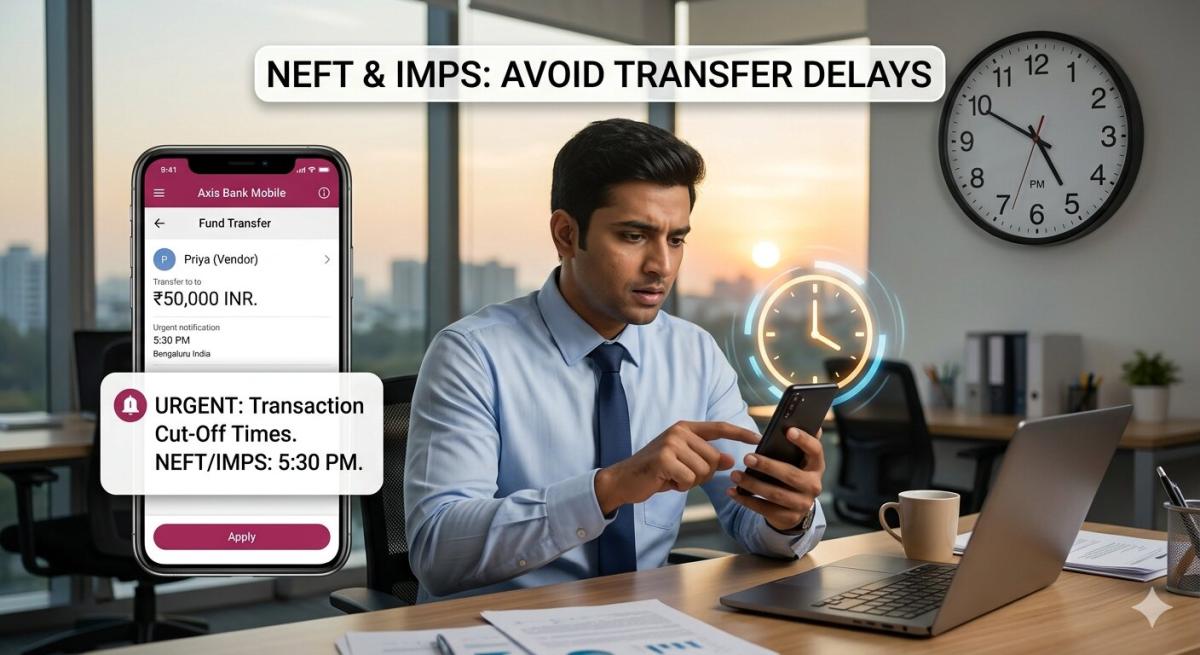

Transaction Cut-Off Times: Avoid Fund Transfer Delays

Learn how transaction cut-off times affect fund transfers, ACH payments, wire transfers, and real-time payments to avoid delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

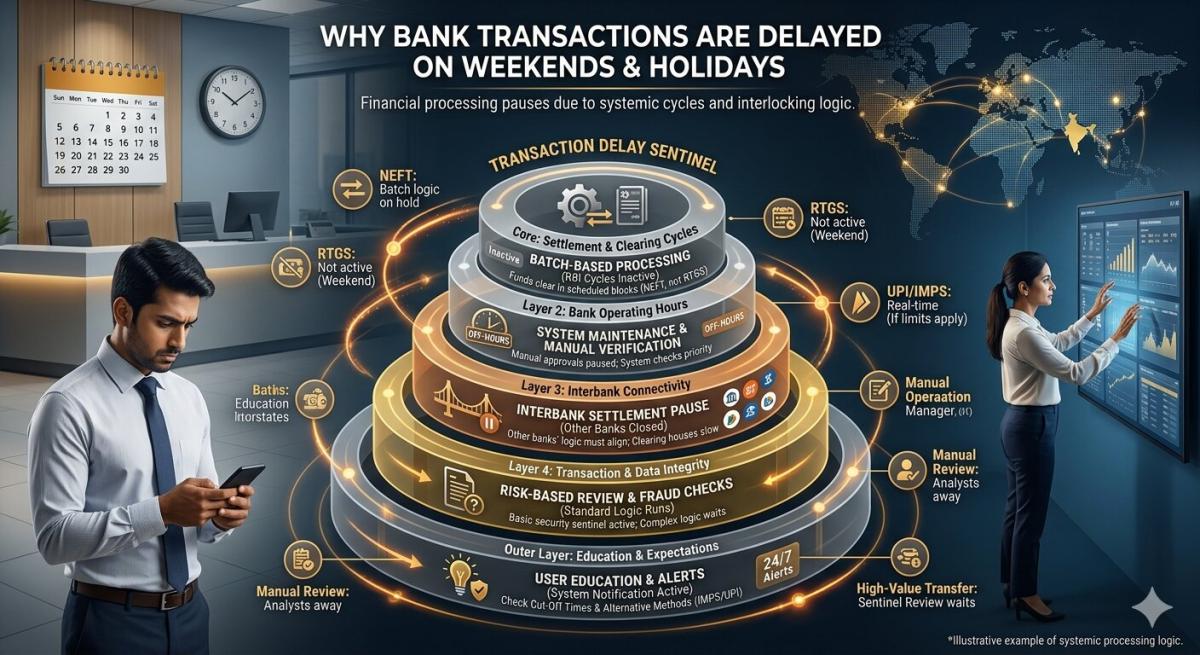

Why Bank Transactions Are Delayed on Weekends & Holidays

Learn why bank transactions are delayed on weekends and holidays, including ACH processing, bank cut-off times, fraud checks, and interbank settlement delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

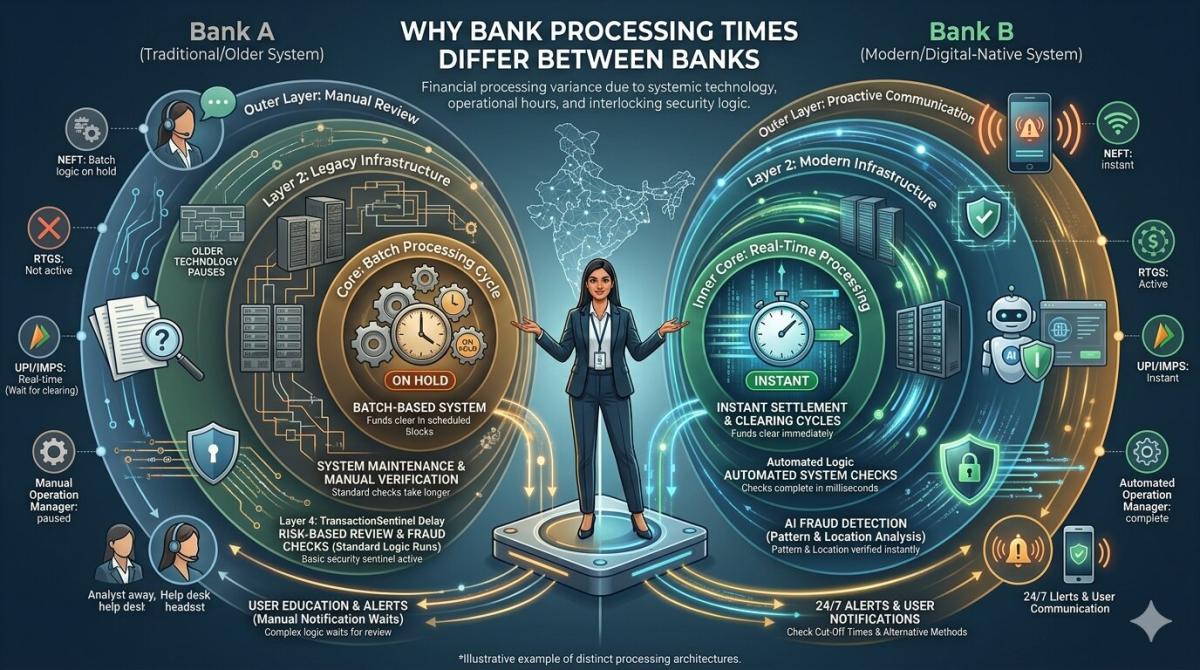

Why Bank Processing Times Differ Between Banks

Learn why bank processing times vary between banks, including ACH, wire transfers, SWIFT, compliance checks, cut-off times, and banking technology in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Are Bank Transfers So Slow? The Real Reasons Revealed

Discover why bank transfers are slow, including legacy banking systems, ACH processing, fraud checks, intermediary banks, and cut-off times in 2026.

Arjun Sharma

Content Lead – Banking & Payments

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ